Philip Morris International (NYSE:PM) is a buy for the dividend income investor that also wants to take advantage of the overdone stock price dip. Philip Morris International is one of the largest manufacturers and distributors of smoking products. PM is a conservative investment for the income investor who also wants a moderate growth estimate of 6% that is increasing since the FDA approval of IQOS.

Philip Morris International is 4.8% of The Good Business Portfolio (a full position). The company has slow growth and has the cash it uses to increase the dividends each year.

I use a set of guidelines that I codified over the last few years to review the companies in The Good Business Portfolio (my portfolio) and other companies that I am considering. For a complete set of guidelines, please see my article “The Good Business Portfolio: Update to Guidelines, August 2018“. These guidelines provide me with a balanced portfolio of income, defensive, total return, and growing companies that hopefully keeps me ahead of the Dow average.

When I scanned the five-year chart, Philip Morris has a poor chart going up and to the right in a steady, strong slope for three of the five years with a downturn starting in 2018 when the FDA started to investigate vaping and other smokeless products. Recently, the PM stock price has gone down with the market correction but not as much as the market. This correction creates a buying opportunity for a great slow-growing defensive business at a discount price.

Data by YCharts

Data by YCharts

Philip Morris is being reviewed in the following topics below.

- The Good Business Portfolio Fundamentals

- Company Business

- Conclusions

- Portfolio Management Highlights

Good Business Portfolio Fundamentals

The Good Business Portfolio Guidelines are just a screen to start with and not absolute rules. When I look at a company, the total return is a crucial parameter to see if it fits the objective of the Good Business Portfolio. My total return guideline is that total return must be greater than the Dow’s total return over my test period. Philip Morris misses against the Dow baseline in my 51-month test compared to the Dow average. I chose the 51-month test period (starting January 1, 2016, and ending to date) because it includes the great year of 2017 and 2019, and other years that had a fair and bad performance. The poor Philip Morris total return of -15.56% compared to the Dow base of -6.84% makes Philip Morris a poor investment for the total return investor but makes an interesting investment for increasing income. Looking back five years, $10,000 invested five years ago would now be worth over $9,800 today. This slight loss makes Philip Morris a poor investment for the total return investor looking back, which has future growth as the United States and worldwide countries need more of the company’s IQOS heated tobacco products.

Dow’s 51-month total return baseline is -6.84%

|

Philip Morris does meet my dividend guideline of having dividends increase for 8 of the last ten years and having a minimum of 1% yield. Philip Morris has an above-average dividend yield of 7.7% and has had increases for twelve years, making Philip Morris the right choice for the dividend growth investor. The dividend was last increased in September 2019 for an increase from $1.14/Qtr to $1.17/Qtr or a 3% increase. The five-year average payout ratio is high, at 94%. After paying the dividend, this leaves cash remaining for increasing the business of the company by developing new additions to the company’s products.

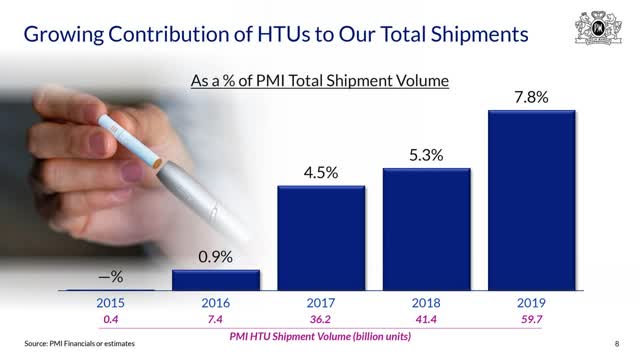

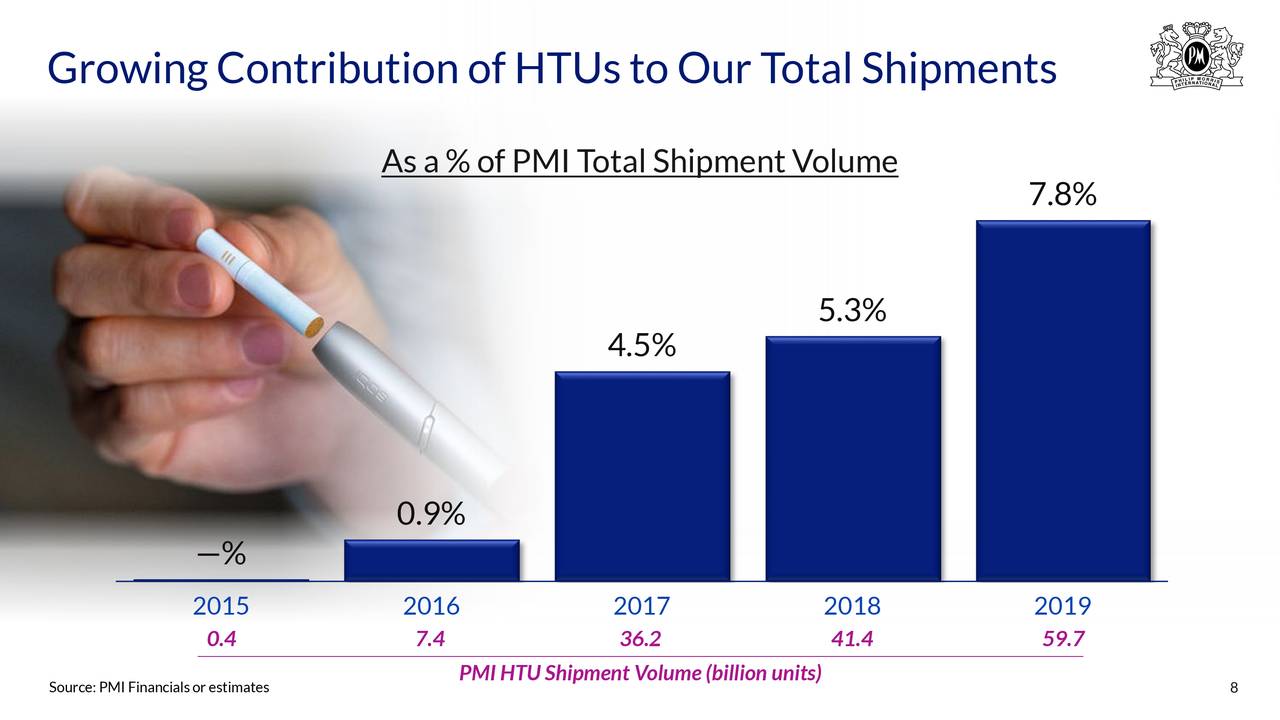

I also require the CAGR going forward to be able to cover my yearly expenses and my RMD with a CAGR of 7%. My dividends provide 3.3% of the portfolio as income, and I need 1.9% more for a yearly distribution of 5.2% plus an inflation cushion of 1.8%. The three-year forward S&P CFRA CAGR of 6% misses my guideline requirement. This slow future growth for Philip Morris can continue its uptrend benefiting from the reliable growth of heated tobacco products in the United States and worldwide but may be mitigated by the coronavirus short term. The graphic below shows the growth of the HTU product.

Source: PM earnings call slides

I have a capitalization guideline where the capitalization must be greater than $10 Billion. Philip Morris passes this guideline. Philip Morris is a large-cap company with a capitalization of $95 billion. Philip Morris 2020 projected cash flow at $10.3 billion is good, allowing the company to have the means for company growth each year. Companies like Philip Morris have the cash and ability to buy other smaller companies and weather any storms that might come along.

One of my guidelines is that the S&P rating must be three stars or better. Philip Morris’s S&P CFRA rating is four stars or buy with a target price of $100, passing the guideline. Philip Morris’s price is below this target by 56%. Philip Morris is below the target price at present and has a low forward PE of 11, making it a great buy at this entry point. Considering the potential growth and stability of the company, if you are a long-term investor that wants good, increasing income and moderate growth, you may want to look at this company. Take advantage of the correction and buy a good business at a nice discount.

One of my guidelines is would I buy the whole Company if I could. The answer is yes. The total return is not good looking back, but the above-average dividend yearly yield has grown at a fair rate over the past five years, making Philip Morris a great business to own for the growth and the long-term income investor. The Good Business Portfolio likes to embrace all kinds of investment styles but concentrates on buying companies that can be understood, makes a fair profit, invests profits back into the business, and also generates a good income stream. Most of all, what makes Philip Morris interesting is the increasing long-term demand for the company’s smokeless products, and the product pricing is inelastic.

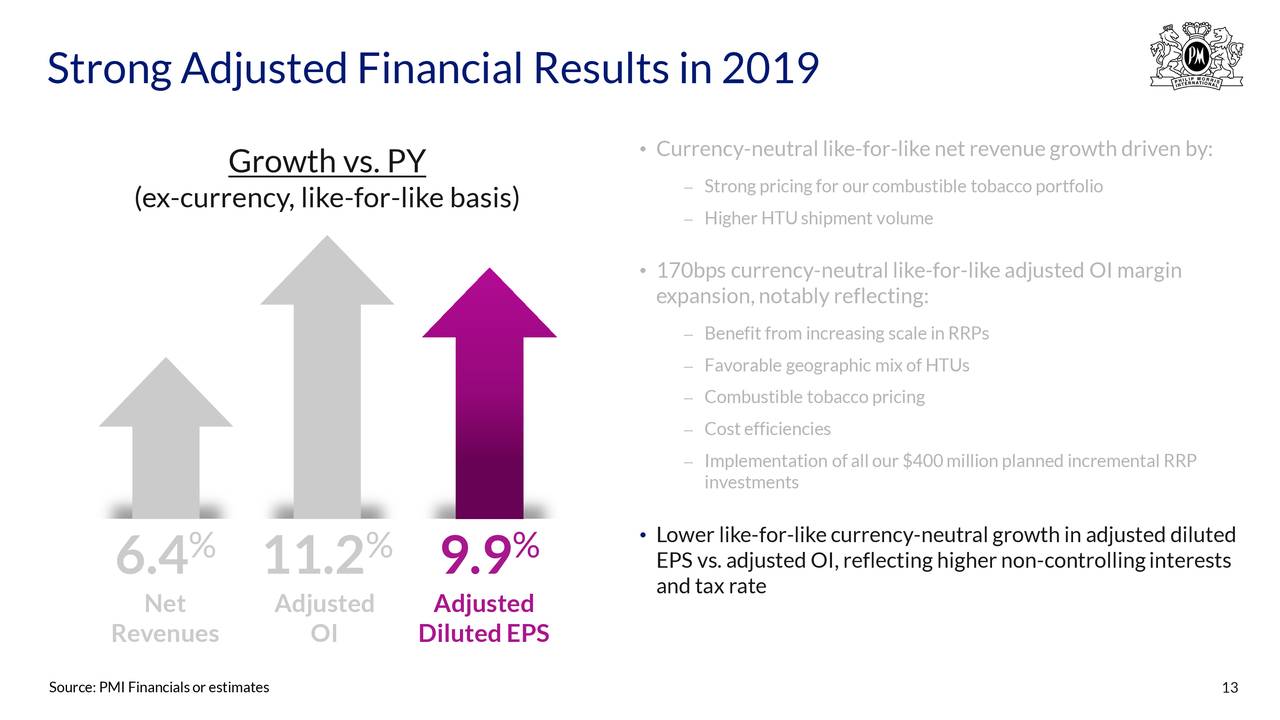

I don’t have a guideline for earnings, but look for the earnings of my positions too consistently beat their quarterly estimates. For the last quarter on February 6, 2020, Philip Morris reported earnings that beat expected by $0.01 at $1.22, compared to last year at $1.25. Total revenue was higher at $7.71 billion more than a year ago by 2.8% year over year and beat expected total revenue by $70 million. This was a mixed report with bottom-line beating expected and the top line increasing with an increase compared to last year. The next earnings report will be out April 2020 and is expected to be $1.08 compared to last year at $0.87 a strong increase. The graphic below shows 2019 yearly growth.

Source: PM earnings call slides

Company Business

Philip Morris International is one of the largest manufacturers and distributors of tobacco products in foreign countries.

As per data from Reuters

The company is engaged in the manufacture and sale of cigarettes, other tobacco products, and other nicotine-containing products in markets outside of the United States.

Its segments include European Union (EU); Eastern Europe, Middle East & Africa (EEMA); Asia, and Latin America & Canada. The company’s portfolio of international and local brands is led by Marlboro.

Its mid-price brands are L&M, Lark, Merit, Muratti, and Philip Morris. Its other international brands include Bond Street, Chesterfield, Next, and Red & White.

Overall, Philip Morris is a good defensive business with a 6% S&P CFRA CAGR projected growth as the worldwide economy grows going forward with the increasing demand for more smokeless products. I feel this growth rate will be at least 8% because of the IQOS and HEETs products. The good earnings and revenue growth provide PM the capability to continue its growth as the business increases by the demand for the inelastic smokeless sector.

From the 4th quarter earnings call are a few highlights that show the great growth and opportunities that are the future of Philip Morris.

IQOS is performing strongly across a broad array of geographies and remains firmly on track to meet the 2021 heated tobacco unit shipment volume target of 90 billion to 100 billion units.

The combustible business continues to perform well underpinned by solid pricing. They achieved several important milestones in their transformation to a smoke-free future. This included the authorization for a version of our IQOS product from the U.S. Food & Drug Administration through the pre-market tobacco product application pathway and the subsequent commercial launch in Atlanta and Richmond under our licensing agreement with Altria. IQOS is now commercially available in 52 markets worldwide.

The shipment volume declined by 1.4%, in line with our previously communicated forecast decline of 1% to 1.5%. The outperformance of the industry was driven by heated tobacco share gains of 0.6 points, which helped offset cigarette declines, partly impacted by heated tobacco unit cannibalization.

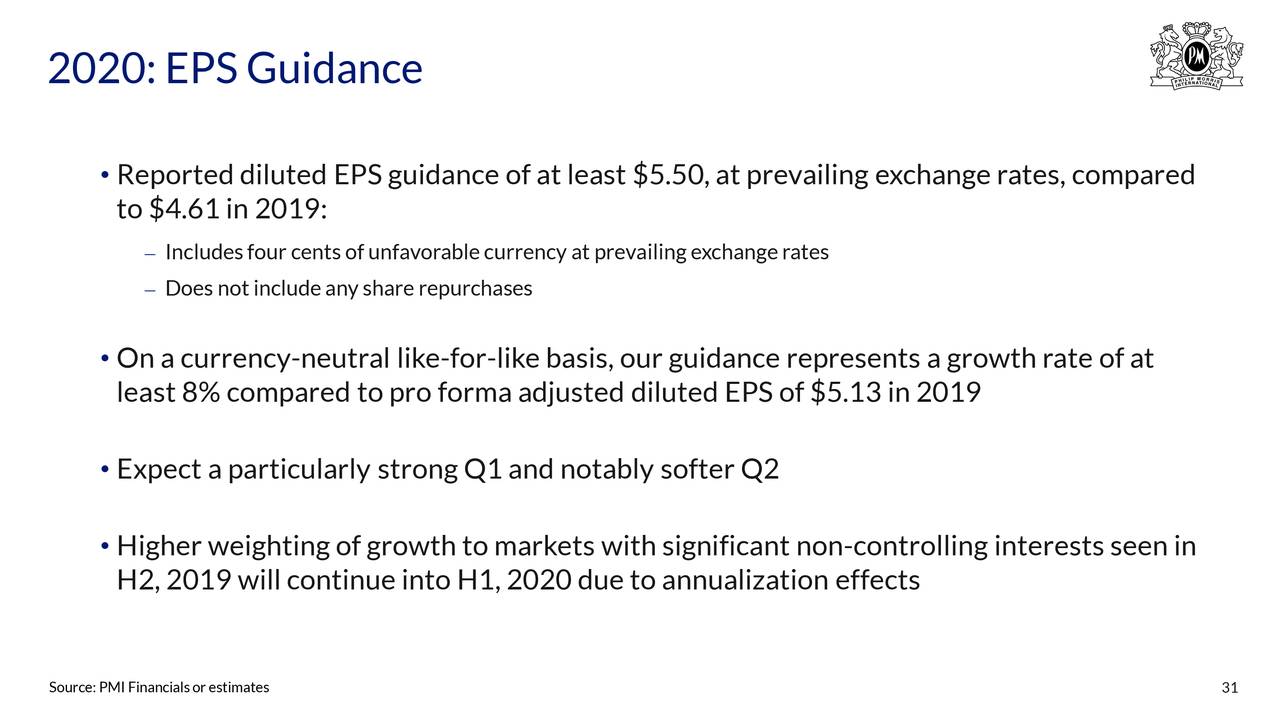

This shows the growth in the 4th quarter that can continue going forward with an increase in top and bottom lines. Philip Morris has good growth and will continue as the United States population grows with the need for more smokeless products. The growth is being driven by the smokeless product sector, which may be balanced by a slowing economy because of the coronavirus. The graphic below shows the EPS guidance for 2020.

Source: PM earnings call slides

Conclusions

Philip Morris International is a good investment choice for the dividend income investor with its above-average high dividend yield and a poor choice for the total return investor looking back. Philip Morris International is 4.74% of The Good Business Portfolio and will be held and watch it grow. PM will be held in the portfolio and will be trimmed when it reaches 8% of the portfolio. If you want a growing dividend income and fair total return to come in, the smoking product business PM may be the right investment for you. I think the price drop, due to the FDA’s possible regulations and the downturn in stock price correction creates a buying opportunity to buy a quality business at a bargain price.

Portfolio Management Highlights

The five companies comprising the largest percentage of the portfolio are Johnson & Johnson (JNJ) at 9.3% of the portfolio, the Eaton Vance Enhanced Equity Income Fund II (EOS) at 7.8% of the portfolio, Home Depot (HD) at 10.3% of the portfolio, Omega Healthcare Investors (OHI) at 9.0% of the portfolio, and Boeing (BA) at 8.0% of the portfolio. Therefore, BA, EOS, JNJ, OHI, and HD are now in trim or close to trim position, but I am letting them run a bit since they are great companies.

- On February 4, I trimmed HD to 9% of the portfolio. HD is a great business but needs more foreign expansion to grow even stronger.

- On January 13, I trimmed DHR to 1.5% of the portfolio. I like DHR long term, but the next year’s earnings look a bit weak, and I need cash for my RMD.

- On December 5, I wrote covered calls against my Danaher (NYSE:DHR) position to collect another premium ($1.54/share December $150). I like DHR, but it’s getting a bit pricey, and the covered calls give me some extra income and some downside protection. On December 19, I closed the position by buying back the calls and made a small profit.

Boeing is going to be pressed to 10% of the portfolio because of it being cash positive on 787 deferred plane costs at $1.3 billion in the third quarter of 2019, an increase from the second quarter. Boeing has dropped in the last ten months because of the second 737 Max crash, and I look at this as an opportunity to buy BA at a reasonable price. From the latest news on Boeing is a rumor that Warren Buffett is taking a position on BA, maybe he knows a good investment. It now looks like the 737 MAX will not be approved until mid-year, but the FAA has said it could be earlier because Boeing is making good progress, all will depend on the first test flight with the FAA.

JNJ will be pressed to 9% of the portfolio because of its defensive nature in this post-BREXIT world. Earnings in the last quarter beat on the top and bottom line, and Mr. Market did nothing. JNJ in April 2019 increased the dividend to $0.95/Qtr., which is 57 years in a row of increases. JNJ is not a trading stock but a hold forever; it is now a strong buy as the healthcare sector remains under pressure.

The total return for the Good Business Portfolio is ahead of the Dow average from 1/1/2020 to March 20 by 0.97%, which is a small gain above the market loss of 32.81% for the portfolio with BA a strong drag. Each quarter after the earnings season, I write an article giving a complete portfolio list and performance, the latest article is titled “The Good Business Portfolio: 2019 4th Quarter Earnings and Performance Review“. Become a real-time follower, and you will get each quarter’s performance after the next earnings season is over.

Disclosure: I am/we are long BA, JNJ, HD, EOS, DHR, MO, DIS, V, OHI, TXN, PM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Of course, this is not a recommendation to buy or sell, and you should always do your own research and talk to your financial advisor before any purchase or sale. This is how I manage my IRA retirement account, and the opinions of the companies are my own.

{kind=link}