Image Credit: Capital Product Partners Homepage

Capital Product Partners Overview

Capital Product Partners LP (CPLP) is an income-focused shipping company with primary exposure to 10 containerships on long-term contracts along with a sole Capesize bulker fixed until Q3-2020. The dry bulk vessel is non-core and I expect that it will be sold off during 2020.

CPLP is ahead of the curve for IMO 2020 compliance and they unveiled a plan last year, with shipyard options secured, to install scrubbers on their entire core fleet. This summer, CPLP further improved their coverage by fixing their two 8k TEU vessels through February 2024 in conjunction with scrubber installations. They disclosed expected EBITDA instead of TCE, but I estimate the equivalent rate of about $24k/day, which is a significant increase from previous short-term employment at $18k/day.

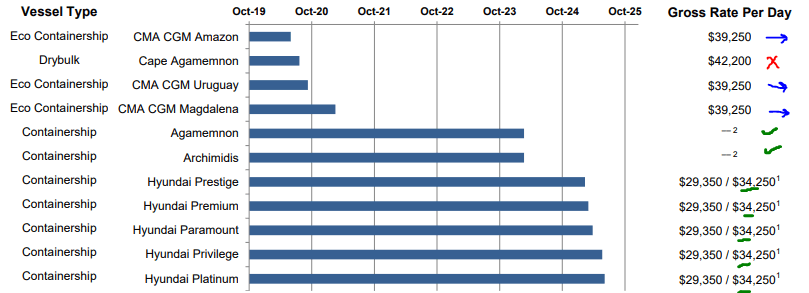

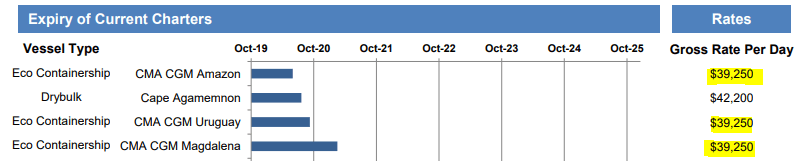

CPLP offers heavy coverage through 2024 and their recent three dropdowns, which we will discuss in greater detail further below, further solidify the company as a top-tier income selection. The impressive charter coverage is shown below:

Source: Capital Product Partners, Q3-19 Presentation, Slide 6 (marks added)

The bulker is well above-market, but it will likely be sold off. The trio of Eco Containerships is highly likely to be extended at similar rate levels. The rest of the fleet is fixed to 2024-2025 and the five Hyundai-linked vessels will all receive significant rate boosts in January 2020. The slide actually understates the increase because those 5 ships are currently earning just $23,480/day. We’re looking at a massive $54k/day swing in DCF into 2020!

CPLP is now an exceptional income vehicle with clear coverage over the next five years. CPLP currently has 18.5M units outstanding for a current market cap of about $245M. Their current yield is 9.5%, but I expect we’ll see some increases soon. CPLP historically trades around a 9% yield, so any increases will likely also boost the unit pricing.

Review of Historical Returns & Performance

2019 was a significant transition year, which included the spin-off of their full product tanker fleet to Diamond S Shipping (DSSI). Patient investors in both CPLP and the follow-on DSSI vehicle have been richly rewarded, but this pick has not been without controversy due to investor angst over the lack of distribution increases. There was also a lot of misconception floating around in late-2018 into early-2019 that the payout was ‘cut,’ but this ignored the significant value of the tanker spinoff. Nonetheless, bulls have been proven correct on CPLP, with eye-watering 2019 total returns (including DSSI spinoff) of 77%. Some weird preliminary brokerage accounting of gain/loss have confused some folks, but the way to properly calculate vs. historics:

- CPLP price ($13.28) divided by 7 (due to reverse split) = $1.90

- DSSI price ($16.43) divided by 10.19 (spinoff ratio) = $1.61

- CPLP’s 2019 distributions ($1.26) divided by 7 (reverse) = $0.18

- $1.90 + $1.61 + $0.18 = $3.69 (77% above 31 Dec 18 price of $2.09)

CPLP has been a huge winner from almost any entry-point as long as investors were patient. For those who added into the dips, as we advocated in September 2018, November 2018, December 2018, and February 2019, the returns have been enormous.

I’ve covered CPLP for a long time and the initial stock pricing was rocky, but we’ve been proven correct as the market slowly begins to realize its value. As reviewed above, the current results are equivalent to ‘CPLP-old’ at $3.69. If we’re back-testing further, CPLP paid out $0.32 in 2018 ($4.01 equivalent), $0.32 in 2017 ($4.33 equivalent), and $0.15 in 2H-16 ($4.48 equivalent).

Although we’re firmly in positive territory (massively positive depending on timing), there is still significant total return upside remaining as DSSI is still the cheapest valued tanker company and CPLP still trades significant below my estimate of adjusted NAV, which is in the low-$20s.

For the rest of the report, I will review the recent dropdown and refinancing transaction, and outline the case for CPLP as a top income choice into 2020.

Deal Background: As Expected With No Equity Dilution

On 18 December, CPLP announced a trio of dropdowns and a partial refinancing of their 2017 credit facility. These dropdowns add significant coverage through April 2024 and they were all completed with zero additional equity (i.e. no dilution to unitholders).

We’ve been expecting CPLP to complete a dropdown (or two) for awhile, and I personally figured the most likely candidates would be the trio of 10K TEU ships. The slide below lists previous potential dropdowns (highlights added):

Source: Capital Product Partners, September Update Presentation, Slide 8

I have been an active participant on recent earnings conference calls and I dialed in on likely dropdowns and structure during the Q3-19 call on 31 October. I specifically confirmed if the 10K TEU vessels were the primary targets and asked if the balance sheet leverage could support additional drops without equity. After our conversation, in our earnings review on Value Investor’s Edge, I concluded:

…between the current cash balances, prospects of using much higher leverage on dropdowns (due to the super low leverage on the legacy fleet), and the good odds of a nice 9k TEU charter roll, I expect they could take at least 2, potentially all 3 of the containership drops without adding any new equity.

I was personally leaning more towards two ships, but as we now know, CPLP has accepted three vessels with zero new equity required! This is a significant win for income investors.

The Dropdown Deal Specifics

CPLP has agreed to purchase three 2011-built 10K TEU ships from their General Partner, Capital Maritime & Trading (“C-Mar”), for $162.6M ($54.2M apiece). They are financing the deal with a $38.5M term loan and two $38.5M sale leasebacks, for total deal leverage of 71%. The vessels themselves are employed at $27,000/day, which will increase to $28k/day on October 2020 for one vessel and from July 2021 for the other two vessels. The $28k/day charters will continue through April 2024 and they include two additional one-year options at $32.5k/day and $33.5k/day.

CPLP paid $47.1M in cash, but they also secured a refinancing on their trio of 9k TEU vessels, replacing a $134.9M facility with a $155.4M sale leaseback, which frees up $20.5M in cash and also reduces total annual amortization by $4.3M per year. CPLP calculates their DCF in a non-traditional manner (they report direct free cash flow as opposed to utilizing a complex replacement formula), so this refinancing move alone will automatically increase their reported DCF by nearly 6 cents per quarter. That’s prior to any of the dropdown contribution!

The term loan costs L+255 (4.48% on current 3m LIBOR) and the lease costs are undisclosed, but I am modeling about 5.0% fixed interest equivalent for both the CMBFL and ICBCFL facilities. CPLP confirmed the lease is at a lower cost than the current financing, which we know was done at L+325 (5.18% current), which supports my 5.0% guesstimate. From PR:

“Furthermore, the partial refinancing of our 2017 credit facility is expected to lower the overall debt amortization schedule of the Partnership by $4.3 million per year, as well as the weighted average interest margin, while also generating additional liquidity for the Partnership that can potentially fuel further growth.”

The only ‘catch’ of the leases is that they come with purchase obligations of $77.7M for the 9K TEU trio after 7 years (yes- Vegas style numbers) and $22.5M apiece after 5 years for the 10K TEU duo. VesselsValue lists the trio as worth $211M, suggesting the leverage is about 73%, but the amortization curve is immediate and smooth.

Source: VesselsValue, CPLP Fleet Overview, 18 December

These are modern eco-tonnage and should serve a minimum of 25-years (designed to do 30+ years). With a straight-line to $15M demolition, the estimated residual value of these ships in 7 years is approximately $152M en bloc, making the repurchase obligation extremely safe. Even with a super conservative 20-year life estimate curve, the trio would be worth about $133M at the end of their 7-year life, significantly above the $77.7M purchase obligation.

Fair Price Paid?

CPLP paid $54.2M apiece for their ships. This compares to $52.5M paid for similar sisterships (2010-built vs. 2011-built) by unrelated 3rd-party Navios Containers (NMCI) about a year ago. On one hand, NMCI was able to generate an additional year of revenue. On the other hand, those ships are one year older, the extension to April 2024 wasn’t yet completed, and sentiment was much weaker a year ago before US-China tensions cooled. VesselsValue currently carries this trio at roughly $49M apiece. Did CPLP overpay by $5M per ship? It’s doubtful, but definitely worth reviewing.

Source: VesselsValue, 16 December 2019

To justify the $49M valuation utilizing a demolition value of $15M and a current age of less than 9-years, requires an implied TCE of $27k/day (nearly $7M in annual EBITDA), a 20-year life expectancy (quite conservative), and a 10% discount rate to the model. To justify $54.2M, we need to see either:

- 25-year Lifespan with same assumptions

- TCE of $29k/day to 20-year lifetime

- Discount rate of 8.5% on the original model

All three of those assumptions (individually) seem very reasonable, especially since the deal is 71% debt financed at a fixed cost underneath 5%! I believe the pricing is entirely fair with those approaches. If we take all three of those assumptions ($29k/day, 25-year life, 8.5% discount rate), we get to $68M value per ship, which I believe is a reasonable ‘bull market value.’

Are the Charter Rates Good?

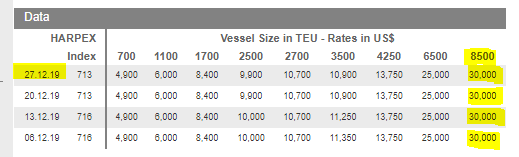

In regards to the charters, initial commentary has mentioned “below market” or even “well below market,” but it’s important to realize that these are not comparable to the 9K eco ships shown above. These 10K vessels also do not have scrubbers installed (nor do the 9K ships…yet). The Harpex index quotes the 8.5K TEU rates steady at $30k/day, but that is only for 1-year charters:

Source: Harper Peterson & Co, Harpex Index, 27 December 2019

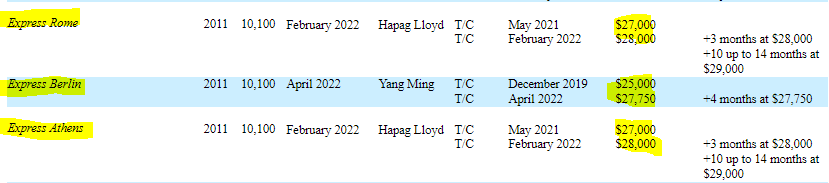

There aren’t any clear comps for these vessels, except from Danaos Corp (DAC), which has their vessels fixed (for less duration) at almost identical levels of $27-$28k/day.

Source: Danaos Corporation, 22 November Prospectus, Page S-2

Capital Maritime recently added the extensions (in mid-2019) through April 2024 at $28k/day. They wouldn’t do those agreements below market nor would their undisclosed counterparty (highly likely to be Hapag Lloyd per their fleet list) agree to anything other than what was indeed ‘market’ at the time.

I am very pleased with these charters, considering these are non-eco, non-scrubber vessels. Any market commentary suggesting these are below-market is simply uninformed.

Further Scrubber Install Upside?

I’m almost shocked that Hapag Lloyd hasn’t pushed for scrubbers yet. If Hapag Lloyd (or another counterparty) wants to install these, CPLP holds all the cards here. Only CPLP can do a scrubber deal since they technically own the ship, so they could extract very beneficial terms including mandatory blending and extending of charters. It wouldn’t be shocking to see something like bumping the rates on all three vessels to somewhere between $32-$35k/day and extending to mid-2026 or later if CPLP pays for the installation expenses.

Next Question: Dividends?!

What matters most for investors is dividends, that’s what drives this stock, which has historically always traded for around a 9% yield until we hit absurd pessimism for a brief period from late-2018 through early-2019. The recent dropdown significantly increase CPLP’s backlog and the refinancing on excellent terms proves the banks agree with cash flow stability. At a 9% yield without any raise, we already get CPLP to $14.00.

My assumption is that we will see a minor distribution raise by mid-2020, likely announced in April (ideally guided in late-January, but we’ll see) to $0.35/qtr. That’s a nice round number and gives CPLP lots of flexibility to see what they want to do with the trio of 9K TEU vessels coming up, potential additional scrubbers (the trio of 10K TEU vessels are perfect candidates for a deal), and to determine the fate of the lone Capesize bulker expiring in Fall 2020.

CPLP can pay for the entire raise to $0.35/qtr with just $2.6M per year, only a fraction of the savings from the lower amortization alone. It costs them virtually nothing, but it shows the firm is back to growing with an 11% raise. I’d like to see even higher raises, but I expect them to retain near-term optionality. Even a meager raise gets us to $15.55/unit with a 9% yield. A more aggressive raise to $0.40/qtr, which would also be super easy to afford, gets us trading around $17.78/unit assuming a 9% yield.

Actual Valuation Potential: $20+?

Utilizing current financials and the arguably conservative VesselsValue numbers along with a premium for above-market charters, I derive an adjusted net asset valuation (“NAV”) of about $22/unit. Unfortunately, as I’ve learned for the past 3-years, the market is either too skeptical or too basic (depending on your viewpoint) to value these vehicles on anything but yield.

So CPLP is worth $22/unit, or arguably about $20/unit with a slight LP discount, but it’s never gonna get there without at least a $0.50/qtr payout. Your move, CEO Jerry Kilogratis (and arguably moreso C-Mar behind the scenes), do you want to trade at $15 or $20? The decision is theirs based upon management’s future distribution choices. Will they finally start pulling the levers to higher unit pricing? If so, strap in for huge gains ahead.

Next Steps? 9K TEU Extension

The next step for CPLP is to extend their trio of 9K TEU containerships which expire over the coming year. Their current rate is $39,250/day, which is pretty close to my current market estimate of about $35k/day without scrubbers or about $40k/day with an upgrade. The fate of the “Cape Agamemnon” is also TBD (current market rate close to $20k/day), but I expect a divestiture.

Source: Capital Product Partners, Q3-19 Presentation, Slide 6

Conclusion: Raising Fair Value Estimate to $16.00

Capital Product Partners is executing very well and I believe the latest dropdown deal is fair. I’d rather see unit repurchases at these bargain prices, but management has been exceedingly clear on their intentions to grow the fleet and they are following through on their guidance.

Logically, CPLP should trade close to NAV minus a small captive-LP discount, but we all know that yield is the only thing this market cares about. I’m raising my ‘fair value estimate’ to $16, which is backed by NAV (30% discount), but also based on the expectation of higher payouts soon.

Last Chance for 2019 Research Rates

We’ve been contrarian shipping investors at Value Investor’s Edge, which wasn’t popular recently, but our performance speaks for itself. Values remain very attractive and we’ve recently released our 2020 Model Portfolios. We’re offering two-week free trials and a last chance to lock-in 2019 pricing.

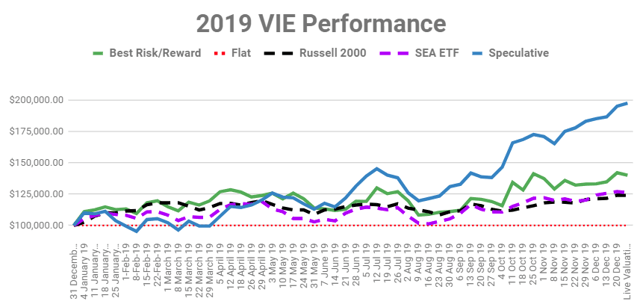

In 2019, our models averaged +69% YTD compared to the Russell (+24%) and industry-comp $SEA (+26%). Prices increase significantly on 6 January, join now to review our 2020 picks and lock-in lower rates.

Join for FREE with a two-week trial!

Disclosure: I am/we are long CPLP, DSSI, NMCI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

{kind=link}