Edwards Life Sciences (NYSE:EW) has shown resilience amidst the recent market uncertainty, with a surprisingly sturdy Q2 exit showcased on July 23rd 2020 with clear guidance moving into the end of FY2020 and 2021. Whilst also beating Revenue and EPS estimates by $133.29 million and $0.10, respectively, the company ultimately registered earnings of $0.34 per share over this period. Current shareholders can take solace in the fact that the company’s hero product, known as the Trans-Catheter Aortic Valve Replacement or TAVR, has shown stability in the reluctancy of hospitals to accept heart surgery candidates during the course of the pandemic. Potential investors can lay weight to the fact that the company is well capitalised on the back of strong performance up to the market selloff this year, alongside management’s competency in liquidity preservation and preventing value erosion. These points are coupled with satisfying ROA and ROCE that have enabled positive FCF for the company to date, thus also illustrating the entity’s capacity to generate additional earnings for shareholders into the future.

In light of this, we advocate that more evidence is required on a sales front and an acceptable valuation target, particularly relative to peer companies within the same domain, to provide an entry point where investors can realise capital gains on the back of the greater society’s dependence on innovation within the medical supplies and interventions industry. Thus, we are waiting for the right entrance on EW and here and will outline our neutral stance below.

Investment Thesis

We do have a neutral sentiment for EW, however feel that the entity can demonstrate the capacity to bolster earnings and continue along the sales trajectory with their TAVR markets. Thus valuation may undergo a correction alongside sustainable capital growth for shareholders moving out of 2020, but for now we are yet to see the evidence without the performance. The company is in a “prove it” stage, particularly based on valuation and slumped sales growth secondary to the market and health industry turmoil experienced this year. However, the vigorous track record in expanding sales and providing steady gains to shareholders provides the case for potential entry coming out of 2020, provided certain factors take place.

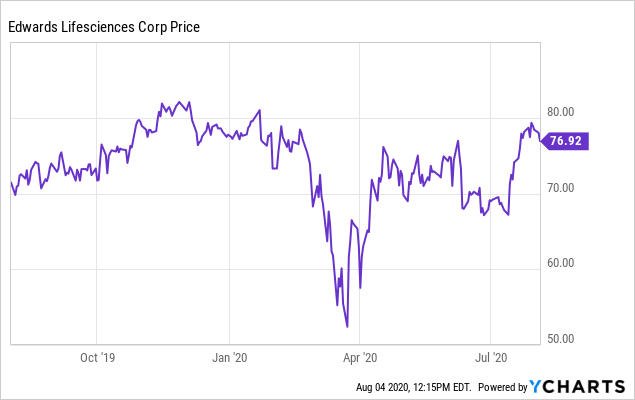

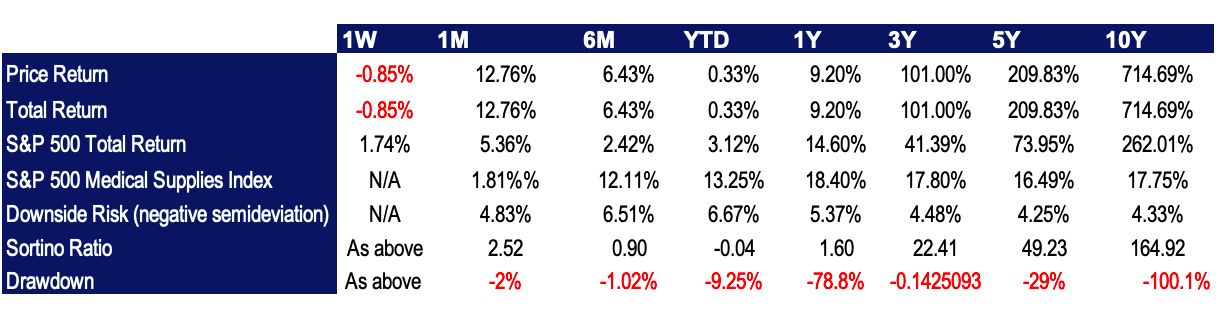

The company has seen exceptional growth to date on the back of the TAVR intervention alongside procedures pertaining to the mitral and tricuspid valves of the heart, a market which is anticipated to reach at least $3 billion in five years’ time. As such, the company has delivered over 100% in price returns to shareholders over the three-year period to date, with 4.48% risk towards the downside. This is aloft the S&P 500 (SP500)’s figures over the same period and has outpaced the S&P 500 medical supplies index (SPSIHE) by around 84% during this term.

Data by YCharts

Data by YCharts

To compare, this year investors have seen returns of only 9.2% with 5.37% downside risk; in stark contrast to previous periods. This is well below the SP500’s postings over the same time and even more so below the SPSIHE by 9.2%. Additionally, the Sortino ratio of 22.41 to 49.23 over the periods from 3-5 years illustrates that shareholders have realised a higher return for each unit of downside risk they have tolerated during this time. Such is the the case especially with long-term holders, 10 years plus for instance; however, in contrast, shareholders will be unpleased with the asymmetry in risk/reward from YTD, showing a ratio of 0.90 over the last six months, to demonstrate, on the back of a maximum drawdown of -78.8% for the previous single-year period and with the heightened downside risk mentioned earlier.

As markets have settled, we foresee a potential upside ratio of 20.3% based on this years returns to date, which brightens the medium to long-term horizon for players within that domain, however we will continue to scrutinise the downside over the next 1-3 months in order to obtain the best picture of what the outlook for the investors will demonstrate as further developments are made in the global Covid-19 case.

NOTE: Click on image for larger view.

Data Source: Value Line EW; Author’s Calculations

Additionally, valuation metrics do not sit favourably for the company at present, which is exactly why there is hesitancy from our end in pursuing a position at this point, as are discussed below. We have had EW on the radar for some time now, but we are waiting on the right flavour to present itself in order to pull the trigger.

In this analysis we will present two scenarios to gauge insight into potential outcomes, so that potential and current shareholders can make an informed decision on their own positions coming into the near future. We feel it is imperative to scrutinise ROE and our valuation using a two-stage FCFE valuation model so that a clearer picture is obtained in light of the potential for more uncertainty as more and more countries experience their second wave of Covid-19 cases.

NOTE: Click on image for larger view.

Profitability

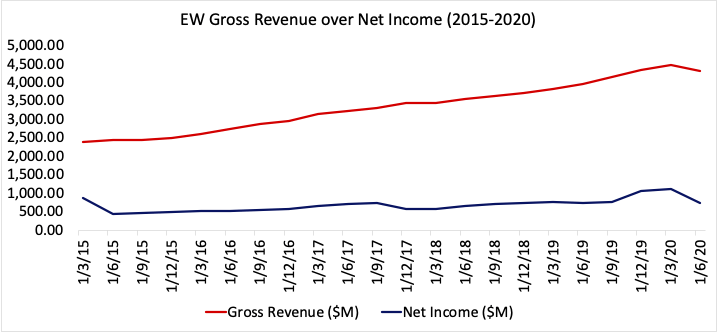

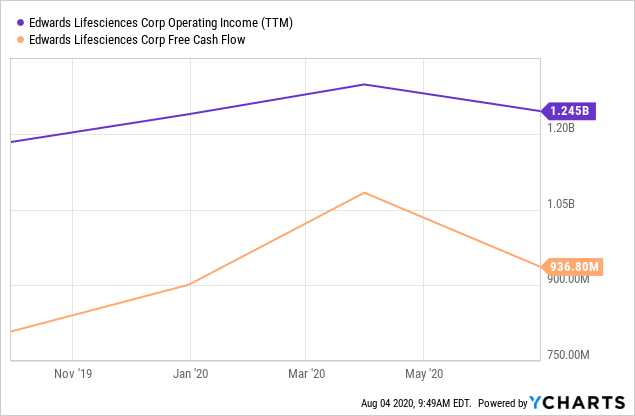

The company has shone in its profitability over the previous 10 years to date with CAGR revenue growth of 11.56% over this period. From the earnings report on July 23rd, the company has posted revenues of $925 million and enjoyed healthy gross margins of 74.97%. Gross revenues were down -14.9% from the previous period, although outshone expectations by around $133 million and the company posted a net loss of -$122 million for this quarter. EW has OCF of $1.27 billion and has remained profitable after meeting its obligations most recently eliciting FCF of $681.5 million, which registers a TTM FCF figure of $936.8 million. The company enjoys FCF margins of 15.76% on the back of EBIT margins of 28.85%.

Data Source: Value Line EW; Author’s Tabulation

In light of the recent slump in revenues, gross sales have grown 9.02% YoY alongside FCF which has seen an impressive 26.37% increase in this same period. OCF has shown a similar trend in increasing by 30.3% on the back of a concurrent increase of 35.5% in capital expenditures which registered a 7.82% proportion of sales using TTM figures, alongside 9.62% bump in reinvestment into net working capital YoY.

Data by YCharts

Data by YCharts

Sales over the years have been driven particularly on the back of their flagship product, the SAPIEN TAVR prosthesis, which has induced a disruption into the world of cardiothoracic surgery across the board. The device has been hailed due to its non-invasive nature and allows physicians to deploy a bovine-tissue derived valve into the aorta through either the femoral artery or intra-arterially through the chest wall, thus eliminating the risks and need for open heart valve heart surgery. Undoubtedly, in current trends of surgery and medical procedures in general, this aligns explicitly with the goals for the patient in receiving as conservative/non-invasive intervention as possible. Ultimately, recovery times and patient outcomes are heightened on the back of these factors.

Sales for TAVR amounted to $594.3 million exiting Q2, which is down around 12% from the year previous. This was driven in part by the fact elective and non-essential cardiothoracic surgeries have been put on hold in the wake of the Covid-19 pandemic, and equipment suppliers across the board have noticed significant reduction in sales on this point. The trajectory will surely continue north in the slow reopening of the economy post Covid-19. To further illustrate, transcatheter therapies governing mitral and tricuspid valve repair were also down around 11% this year from reports obtained from the company alongside their surgical structural heart segment, which registered sales of $160.9 million, a reduction of 26% over the single-year period. What is essential to also mention is that the company beat analyst estimates on all three of these fronts, albeit on the back of slumped YoY growth. Interestingly, the surgical structural heart also appears to be a cannibalised product as much of the reduction in sales is attributed to a shift towards the less invasive TAVR procedure, thus limiting the requirement for product sales in this segment.

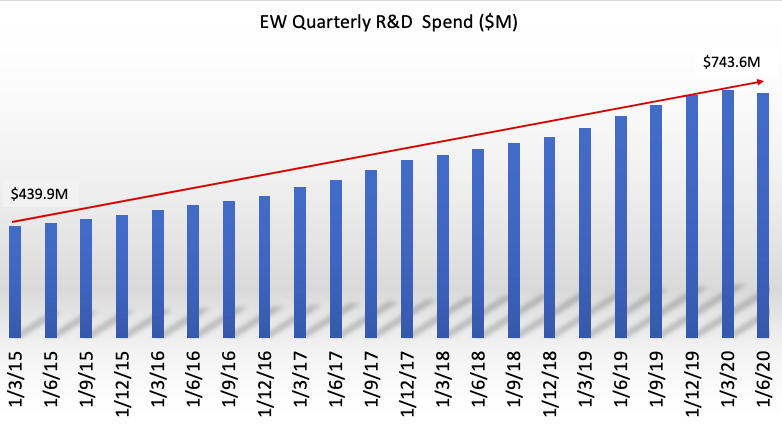

In light of these points, operating costs demonstrated a decrease of 8.7%, falling to $455 million over this period, which has assisted in the company enjoying the high margins mentioned earlier. However, this has had a moderately negative result on operating income which also contracted during the quarter. Whilst R&D expenditure fell this quarter, this was largely on the back of high R&D investment over previous periods, alongside reduced clinical trial activity within the sector this year as a result of the pandemic.

Data Source: EW 10-Q 2015-2020; Author’s Tabulations

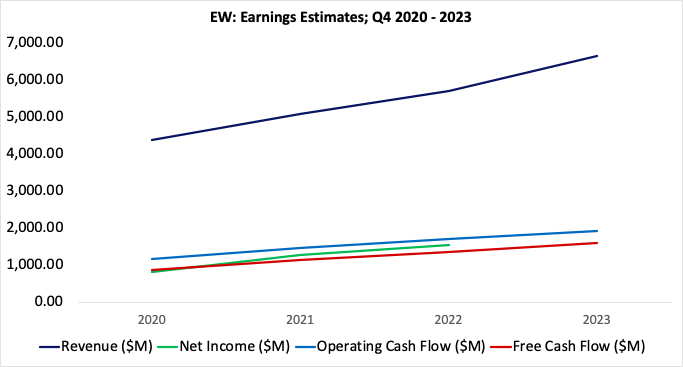

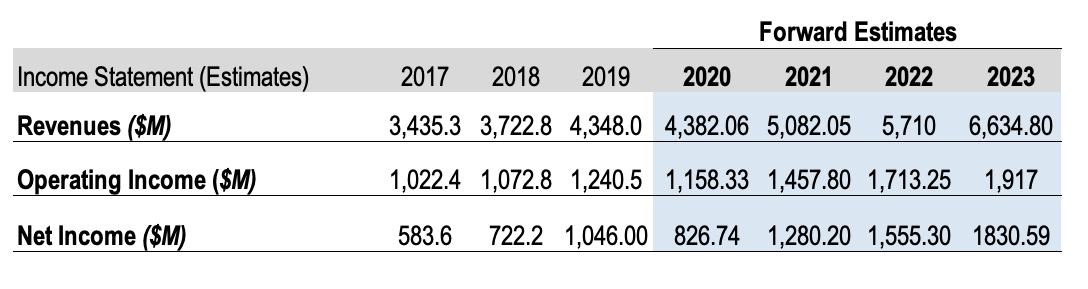

Future revenues are expected to climb by an average of 14.84% on an annual basis to 2023 which would register a CAGR of 4.6% over the same period, both figures obtained by linear regression from the consensus of analyst estimates. Additionally, the company is poised to remain profitable from a net income and FCF perspective, continuing a healthy average FCF growth of 23% over the same time period using the same approximation method, whilst cash from operations is estimated to follow suit increasing by 65% in 2023 (using the same method). Ongoing Net income increases will undoubtedly prop up the by case from an EPS perspective however the FCF figures are exciting and demonstrate the company’s capacity to generate ongoing returns to shareholders, much like the glory days for the company over the previous 10 years prior to the pandemic.

Data Source: Author’s Calculations, obtained from linear regression of the consensus of analyst estimates reviewed.

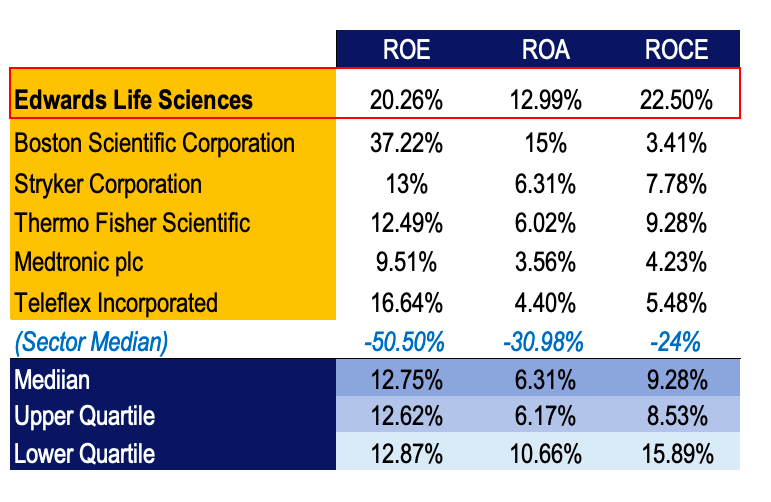

The company has delivered these results on the back of pleasing ROA of around 13%, which lies ahead of the 5 peer company’s we have used as comparables within this analysis except for Boston Scientific Corporation (BSX) at 15% but is well aloft the industry median of -30.98%. ROA is achieved by EW’s assets turning over ~72cents for every dollar held within the asset base, evidencing the company’s diligence in achieving returns from their investment choices. It is seen that the industry median is below this figure, at 0.35 as a measurement. Further evidence of the same is shown in extremely favourable ROCE of 22.5%, which has increased satisfactorily from 21.5% over the three-year period. ROCE is certainly a metric that we use in order to identify quality in valuation and capital return, because we find many companies who evidence growing and high ROCE to enable shareholders and the company alike to realise higher returns over the medium to long-term.

Data Source: Value Line EW; Author’s Calculations

ROE is also well above the meagre industry mean and also the peer median figure and pleasingly also lies within the upper 25% of the comparables listed, particularly above Thermo Fisher (TMO) which we feel is currently a strong buy case as previously mentioned in a previous analysis, found here. We feel the ROE is a an accurate reflection for investors to take note of considering the company’s low reliance on leverage and management total debt level and certainly an indication of the company’s profitability as a function of shareholder equity.

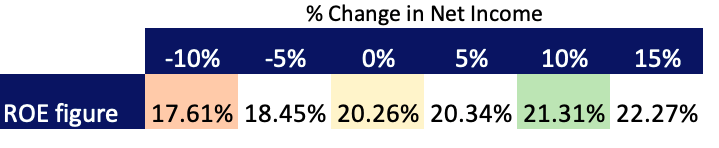

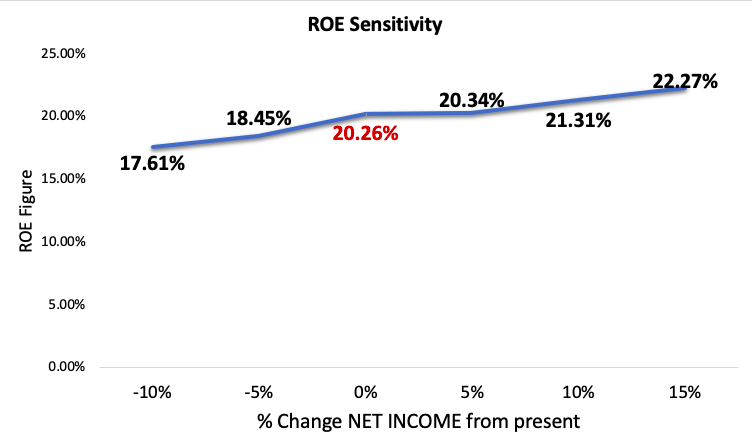

NOTE: Click on images for larger view.

Data Source: Author’s Calculations

In our downside case, we see a 10% decrease in net income from the current TTM figure resulting in a 13% change in ROE expectations for shareholders, assuming the company retains the same shareholder equity. In contrast, a 10% increase in net income will only yield a 5.16% increase in ROE, thus, from our estimates ROE is more sensitive to the downside with any further decrease in revenue from the current figures. This presents as risks to shareholders however the company is certainly on the trajectory for growth in net income over the coming periods, nonetheless this will be an excellent stress test for the company to understand how it will perform on a profitability basis coming out of 2020.

Solvency

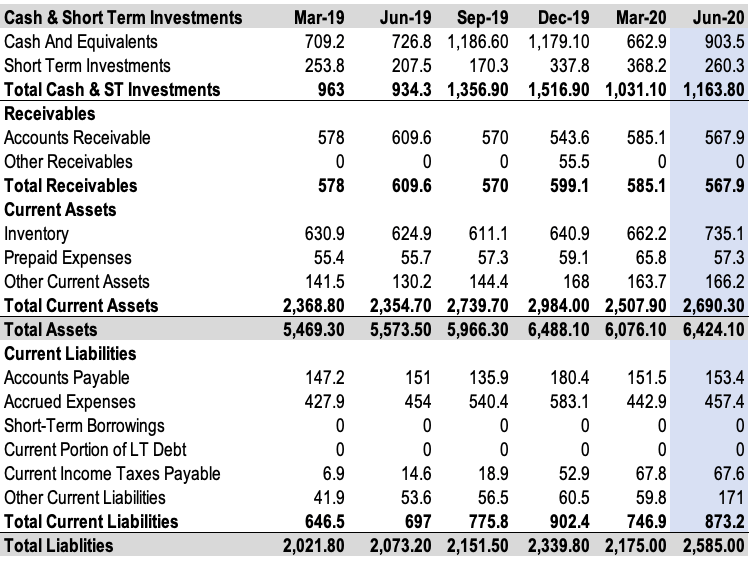

From a solvency perspective, the company remains well capitalised moving out of 2020 and the company has provided guidance of around $4.5 billion in sales over the next year and is confident in around $1.2 billion in revenues as a strong drive forward into Q3 & Q4 of this year. Current earnings figures provide adequate coverage over short-term obligations thus the company should meet its obligations in this horizon as they fall due, showing a current ratio of 3.08x coverage and inventory seems well managed having increased at an average of 32.4% over the previous 3 years, thus performing an acid test on short-term solvency the company shows a quick ratio of 1.98x in the case inventory is not highly marketable and liquid moving forward.

Moreover, ongoing interest payments are well covered at over 60x coverage whilst Debt/FCF is at. 0.87 illustrating the company’s solid cash position if it were to accelerate its debt payments on $684.5 million in total debt and thus free up capital for additional R&D expenditure or net working capital, for example. The company also has corporates notes on issue under the title EDWARDS LIFE. 18/28 with a Baa2 rating, currently trading at a premium of $122.11 and were released on 15/06/2018 on a volume of 600,000,000 issues. The notes pay a fixed coupon of 4.333% semiannually, with the next payment due on 15th December 2020.

EW Current Position:

Data Source: EW 10-Q June 2020; Seeking Alpha

Equally as pleasing is the company’s cash per share which shows a figure of 1.87, highlighting the company’s liquidity within the asset base. Undoubtedly, the citadel surrounding the company from a solvency perspective is quite wide and management have demonstrated excellent capacity to muster out the remainder of any market turmoil coming out of 2020 and into 2021 and beyond.

Valuation

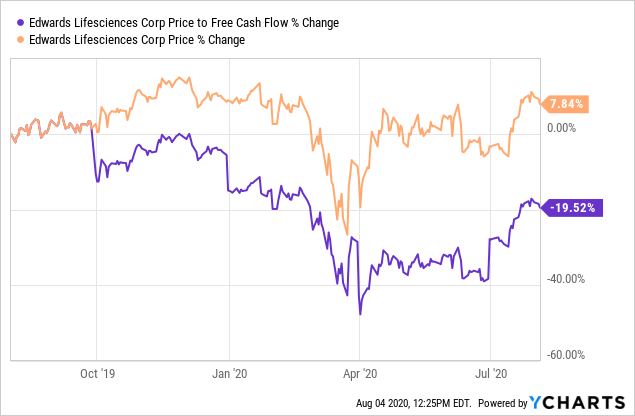

We feel that EW must evidence a correction in valuation to support a recommendation of a buy case. The company is trading at a significant premium as observed by a number of metrics built into the valuation model in this analysis. For instance, the entity presently has P/FCF of 52.08, which is reasonably high however not unexpected considering the growth in capital expenditures and net working capital over the most recent single-year period. This figure has shown a change of around 7.84% and in our opinion is an appropriate measure to factor considering the relatively low and stable debt recordings, thus is an accurate snapshot of the company’s ability to generate additional revenues moving out of 2020.

Data by YCharts

Data by YCharts

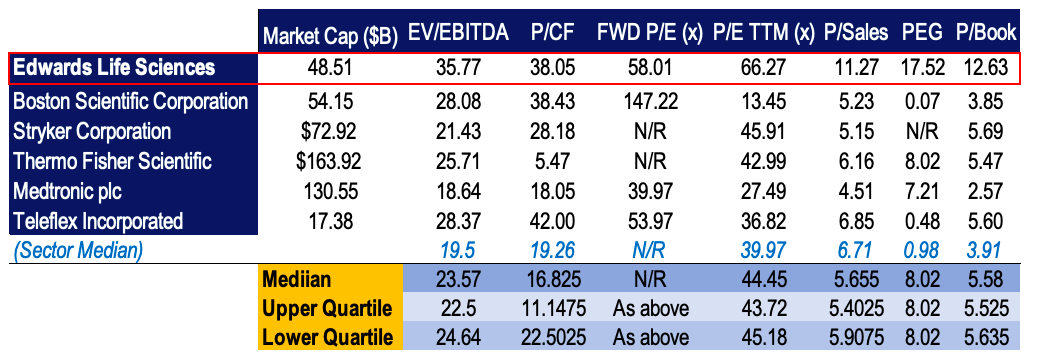

Furthermore, the company trades at a premium on a TTM P/E multiple of 66.27x well above the sector median and lies within the 75th percentile of the comparables listed. Additionally, on a P/Sales front, the market has demonstrated high sales expectations from the company as a function of share price on a figure of 11.27 which again lies within the lower quartile in this instance, however does provide some weight to the suppositions from market participants who foresee the future of the company. Similarly, on a P/CF front, the company seems overvalued at a figure of 38.05, which is exceptionally high in comparison to the industry median, TMO and Medtronic Plc (MDT), by way of example. Considering the company’s market capitalisation of $48.51 billion, further evidence of overvalued territory is seen in the EV/EBITDA multiple which is the highest out of the five comparables listed and the median industry figure. Thus, on a multiples and ratio front, we feel the company is overvalued here and needs to evidence consistency in sales figures particularly within their TAVR markets to justify these premiums moving forward, more so as the market highlights large expectations from the company on the same from these figures.

NOTE: Click on image for larger view.

Data Source: Author’s calculations; Value Line EW

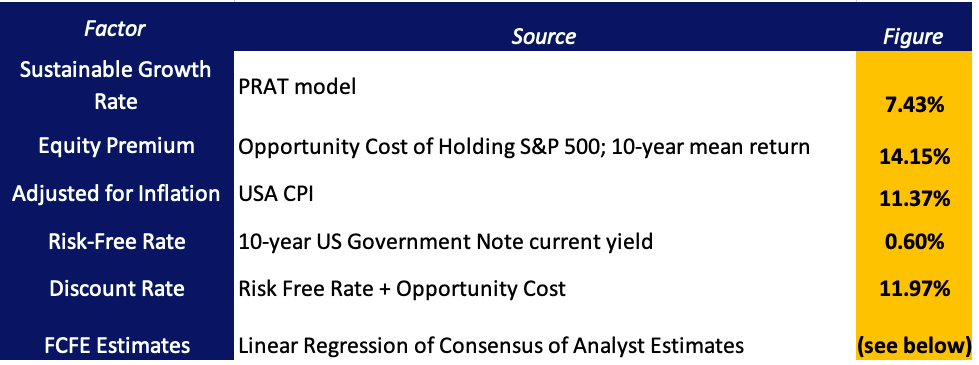

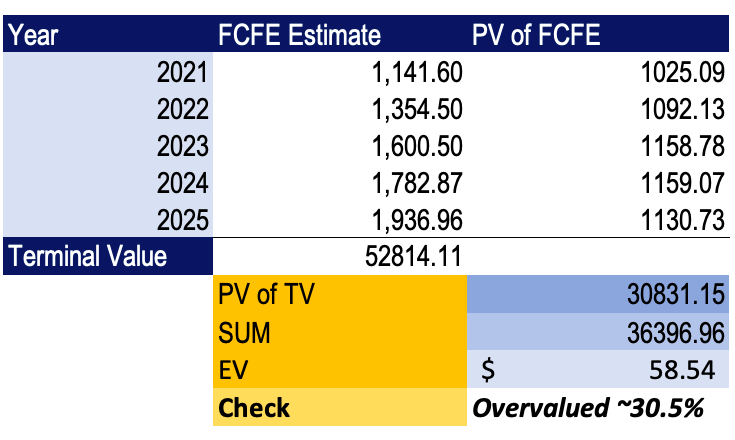

To add weight to the valuation model, we have analysed FCFE estimates and obtained figures using linear regression on the consensus of analyst estimates to 2025. As the company is in an easily disrupted industry, and markets are showing ongoing signs of uncertainty, we have forecasted to 2025 using the above methodology. We have assigned the growth rate to perpetuity using the PRAT model of DuPont as a conservative measure to arrive at a figure of 7.43% and a terminal value of $52814 million in year five.

NOTE: Click on image for larger view.

Data Source: Author’s Calculations

On the valuation model built above, the stock appears undervalued by around 30.5% at an intrinsic value of $58.54. We tend to agree at this stage particularly on the back of other valuation metrics suggesting the same and the stock does not seem to be heading south towards the $60 mark any time soon on current momentum. This figure will be watched very closely over the coming weeks and even months, where we will use the inputs for the model to provide consistency against other valuations for additional companies. We present our base case, downside case and upside case for sensitivity to the growth figure on valuation below.

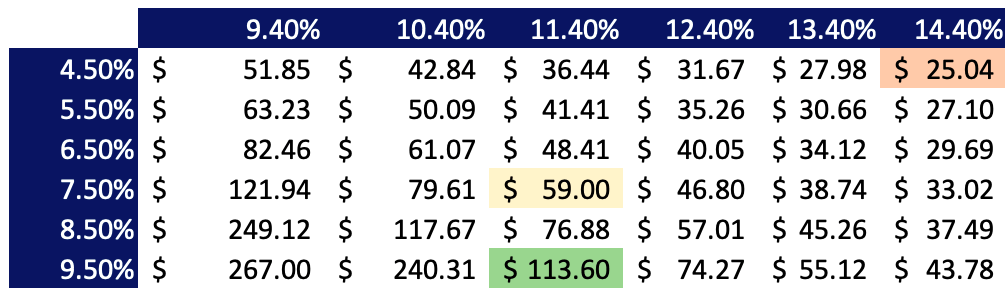

NOTE: Click on image for larger view.

Data Source: Author’s Calculations

We foresee an increase in the perpetual growth rate of ~2% resulting in a significant change in our intrinsic valuation, thus highlighting the sensitivity of the value to this metric. This represents our upside case in valuation here. It is an important number for investors to watch over therefore, particularly as the company is poised for an average of 18-20% growth in FCF over the next few years and has delivered around the same in CAGR of FCF over the previous three-year period to date.

Conversely, by this analysis, if perpetual growth of FCFE were to reduce alongside a corresponding hike to the discount rate, then we would deduce that the stock is extremely overvalued on this valuation model, thus would be looking to allocate our capital elsewhere. We believe that EW is still overvalued on this front, as even if we are wrong in two out of the three scenarios, the stock is still overvalued up until a growth rate of 8.5%, by our analysis.

Risks

The are risks to both shareholders and the company. To shareholders, we see in our downside case that a reduction in net income below the current TTM figure is more sensitive to expansion of the same. Additionally, from a price returns perspective, the firm has shown us downside risk in the ranges of ~5-7%, which we do not see favourably on. Ideally, we would like to work with a figure that is closer to 4%, as has been our track record to date. We feel that investors can achieve a greater asymmetric risk/reward towards the upside around about this figure in equities. Moreover, we don’t see investors benefiting from the additional exposure to the downside risk, as the sortino ratio highlights for the 1-year, YTD and 6 month price returns. In fact the figure is quite disappointing and we need more from the share price here to argue successfully for an immediate entry.

The company’s board is also authorised to issue up to 50,000,000 shares of preferred stock without common shareholder approval and to set the terms of which the preferred stock will be issued. Undoubtedly the addition of more primary claimants alongside the bondholders presents a risk to the potential earnings shareholders will see and will remove access to capital from the company’s end. Moreover, this issuance of stock would make M&A activity seem less attractive from potential buys and receivers of the same.

Furthermore, without clear indication of when elective cardiothoracic surgery will be permitted to continue within the global healthcare system to a level and standard as was prior to Covid-19, there is no saying as to what ongoing impact this may have on the TAVR line, much less the company’s additional cardiac and critical care markets. From all accounts, there is also an acute response to those exposed to the pathogen and concurrently receiving cardiac interventions which is not completely understood or recognised, however it has meant a large push away from any form of intervention for these patients thus the results the company seeks in pursuing to extrapolate the benefits of their non-invasive procedure seem unlikely to kick off very soon.

On this point, the company’s exposure to its hero product TAVR means that any disruption to the technology will alter the demand and supply of the device thus without ongoing diversification into alternate intervention classes there is inherent risk that the company cannot sustain gaining market share within that particular domain. This point is offset by the ingenuity of the product however there are ever changing thoughts and concepts on how to perform stent/valve type procedures, showing risks to the company.

At this pace, we would foresee a similar situation for the company as it was heading into 2020 once the pandemic has settled. It is certainly well positioned in its cash position, however, large, one-off items associated with Covid-19 that will impact the income statement will also play havoc on shareholder returns as the market continues its flight to quality in weeding out weaker firms. For example, the firm has reached a settlement with the Abbott laboratories (ABT) following a dispute over its Pascal sales in the beginning of July this year, consequently ABT will receive a one-off payment in addition to ongoing payments derived from Pascal sales through until 2025 in addition to a potential sales milestone payment the year after. EW must surely look to preventing such matters from occurring again.

Conclusion

This is the time for potential investors to flag the above points made throughout the entirety of this report as a stress test for management and the company’s performance moving out of 2020 to understand the growth strategy and to enter at a more correct valuation. At this stage, we cannot advocate for entry at the current valuation, particularly in relation to the comparable entities we have included as an alternative source to allocate capital to maximise returns. What is promising is the upside potential ratio of ~20% which we believe is accurate from historical earnings, however it may be too uncertain to call the same with the new waves of Covid-19 appearing now.

In the medium to long-term we have no doubts that EW will be around however it is the valuation and lack of certainty around their markets in the shorter term that leaves us neutral on the company. Providing the company does pass the so-called stress test mentioned above and continues to deliver high ROCE and ROA through asset turnover, we would anticipate that once the economy and health system slowly enters recovery phase (no pun intended) and cardiothoracic surgery commences again to the critical masses, EW will shine again and continue their innovation in the domain. Time for the company to prove it to us.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}