State Agencies Release Dairy Marketing Assessment Report to Legislature

Vermont Business Magazine Dairy consumption in the United States is actually going up, Vermont cheese has made in-roads against Wisconsin cheese and there could be several opportunities for local dairies to take advantage of changing consumer tastes. The Vermont Agency of Agriculture, Food & Markets (VAAFM) and the Vermont Agency of Commerce and Community Development (VACCD) outlined to legislators today a report looking at the future of dairy in Vermont and the economic viability of expanding dairy markets in the northeast, major metropolitan areas and beyond.

The report comes as a result of Act 83 requiring both Agencies to research these concerns and report back. (To read the report, analyze its findings and recommendations, click HERE.)

While the Dairy Marketing Assessment Report brings research to the table, it also points to a number of opportunities that could best leverage the state’s recent selection and funding as one of the nation’s Dairy Business Innovation Centers. VAAFM will receive $6.45 million over three years allowing Vermont and the region to focus on innovative ideas and projects that will give the dairy sector options. One of the most exciting opportunities of this funding is that half of the money will be distributed as grants to dairy farmers and value-added processors.

“We are focused on improving the bottom line for all dairy farmers,” said VAAFM Secretary Anson Tebbetts. “This comprehensive report gives us a path to improve the dairy economy. Farming is important and farmers are important to the future of Vermont.”

Both the Dairy Marketing Assessment Report and the Dairy Business Innovation Center funding recognize the value of dairy and agriculture to the state and its economy. In 2017, Vermont dairy receipts totaled $504,884,000 million dollars, accounting for 65% of Vermont’s total agriculture receipts (USDA National Ag Statistics). In total, agriculture was responsible for $776,105,000 million in receipts, highlighting the importance of the industry to Vermont’s economic diversity.

Heather Pelham, Commissioner of the Vermont Department of Tourism and Marketing said, “High-quality local food and culinary experiences are at the heart of the Vermont experience for over 13 million visitors to the state each year. This report reminds us of the important role that high-quality dairy products, such as cheese and ice cream, play in maintaining that Vermont food experience and supporting Vermont’s brand associations with quality and authenticity.”

VAAFM Deputy Secretary Alyson Eastman believes these numbers point to a state economy that thrives from its rural communities. “The Dairy Marketing Assessment, coupled with the Vermont Dairy Innovation Center funding and innovative thinking, will give our Vermont dairy farmers the opportunity to improve market opportunities, create pathways for new products, help diversify their farms and address ongoing environmental challenges,” Eastman said.

VACCD Department of Economic Development Commissioner Joan Goldstein said, “This report is an important piece to help the Vermont dairy industry – an industry, like so many in Vermont that has combined its historic roots with innovation to produce some of the best food in the world.”

NATIONAL & REGIONAL DAIRY MARKET DYNAMICS

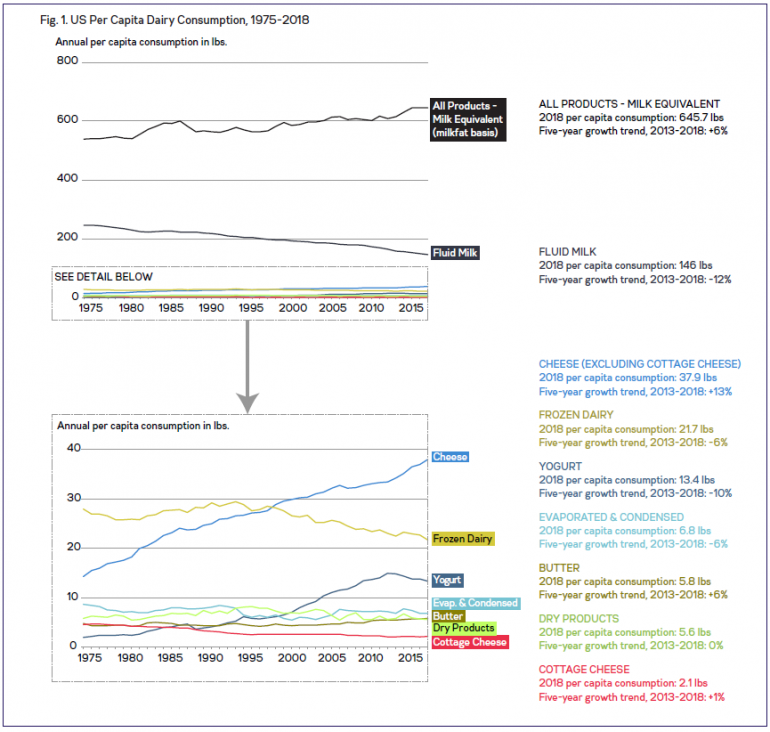

Dairy consumption in the U.S. has changed substantially over the past two decades and continues to shift. Figure 1 illustrates changes in U.S. per capita consumption of dairy products from 1975 to 2018. While fluid milk consumption has been steadily declining for years, Americans are actually consuming more dairy than ever—6% more (by milk equivalent) in 2018 than five years prior.

This growth is largely driven by cheese and butter consumption, which grew 13% and 6%, respectively, from 2013 to 2018, while fluid milk consumption dropped by 12%.

Since cheese and butter require many pounds of milk to produce a single pound of finished product, Americans now consume more milk in the form of cheese and butter than they do as fluid.

Cheese consumption alone accounts for more than twice the volume of fluid milk Americans consume (350 lbs. milk equivalent per capita as cheese vs. 146 lbs. fluid milk). Fluid milk’s steady decline belies more nuanced dynamics within the fluid milk market.

One of the more notable shifts over the past decade has been the reversal in whole vs. reduced fat and non-fat milk. After reaching a low point in 2013, whole milk sales have been climbing since, growing 15% from 2013 to 2018. Reduced fat milks (1% and 2% milk fat), in contrast, declined by 15% during that time, while non-fat milk sales dropped by 44%.

Farmers and processors we spoke with commented on the challenges of adapting to this shift in consumer preferences, as it has led to an oversupply of skim milk, and an undersupply of cream as an ingredient for products like half-and-half.

Data provided by New England Dairy reveals additional trends in fluid milk consumption at both the national and New England levels.

Organic milk sales, which occupy 13% of the U.S. market and 17% of the New England market by sales value, both dropped from 2017 to 2018, and continued to slip in the first three quarters of 2019. Grass-fed milk, which accounts for 0.4% of the New England market and 0.25% of the U.S. market by sales value, saw tremendous growth from 2015 to 2018; the segment grew by 13% for the U.S. during the first three quarters of 2019 but dropped by 13% for New England.

Sales of non-homogenized milk in both markets have slipped after peaking in 2015 and 2016, and still occupy a market share of less than one-tenth of one percent. Lactose free milk, at 11% U.S. and 12% New England market share by sales, is growing in both markets.

After peaking in 2013, per capita yogurt consumption has been on the decline since, dropping by 10% from 2013 to 2018. New England Dairy data also shows that yogurt consumption is dropping in both the U.S. and New England markets.

Greek yogurt, which two interviewees acknowledged for giving a big boost to the dairy sector, has been declining since a 2015 peak in both New England and the U.S., though it still occupies substantial market share (48% of all yogurt sales in New England, 43% in the U.S.).

Quantitative data and qualitative input from interviewees both support the notion that cheese is an area of high potential and growth for the dairy sector.

As previously mentioned, U.S. per capita cheese consumption grew by 13% from 2013 to 2018, and accounts for more than twice as much milk usage as fluid milk.

A 2020 market research report by Sundale Research projects that U.S. cheese consumption will grow by 14% in sales from 2019 to 2024. The report also explicitly calls out specialty and artisan cheeses as top growth segments, noting that specialty cheese sales grew 9.5% in 2018 and 8.7% in 2019, amounting to about $5 billion in retail sales; it projects specialty cheese growth of 8% per year from 2019 to 2024, significantly outpacing growth in the overall cheese market.

According to Sundale’s research, specialty cheese accounts for 12% of total U.S. cheese production, at 1.6 billion pounds in 2019.

State origin data from New England Dairy shows that Vermont-origin cheese accounts for $63.4M in sales in New England and $220M in the U.S., representing 8.1% and 1.3% market share respectively.

Vermont-produced cheese has been steadily climbing in New England market share over the past five years; in 2018, Vermont cheese surpassed Wisconsin cheese in New England market share for the first time, and increased its lead over Wisconsin in 2019.

In U.S. sales, Wisconsin has lost market share for the last four years, whereas Vermont has shown recent gains.

· To read the report, click here: 2020 Vermont Dairy Marketing Assessment Report.

· To find more on the Vermont Dairy Innovation Center, click here: Vermont Dairy Innovation Center.

Source: February 26, 2020 I Montpelier, VT – The Vermont Agency of Agriculture, Food & Markets

{kind=link}