Investment Thesis

electroCore share price performance since IPO. Source: TradingView.

electroCore share price performance since IPO. Source: TradingView.

electroCore (NASDAQ:ECOR) has been a crushing disappointment for its investors since its June 2018 IPO. Despite the promise of its FDA approved, non-invasive treatment for migraines – gammaCore – cleared for the acute and preventive treatment of migraines and episodic cluster headaches – there is now significant doubt as to whether it will be able to retain its listing on the Nasdaq given that the stock currently trades below $1, and a reasonable chance that electroCore will have to cease operations altogether.

Whilst these 2 events remain a possibility rather than a reality, however, electroCore remains an interesting, albeit extremely risky, investment opportunity in my view.

Medical devices are notoriously hard to bring to market, but when they do gain a foothold, can often go on to perform spectacularly well – witness the explosive growth of companies like DexCom (DXCM) and its continuous glucose monitoring devices (see my note here), or Medtronic (MDT), or even novel cancer therapy developer NovoCure (NASDAQ:NVCR) (see my note here), not to mention the vaping industry.

Although gammaCore appears to be a convenient and fast acting migraine treatment that has demonstrated clinically meaningful value both in trials and within a real-world setting, electroCore has simply not been able to convert its very high marketing spend into comparably high sales.

In 2018 and 2019 respectively the company spent $42.5m and $35.4m on SG&A yet delivered just $0.93m and $2.4m of sales. Although we can see the trend is in the right direction, it is also clear that, with just $15.6m of cash available, the company is going to have to embark on a radical program of change in order to preserve its listed status, and indeed its status as an ongoing concern.

A new management team has come in to try to turn the company around. In September last year Daniel S. Goldberger was appointed electroCore CEO, joining from Repro Med Systems (NASDAQ:KRMD), a medical device company that has performed extremely well for investors over the past 12 months despite trading at <$1 for many years prior.

electroCore has also said goodbye to outgoing Chairman Carrie Cox – replaced by independent board member Michael Atieh, another biotech smallcap veteran – and 2 more members of Senior management, who have been replaced by executives with the necessary turnaround experience, Goldberger told analysts on the company’s recent Q120 earnings call.

Although Q120 results continued – and even accelerated – the trend of growing sales versus shrinking costs, the gap between the two still appears to be insurmountable, with the company losing another $8m in Q120, whilst its accounts payable figure also grew from $2.6m to $5.2m between 2018 and 2019.

electroCore has a purchase agreement in place with Lincoln Park Capital giving it the right to sell up to $25m of stock to Lincoln Park, which ought to keep the company solvent until the first quarter of 2021 at least. The company has been scrambling for various different types of funding over the past year, seemingly unable to find a white knight backer to provide the long-term sustainability the company needs. And who could honestly blame funders from backing away from the company at this time?

Despite all the grim news, however, I am still inclined to wonder if the company is just one or two catalysts away from turning its fortunes around.

As recently as late September 2019, electroCore’s share price leapt from $1.5 to $5 – nearly making the company the most unlikely of “5-baggers” – before collapsing again after an FDA request for further information and analysis relating to its attempt to gain clearance to use gammaCore for prevention of episodic migraine. Today, the company has no clinical trials ongoing. An application for an Emergency Use Authorization from the FDA to use gammaCore to treat COVID-19 patients with respiratory problems also saw the share price gain 80% in April.

Opportunities to make 500%+ gains on a stock in a matter of days are extremely rare, hence the attraction of electroCore to risk-on investors. In the rest of this article I will look at what has gone wrong for the company, what it may be able to do to put matters right, and assess the likelihood of it prospering versus the prospect of ceasing operations altogether.

An interesting strategy may be to buy and hold the stock. Since we know that the company has enough funding until next year, and the price cannot realistically drop much lower, there is a form of downside protection in place (unless the stock is delisted), and there is evidence that even a small catalyst or piece of good fortune can move the share price by a triple-digit percentage.

Despite all the signs to the contrary, I can’t help but feel a little bullish about electroCore’s prospects, and using my own financial forecasting, can even see a path to profitability by 2025. Risk-off investors, however, should probably run a mile from this stock.

Company Overview – what went wrong for electroCore?

At the time electroCore IPO’d, despite losses that were considered typical of an early stage medical device developer ($25.9m in 2017 and $15m in 2016 according to the IPO prospectus) the company looked promising. gammaCore was the first FDA-cleared prescription-only vagus nerve stimulation, or VNS, therapy for treatment of migraines and cluster headaches (“CH”), administered in discrete doses using a proprietary, simple-to-use handheld delivery system.

The Vagus nerve is the longest cranial nerve in the body, exchanging information between the visceral organs and the brain. gammaCore stimulates fibers in the vagus nerve using a proprietary high-frequency burst wave-form that is therapeutically relevant for neurotransmitter modulation, and also reduces inflammatory cytokines, to an extent comparable to commonly prescribed current standard of care treatments such as selective serotonin reuptake inhibitors, serotonin norepinephrine reuptake inhibitors, GABA analogues, acetylcholinesterase inhibitors and triptan medications.

The total addressable market for gammaCore also looked exciting. Migraines affect 12% of the adult population globally and there are ~36m migraine sufferers in the US, 60% of whom are dissatisfied with, or have contraindications to current standard-of-care treatments, according to US Pharmacist (quoted in electroCore’s IPO prospectus). electroCore estimates the TAM for its migraine treatment to be in the region of $3.8bn.

Cluster headaches (“CH”) affect 350k people in the US, with 225k seeking treatment every year from headache specialists and, according to a market research survey, 87% of CH sufferers expressed dissatisfaction with currently available treatments in 2018. electroCore estimates the CH market to be worth around $400m.

An absurd pricing strategy

As somebody who has suffered in the past with CH, I can say that at the times when my migraines were most severe I would unhesitatingly have tried a treatment such as gammaCore (and I am sure this would be true for most CH sufferers and, or people who suffer from more-than-occasional migraines), that is until I researched electroCore’s pricing strategy.

According to these very insightful blog posts from The Daily Headache, the gammaCore device costs $600 per device, which does not seem unreasonable, until we learn that the device needs replacing every month, notwithstanding the fact that technically and scientifically speaking, there is no need to replace the device so often. electroCore claims that the device needs “refilling” every month, but in fact, the company sends a brand new device each month, the blog posts reveal.

Without insurance, then, gammaCore will set you back $7,200 per annum, which seems frankly ludicrous and provides a very simple explanation (to my mind) as to why the product has not delivered the sales volumes expected of it. electroCore does offer 2 months of free use if patients agree to take part in a follow-up study, but to qualify for the study, they must be suffering from episodic CH.

There is also co-pay assistance of $100 for each product purchase for qualifying users, and of course, physicians can prescribe gammaCore and insurers can foot the bill, but insurers’ coverage of medical devices is not comprehensive and users are likely to end up covering ~40% of the costs.

When I read that the Daily Headache poster was having to skip meals in order to meet the costs of her gammaCore migraine treatment, I am not at all surprised that electroCore finds itself in the position it is today!

Where did the marketing money go?

The next question is how the company managed to burn through a $78m marketing spend in 2 years, only to deliver just 2 deals of note.

The first deal, or agreement, is with the National Health Service (“NHS”) in the United Kingdom, where the National Institute for Health and Care Excellence (“NICE”) has recommended the use of gammaCore for acute and preventive treatment of cluster headaches in adult patients, across the National Health Service. On the Q120 earnings call Goldberger revealed the NHS intends to extend its innovation technology payment program with electroCore until September 2020, which Goldberger added:

makes gammaCore eligible for the new medtech funding mandate mechanism, which could lead to long-term sustainable reimbursement of gammaCore.

in Q120, gammaCore earned $245.5k, or 33% of its total revenues, in the United Kingdom as a result of this arrangement.

The second agreement relates to a contract secured with the Veterans Administration (“VA”), and the Department of Defense (“DoD”), which drives the bulk of the $457k the company earned in the US in Q120. According to electroCore’s Q120 10Q, approximately 400,000 patients saw a VA healthcare provider in 2018 with headache concerns (data from the American Headache Society) hence this is the strong sales focus following a company restructuring which reduced the size of the sales force and shut down numerous campaigns focused on other market opportunities. Probably a wise move, given the scale of the cutbacks the company must make to stay solvent.

Still, this is a poor return from a near $80m SG&A spend since IPO, and it seems entirely right that the management team responsible for this outcome have been moved on, or chosen to move on from, the company. John Gandolfo, Thomas Patton, and Peter Cuneo are the replacements, and are, according to the CEO,

proven organisational leaders with diverse medical device industry and turnaround experience that will serve us very well as we continue to execute on our more streamlined commercial plan.

To my mind, although the NHS and VA contracts are promising and growing sales, by 20% sequentially in the case of VA with paid months of therapy also increasing by 31% to 1,084, and by 5% sequentially outside the US to 1008 paid months of therapy, it should not have proven so difficult to market and sell a product that is unique, proven to work, portable, and inexpensive to produce.

In order to turn the company around, I believe the company would benefit from a complete overhaul of its pricing structure, and should explore a direct-to-consumer model to complement its reimbursement efforts, such as those used by the likes of DexCom, and Medtronic. Surely, selling at scale is preferable to charging a very small pool of customers a prohibitive amount.

I’ll admit to being slightly concerned not to hear management discussing these kinds of sweeping changes on the recent earnings call. Instead, the company discussed in detail a plan to submit an Emergency Use Authorization (“EUA”) application to the FDA pitching electroCore as a means to treat respiratory issues in COVID-19 patients.

Whilst this may be innovative and public spirited (and when announced, marginally lifted the share price above $1.3) sparking several clinical trials into life, it also seems tangential to the company’s core operations. In my mind’s eye, I can see a gammaCore device in the handbags or rucksacks of perhaps hundreds of thousands of people worldwide, if only the price and the strategy were right.

Clinical development has stalled

electroCore also announced during the Q120 earnings call that as part of its cost-cutting strategy it was abandoning its Premium II study to support its label expansion into migraine prevention. The trial was the largest randomized controlled clinical trial of gammaCore in migraine prevention in the United States. The abandonment means the company is no longer pursuing any clinical trials, which from a cost-cutting perspective may be a wise move. Management has advised that the data collected may still prove useful, however.

Although data from the Premium trial saw gammaCore outperform a sham device in almost every category the conclusion from the trial was that preventive effects of nVNS in episodic migraine were not superior to sham stimulation. The results may have been skewed somewhat, however, by the fact that the sham device “produced a level of active vagus nerve stimulation (28) that likely affected the therapeutic gain observed in the study.” It’s possible that, if electroCore had the funding, further tests might have seen the verdict reversed, since patient adherence rates were also low.

Another recently conducted study (it is worth noting that this study was funded by electroCore, although that does not necessarily invalidate the results) of cluster headache sufferers, concluded that

That gammaCore provides safe and effective pain relief to patients in the real-world setting and should therefore be considered for reimbursement by payers in the United States.

Whether this is enough to persuade physicians and health insurers to consider gammaCore a standard-of-care treatment remains to be seen – my verdict would be, “not at the current price”.

Can new management team arrest the slide?

There’s no doubt that management faces a daunting task trying to turn the fortunes of electroCore around, but at the very least, there appears to be a lot of low-hanging fruit that could be plucked immediately in order to make the overall situation look more palatable.

Investors may well be facing further dilution. Management discussed the possibility of a reverse stock-split, which may be necessary to avert a de-listing, during the recent earnings call. COVID-19 has also affected the company’s operations, as CFO Brian Posner warned analysts:

Due to these risks and uncertainties the company may need to reduce its activities significantly more than its current operating plan and cash flow projections assumed in order to fund its operations beyond the first quarter of 2021.

Given the scale of the task ahead, it is tempting to wonder if management has already raised the white flag and has resorted to running the company along restructuring lines until the funding runs out. Management did not discuss a specific turnaround plan or a strategic overhaul of the business during the earnings call, which is surely required since current revenue streams are not large enough to cover costs, even if they are drastically reduced as promised.

At this stage, however, I will give management the benefit of the doubt and assume they are looking at a range of options, including my suggestions above.

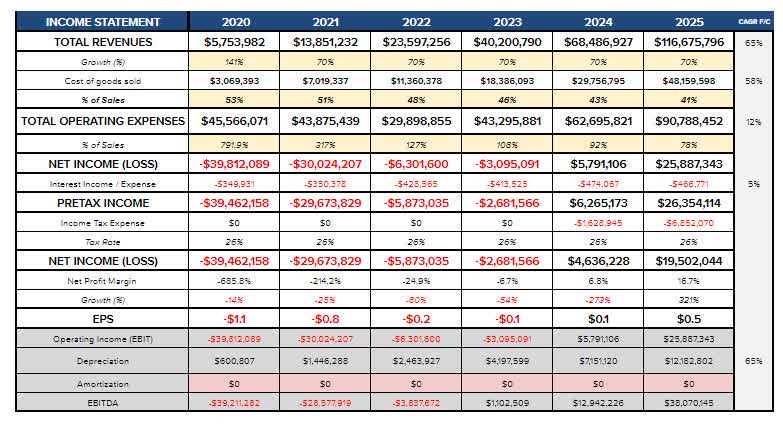

It is possible to (using ballpark figures) forecast a situation whereby electroCore becomes profitable by YE25. Essentially, it would involve management reducing OPEX as a percentage of revenues (1980% in 2019) by 60% in years 1, 2, 3 and 4, whilst at the same time increasing top-line revenues by 141% in 2020 (the same level as 2019) and by half that percentage each year until 2025.

electroCore financial forecasts. Source: my table using company historical financial data plus my assumptions.

There are many different numbers and scenarios that an analyst could plug into a table like the above in order to try to sketch out a recovery plan for electroCore. Mine depends on a significant sales uplift and I suspect my 2020 top-line revenue expectations may be way beyond what is possible. Long term, however, management will need to somehow find a way to engineer growth like this.

I believe that the company’s best chance of turning it around involves a new pricing and sales strategy since with the incremental gains currently being made, it is hard to see how electroCore deals with its OPEX issues over the medium-to-long term.

Conclusion

All is not lost – yet. The legacy issues at the company appear very severe and perhaps it may not be possible to overcome them. But my bullish thesis rests on several important points.

Firstly, the efficacy of the product has been established – gammaCore is FDA-approved, and is arguably as effective a treatment for migraine and CH as any many currently available treatments.

Secondly, medical devices is a strong growth industry and the company’s core value offering – a portable, easy-to-use device to treat migraines – strikes me as a potential winner.

Thirdly, the company is under new management, with a new Chairman, and is in the process of clearing out the dead wood.

Fourthly, there is a route to funding via Lincoln Capital, and I believe investors can be diluted when the rewards on offer (huge share price gains if the company makes meaningful progress) are tantalizing.

And lastly, the company’s share price is proven to be responsive to catalysts meaning investors could potentially realize strong gains if things go right – which introduces (institutional or otherwise) investor goodwill into the equation.

As mentioned in my intro, if an investor were to buy stock now, they are likely to be able to sell at the same price (or a maximum of 30-50% lower price) in 9 months’ time, but during that period, there is the possibility of a potentially triple or even quadruple digit percentage gain in the stock price, if for example, a catalyst allows the company to capital raise at a share price of $5 instead of $1, and follows up with a commercial partnership, or lucrative new sales contract.

I believe the Woody Allen saying “80% of success is showing up”, is appropriate here. The gammaCore product is built, approved and has garnered favorable consumer reviews. Management may have failed spectacularly when attempting to sell it, but the core value proposition is unchanged, and as contrarian as it may seem, I believe gammaCore retains the opportunity to become a successful product, and electroCore a profitable company.

Gain access to all of the market research and financial analytics used in the preparation of this article plus exclusive content and pharma, healthcare and biotech investment recommendations and research / analytics by subscribing to my channel, Haggerston BioHealth.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in ECOR over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}