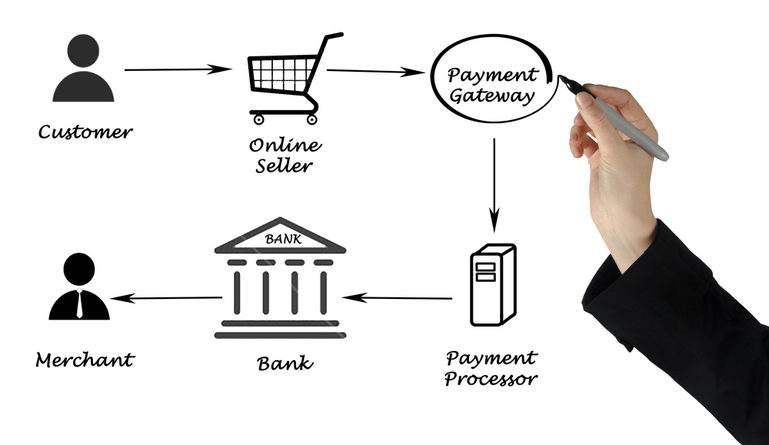

How do Payment Gateways works?

The flow of transactions remains the same where you’re utilizing a virtual or physical payment gateway, however online and mobile payments utilize digital capture files to store the credit card data instead of output from a credit card reader.

Below we have highlighted how does it work:

- The customer initiates a credit card payment via the merchant’s e-commerce site or credit card reader.

- The payment gateway:

- Transfers the transaction data to the receiving bank (the acquirer or merchant bank)

- Identifies which credit card provider (American Express, Discover, or MasterCard) issued the customer’s card.

- Directs the transaction data to the right payment switch

- The payment switch directs the request to the issuing bank (the bank that provided the customer’s credit card) and routes the transaction data onto the right credit card network.

- The issuing bank executes fraud detection measures to verify the authenticity of the transaction and ascertains that the customer has enough credit in their account to complete the purchase.

- The issuing bank either rejects or approves the transaction and passes this information back via the credit card network to the payment gateway and the merchant bank.

It can be likened to a train commuting between stations, with the conductor talking with the station master at every stop.

Credit card payments are verified by the issuing bank (via the payment gateway) at the point of sale. A verified transaction shows that the bank has reserved the funds, however, the merchant is yet to actually receive the payment. This is written as a “pending” transaction when customers check their credit card statements.

After some time, usually at the end of the day, it’s necessary for the merchant to reconcile payments, include tips if necessary, and submit a batch capture manually, or “processing” file, for every awaiting credit card transaction. At this stage, the pending transactions are dedicated, meaning that the merchant now has the entitlement to the funds originally withheld by the issuing bank. The money is then sent to the merchant’s bank and can be accessed immediately they are credited to the merchant account

{kind=link}