Few efforts to improve international tax governance have drawn quite as much ire from such a diverse group of critics as the EU’s list of non-cooperative jurisdictions. In late 2017, the European Union began publishing a list of those that were not doing enough to curb international tax evasion and profit shifting. The list immediately drew criticism from tax havens for being arbitrary and overly punitive and from nonprofits fighting for international tax justice for being too limited in scope and for giving European territories a pass.

Unperturbed by the criticism, the EU has been running its list for over two years and claims that it has led to “real improvements in global tax transparency.” Much of the purported success of the listing exercise is based on the fact that many countries have graduated off of it since originally being named and shamed. Jurisdictions are taken off the list when they have fulfilled various tax governance targets set by the EU’s Code of Conduct Group for Business Taxation, a group of bureaucrats who have the unenviable task of scouring through dozens of legal frameworks looking for gaps that corporations and people can use to avoid paying tax.

But counting the number of boxes that the EU ticked to remove jurisdictions from its list doesn’t give us the full picture of the listing process’s impact. To really understand the impact the EU’s efforts have had on international tax governance, we first need to know what has been going on in the jurisdictions that the EU chose not to review.

In a new working paper, I investigate the impact of the EU’s entire review process on the very standards it was aiming to enforce. Prior to the release of its first list, the EU developed a set of criteria to score jurisdictions across three dimensions: how close their economies were tied to the EU, how big their financial sectors were, and how well governed they were. Jurisdictions that scored high enough across all three dimensions were reviewed carefully by the Code of Conduct Group and, if found wanting, were given the chance to implement changes. Nearly 50 jurisdictions that committed to improving their tax governance by the end of 2018 were added to a “grey list” while 17 that were considered non-cooperative were added to a blacklist.

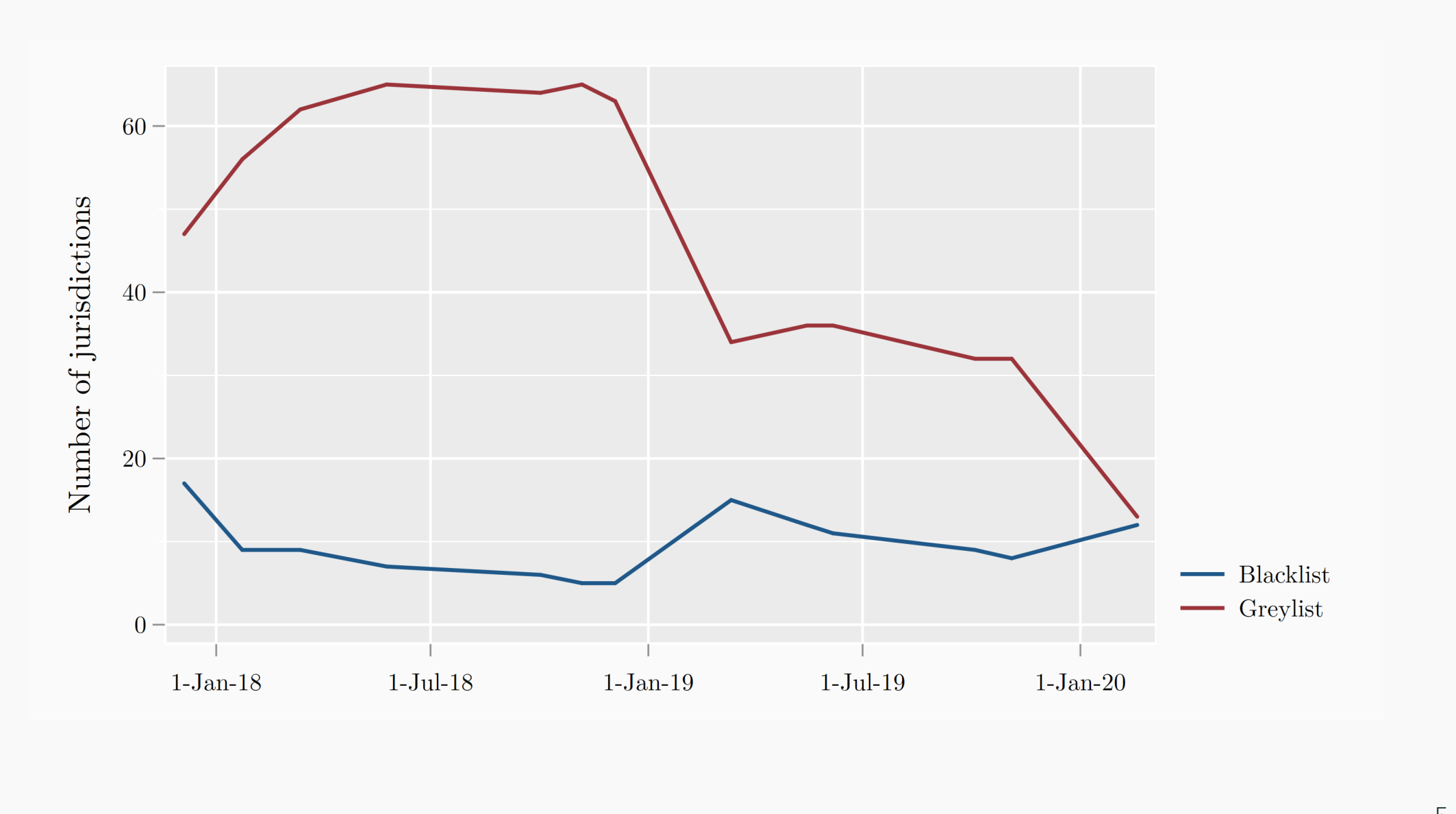

Figure 1. The evolution of the EU’s listing exercise over time

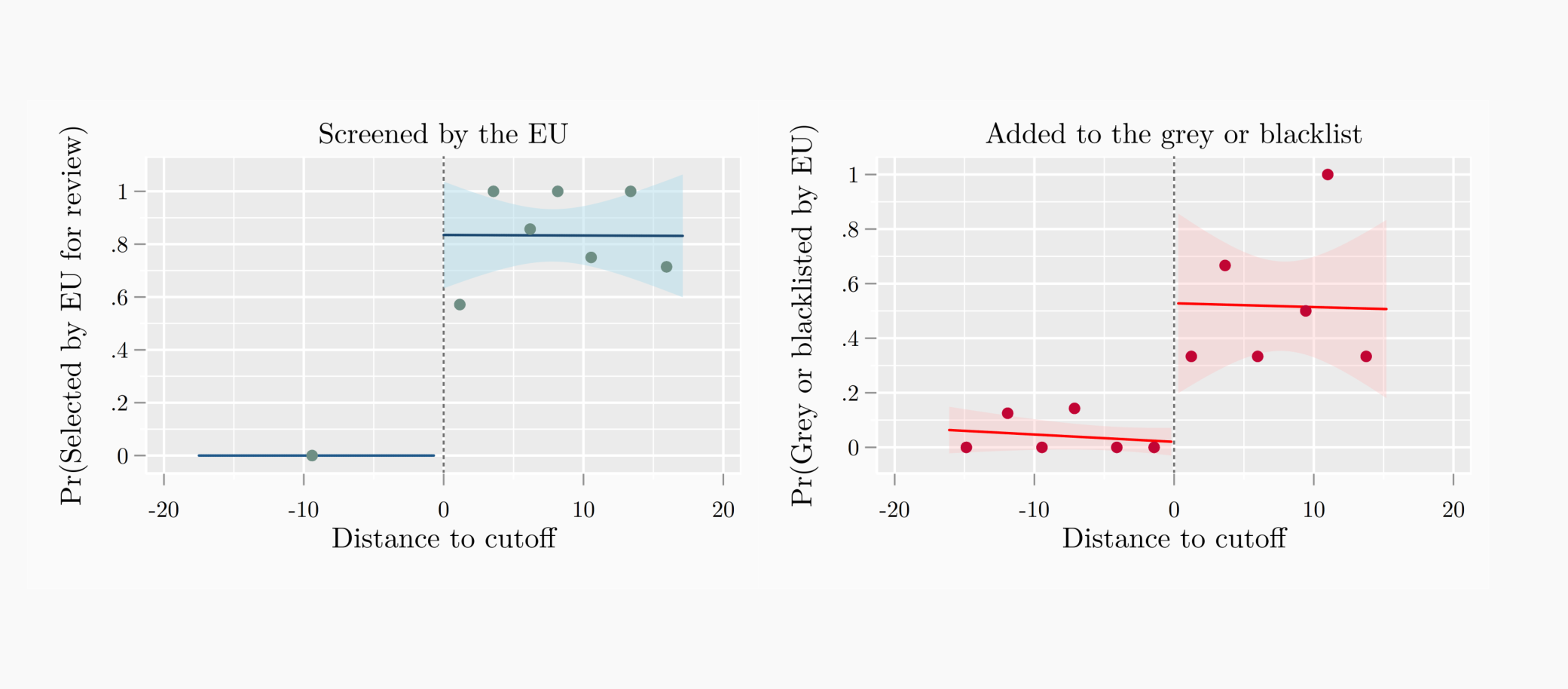

The fact that the EU used a scoring system allowed me to compare jurisdictions whose scores just barely made them eligible for being reviewed by the Code of Conduct Group to those who were just barely ineligible for being reviewed. In the paper, I use a regression discontinuity design (RDD) framework, which makes it possible to understand what the net impact of the Code of Conduct’s review process (and the subsequent grey and blacklisting) has been on jurisdictions close to the cutoff for selection.

Figure 2. Jurisdictions that barely scored above the EU’s selection threshold were much more likely to be screened and, eventually, added to the EU’s list

Notes: Each figure shows the results of a local linear regression-discontinuity estimate, without controls, of the (reduced form) effect of crossing the EU selection threshold on the probability it was eventually selected and also the probability that it was added to either the first grey or blacklist published in December, 2017. Data points are binned, with bins chosen using mimicking variance evenly-spaced (ESMV) method (Calonico, Cattaneo, and Titiunik 2015).

The ways in which the EU moved the needle and the ways in which it didn’t

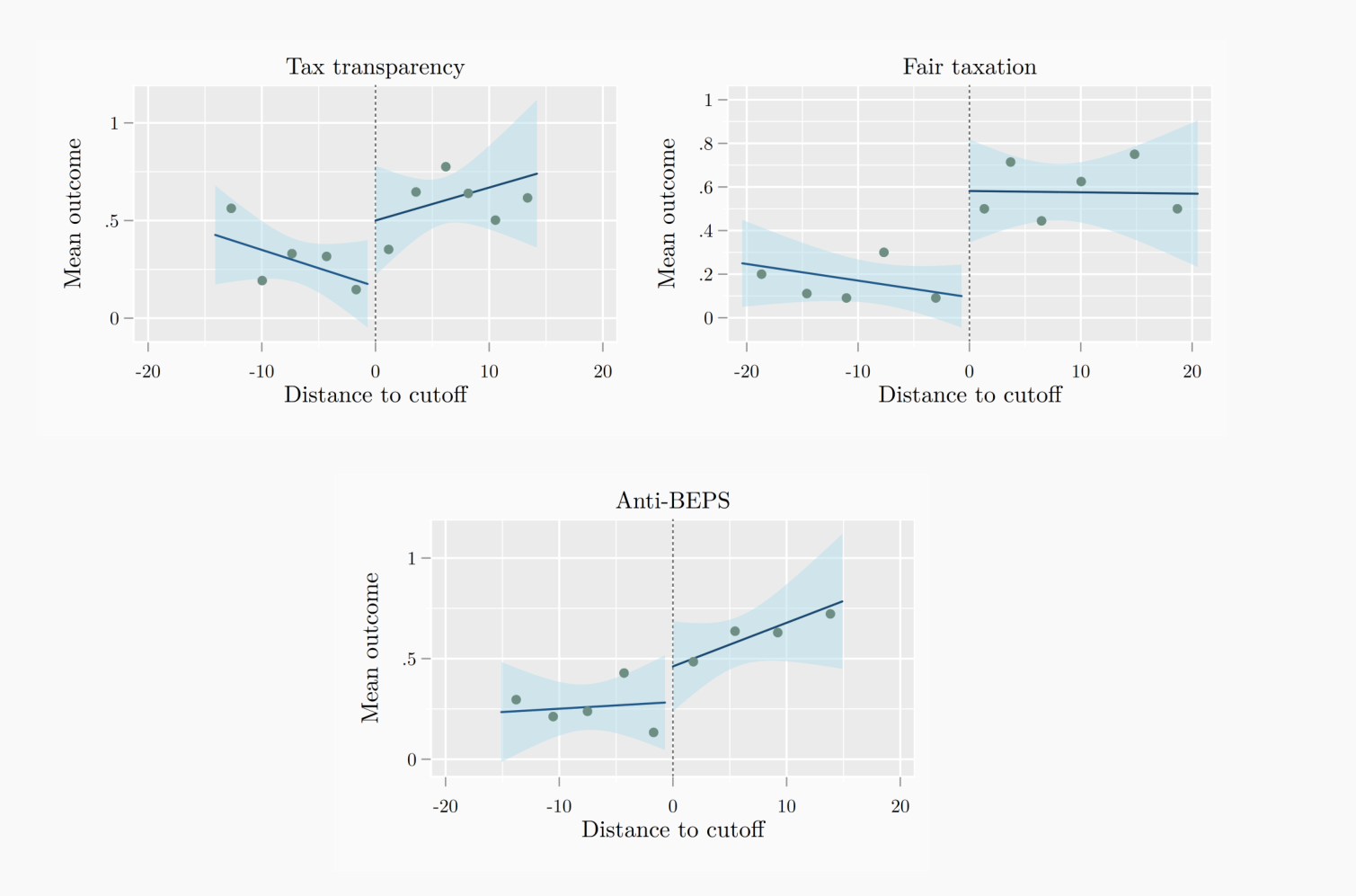

The jurisdictions who just passed the threshold were substantially more likely to end up on one of the two EU lists, so it is clear that the Code of Conduct group paid more attention to them. But the evidence behind transformative changes in international tax governance is more muted. To understand what the effects of selection into the Code of Conduct’s review were, I looked at a wide range of outcomes, grouped together under the categories of Tax Transparency, Fair Taxation and Anti-BEPS (actions taken towards the Base Erosion and Profit Shifting agenda).

Figure 3. The EU review and listing process had a significant impact on outcomes related to fair taxation, but selected jurisdictions did not see significant increases in the average number of reforms related to tax transparency or anti-BEPs

Notes: Each figure shows the results of a local linear regression-discontinuity estimate, without controls, of the (reduced form) effect of crossing the EU selection threshold on each of the three main tax governance groups of outcomes. Each measure (Tax Transparency, Fair Taxation, Anti-BEPS) is an average of tax governance outcomes within the group. 90 percent confidence intervals shown. Data points are binned, with bins chosen using mimicking variance evenly-spaced (ESMV) method (Calonico, Cattaneo, and Titiunik 2015).

I found that the impact of the EU review and listing process on the average number of Tax Transparency outcomes was mixed. Overall, there was no significant impact, nor was there consistent evidence that selected jurisdictions were more likely to successfully implement automatic-exchange of information (AEOI) agreements, which allow tax authorities to automatically share information on bank accounts held by each other’s citizens to better understand who is hiding cash offshore. However, there was some evidence that selected jurisdictions were more likely to implement an older, more limited model of information exchange, known as exchange-of-information on request (EOIR).

One of the biggest successes of the EU review and listing process was in expanding the set of jurisdictions that had their tax regimes reviewed and potentially-revised to reduce the chance that they unfairly allowed multinationals to shift profit there, to the detriment of other countries. Selected countries were between 68 and 90 percentage points more likely to have had a tax regime reviewed by either the Code of Conduct Group or the OECD’s Forum for Harmful Tax Practices and to no longer have any harmful regimes present. This in itself is a win for transparency around international tax rules and one of the benefits the EU routinely takes credit for. However, we only see harmful regimes where the EU and OECD looked for them, so while transparency did improve for these jurisdictions, we cannot be sure that jurisdictions that weren’t subject to review didn’t also dismantle their harmful regimes.

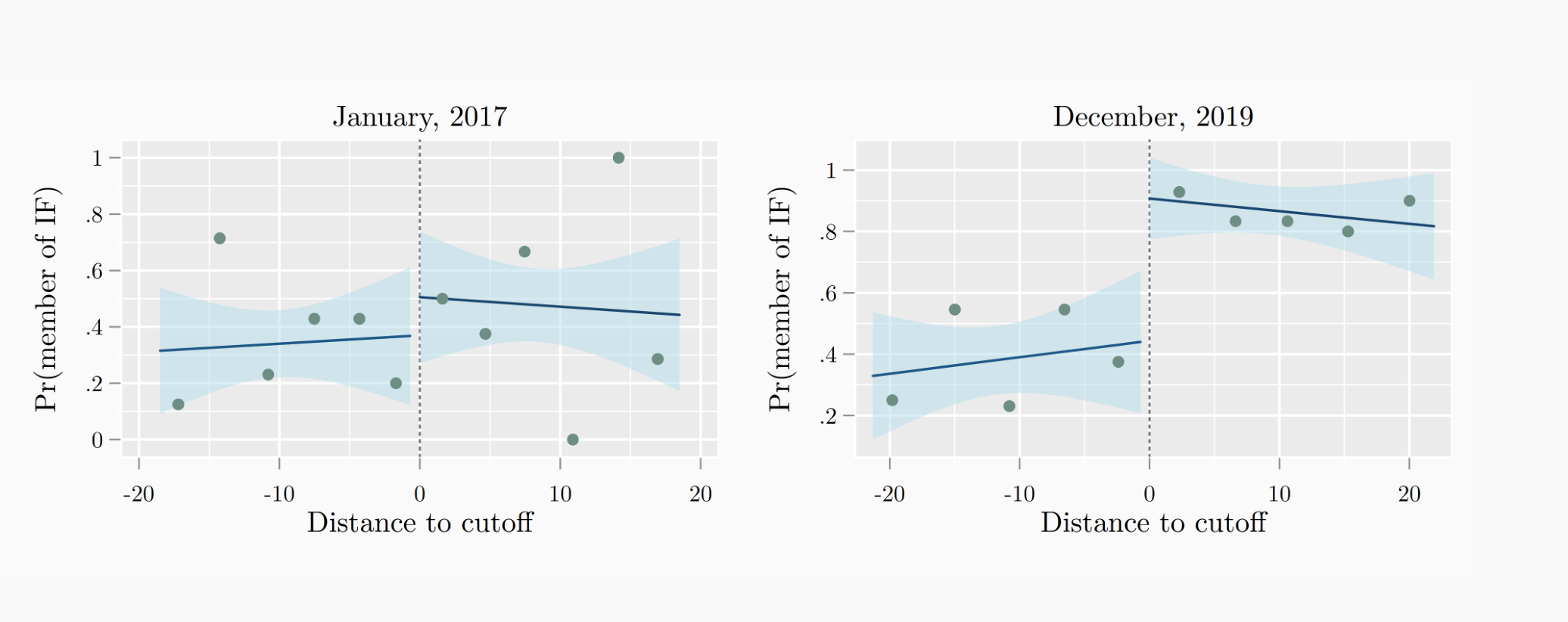

Outside of improved accountability around harmful tax practices, there wasn’t strong evidence that the EU moved the needle on efforts to implement the OECD’s BEPS Minimum Standards, at least not enough to be statistically detectable. However, jurisdictions that were selected were almost guaranteed to have joined the Inclusive Framework (IF), a forum dedicated to implementing the Minimum Standards and to deliberating new international tax rules. Back-of-the-envelope calculations suggest that the IF is about 15 percent bigger thanks to the EU’s intervention. This has had the knock-on effect of increasing the number of jurisdictions reviewed by the Forum for Harmful Tax Practices, crowding in attention on harmful regimes rather than crowding it out.

Despite being slightly larger, the representation of poorer countries in the Inclusive Framework wasn’t improved by the EU listing, mostly because the EU excluded least developed countries (LDCs) from consideration, due to the fact that they face capacity constraints in implementing many of the desired reforms. There have already been questions about the degree to which members of the IF, particularly poor countries, have had meaningful participation in the ongoing modeling of new international tax rules aimed at clamping down on multinational tax avoidance.

Figure 4. There was no significant difference between selected and non-selected jurisdictions when the Code of Conduct Group began its work, but over time, selected jurisdictions were substantially more likely to join the OECD’s Inclusive Framework

Notes: Each figure shows the results of a local linear regression-discontinuity estimate, without controls, of the (reduced form) effect of crossing the EU selection threshold on each of the three main tax governance groups of outcomes. 90 percent confidence intervals shown. Data points are binned, with bins chosen using mimicking variance evenly-spaced (ESMV) method (Calonico, Cattaneo, and Titiunik 2015).

Why wasn’t the listing exercise more successful?

In many ways, the EU’s list moved the needle more than might have been expected. But it wasn’t a knockout success. Many of the criticisms of the effort remain, from the institution’s reluctance to sanction their own members or larger, more impactful economies like the United States, to the EU’s inability to quickly implement aggressive countermeasures against tax havens on the blacklist. While some research suggests that companies and investors paid attention to who ended up on the EU blacklist, macroeconomic data on foreign direct investment or offshore banking assets suggest that listed jurisdictions did not pay a high financial price for being named and shamed.

As some European countries begin to consider prohibiting companies with subsidiaries based in blacklisted jurisdictions from being eligible for COVID-19 economic relief, we may start to see more companies and countries taking the list seriously. That’s great news if you already like the EU’s blacklist, but bad news if you think that the list is mistargeted or just reinforces existing political power imbalances in the international tax debate. As a projection of Europe’s power, the listing exercise can be counted as a partial success, but in moving the needle in making the international tax system more fair, it clearly has some way to go.

{kind=link}