Alibaba (BABA) has the following company mission: “To make it easy to do business anywhere”. The company provides the technology infrastructure and marketing reach to help merchants, brands, and other businesses leverage the power of new technology for efficient transactions between parties.

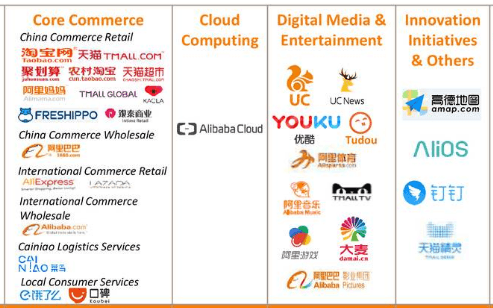

The company’s core commerce business comprises 86% of total company revenue and is the largest retail commerce business in the world. This was accomplished through various businesses: Alibaba.com, Taobao.com (China’s largest mobile commerce), Tmall.com (mobile commerce platform for brands/retailers), AliExpress, Lazada (e-commerce in Southeast Asia w/ various language apps), and others.

Alibaba also has a growing cloud business comprising 7% of company revenue. Alibaba is China’s dominant cloud provider and the company is at the top of the cloud market in Asia. There is plenty of room for further growth as projections are calling for 17% global cloud revenue growth in 2020. Alibaba currently ranks as the fourth largest cloud provider worldwide behind Amazon (AMZN), Microsoft (MSFT), and Google Cloud (GOOG). Alibaba is expected to surpass Google Cloud to become the world’s third largest cloud provider in 2020.

Alibaba also has a digital media/entertainment business comprising 6% of total revenue primarily through Youku (China’s online streaming service) and UCWeb (mobile web browser, gaming, reading). The company’s innovation initiatives (smart speakers, digital maps/navigation, business efficiency app) comprise the remaining 1% of revenue.

Strengths

One of Alibaba’s largest strengths is their wide business diversity. The company runs multiple websites and businesses, which spreads revenue over a large number and variety of customer sources. This includes consumer to consumer, business to consumer, and business to business services.

- Alibaba’s e-commerce business is diversified among multiple websites and wide product selections. This reduces risk as the company is not highly dependent on a small number of customers. The company acts as a portal or common denominator for the global economy, benefiting from the top selling items in the marketplace.

- The company established themselves as the largest retail business globally. This achievement can help the company continue to grow as their reputation and reach spreads to a growing number of new customers.

- With a gross margin of 46%, Alibaba has a higher gross margin than Amazon’s 41% and Tencent’s (OTCPK:TCEHY) 44%. The company’s EBITDA margin of 28% is significantly higher than Amazon’s 12.9%.

- The return on equity [ROE] of 29.8% is higher than Amazon’s 23.7%. This shows that Alibaba gets a higher return on shareholders’ equity, a measure of management effectiveness.

- Alibaba has a strong research & development [R&D] program. Over the past 12 months, Alibaba spent 8.8% of total revenue on R&D. This helps the company remain on the cutting edge of technology and their businesses in order to achieve ongoing growth.

Weaknesses

Alibaba has some weaknesses that are the nature of their business and others that can be improved upon.

- The business requires large capital investments for expansion. In order to grow, large investments need to be made for the logistics network, facilities, new technologies, expanding the core commerce offerings, and for acquisitions.

- The company’s e-commerce business is flooded with a large amount of sellers. While this can be good for consumers, it can reduce margins for sellers and make doing business for them challenging with such high competition.

- The ROIC of 7% is lower than Amazon’s 8.23%. Double-digit ROICs are preferable. So, we’ll have to see if Alibaba can improve their returns as they grow their cloud business.

- Alibaba is a China-based company. This makes the company largely dependent on the health of China’s economy and any potential unfavorable trade policies between China & the U.S. and other nations.

Opportunities

Alibaba has various options and strategies to grow the business for the long-term.

- Continued expansion globally: Alibaba established themselves well in China and Asia. There is plenty of room for further growth on an international basis. The company can leverage their success and expertise and apply it in untapped regions.

- Expand the cloud business: Alibaba has a successful growing cloud business. The double-digit growth for the cloud market provides room for Alibaba to expand this business segment further.

- Growth can also be aided through partnerships with other companies. This is where Alibaba can get creative. Partnering with established experts in various regions can help secure new business rather than doing it alone.

- Strategic acquisitions can help Alibaba expand on top of their organic growth. This could be smaller cloud businesses, additional e-commerce websites/businesses, and media/entertainment firms.

Threats

While Alibaba is currently thriving, there are a number of external factors that could have negative consequences for the company.

- Increased competition is an ongoing threat. Alibaba competes with Amazon, Microsoft, and Google in the cloud space. Of course, the company competes with Amazon and Walmart (WMT) in the e-commerce market. Tencent is a large competitor in China for the digital media/entertainment segment. Increased competition could make it challenging for Alibaba to grow market share in their various businesses.

- A slowdown in China’s economy would likely have a negative effect on Alibaba’s revenue. Slowdowns in the global economy could also reduce the company’s revenue.

- Unfavorable tariffs or trade policies could make doing business with other countries more expensive. New government regulations in each region where the company operates could add to the company’s costs.

- High profile security breaches, attacks on networks/systems, or counterfeit sellers could harm the company’s reputation and lead to the loss of business.

Long-Term Business Outlook for Alibaba

Alibaba is experiencing growth in each business segment. This has a good probability of continuing as the markets for these segments are all expected to grow at double-digit CAGRs. The markets for e-commerce, the cloud, and video streaming are expected to grow at a CAGRs of 11%, 10% and 19.6% through 2025 respectively. Alibaba’s is poised to grow each business segment with the tailwinds in these markets along with their effective offerings.

Alibaba has a good chance of achieving above average growth over at least the next 5 years. There might be a hiccup along the way if a recession hits in China or globally. However, overall future growth has a good chance of being positive for most years. Alibaba has a good track record of achieving growth and this can be leveraged and capitalized on going forward.

Fears regarding the coronavirus already caused the stock to begin declining. While I am bullish on the company for the long-term, I would wait for the aftermath of the coronavirus to play out. The stock could fall much further until more clarity of this situation becomes apparent.

The 2020s will see the transformation of the economy during the 4th Industrial Revolution. We are also running head first into a wave of demographic and debt driven problems that will need solving. A cautious, but forward looking approach, will be required to thrive in what could be a lost investing decade for many, much like 2000-2009.

Benefit from the insights of Kirk Spano, Dividend Sleuth and David Zanoni. Get exclusive investment ideas based upon in-depth and up close research that few others do.

Sign-up now for a free trial and 20% first year discount.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. Business relationship disclosure: The article was written by David Zanoni for Kirk Spano’s Margin of Safety Investing service [MoSI]. Subscribers had an early look at this article. We have a library of SWOT analyses that are primarily available to subscribers. However, we release a few to the public as samples.

Additional disclosure: The article is for informational purposes only (not a solicitation to buy or sell stocks). David is not a registered investment adviser. Kirk Spano is an RIA. Investors should do their own research or consult a financial adviser to determine what investments are appropriate for their individual situation. This article expresses my opinions and I cannot guarantee that the information/results will be accurate. Investing in stocks involves risk and could result in losses.

{kind=link}