Abstract

BACKGROUND: Brand discount cards have become a popular way for patients to reduce out-of-pocket spending on drugs; however, controversy exists over their potential to increase insurers’ costs. We estimated the impact of brand discount cards on Canadian drug expenditures.

METHODS: Using national claims-level pharmacy adjudication data, we performed a retrospective comparison of prescriptions filled using a brand discount card matched to equivalent generic prescriptions between September 2014 and September 2017. We investigated the impact on expenditures for 3 groups of prescriptions: those paid only through private insurance, those paid only through public insurance and those paid only out of pocket.

RESULTS: We studied 2.82 million prescriptions for 89 different medications for which brand discount cards were used. Use of discount cards resulted in 46% higher private insurance expenditures than comparable generic prescriptions (+$23.09 per prescription, 95% confidence interval [CI] $22.97 to $23.21). Public insurance expenditures were only slightly higher with cards: an increase of 1.3% or $0.37 per prescription (95% CI $0.33 to $0.41). Finally, out-of-pocket transactions using a card resulted in mean patient savings of 7% or $3.49 per prescription (95% CI −$3.55 to −$3.43). The impact varied widely among medicines across all 3 analyses.

INTERPRETATION: The use of brand discount cards increased costs to private insurers, had little impact on public insurers and resulted in mixed impacts for patients. These effects likely resulted from private insurers reimbursing brand drug prices even when generics were available and from discount cards being adjudicated after claims were sent to other insurers in most cases. Patients and their clinicians should recognize that discount cards have mixed impacts on out-of-pocket costs.

Over the past decade, many popular drugs have lost their patent protection and have become available as generics.1 As the prices of brand name medications are typically greater than the prices of equivalent generics, many individuals switch to a generic once available, and insurers often impose rules to maximize the use of generic drugs. In an effort to maintain market share without reducing list prices, many brand manufacturers have introduced patient discount cards.2,3 In Canada, patients can obtain these cards through multiple sources, which include signing up on websites or obtaining them from pharmacies and from physicians’ offices. The cards are adjudicated at the pharmacy in a manner similar to an insurance plan to reduce the cost of the prescription for a branded product.4 Since their introduction, these discount products have been widely used: a coupon was used for an estimated 20% of brand prescriptions in US commercial insurance plans in 2016,5 and more than 1.5 million individuals have signed up for a single provider’s cards in Canada.6

These discount cards have been controversial because of their potential impact on drug expenditures. Although the cards are generally thought to cover enough to make the patient’s copayment similar to that of an equivalent generic, costs to insurers for the remaining portion of the drug can be higher.2,6 This increase in cost for the insurer occurs because the difference in cost between the branded product and the generic is covered only for the patient and not for the insurance plan. In particular, this increased cost is more likely when the claim is sent to the insurance plan for adjudication before the card is applied, making it seem to the insurer that the patient is filling a standard brand prescription. For this reason, in the United States these cards are prohibited in public insurance plans (including Medicare and Medicaid), and 3 states have either laws or pending legislation limiting their use.7 Legislation has also been passed in the province of Quebec to limit their use, but the accompanying regulations have not been developed, and this aspect of the law is therefore not in force.8 The cards remain legal, therefore, in private plans in the US and for both public and private insurance plans in Canada.

Despite the controversy surrounding their use, we are not aware of any studies that have directly quantified the impact of these cards on the amounts paid by private insurers, public drug plans and patients. There have been a few US studies comparing branded products with these discount programs and their generic competition, which found mixed impacts on adherence and cost.9–11 However, these studies were mostly descriptive and unadjusted, and the economic impact of discount cards remains unclear. Therefore, we used comprehensive pharmacy adjudication records to study the use of discount cards and their impact on costs for different payers in Canada.

Methods

Study setting

Although Canada operates a universal national insurance program for physician and hospital services, prescription drugs are funded through a mix of public coverage, private benefits coverage (which is largely employer-based) and out-of-pocket patient charges. Before the introduction of discount cards, it was not typical for branded manufacturers to lower prices when generic alternatives became available. Brand discount cards can be used in conjunction with any type of plan and are adjudicated at the pharmacy in the same fashion as any other public or private insurance plan. We focused on cards that offered discounts on branded products for which a generic equivalent was available (as opposed to new drugs without approved generics).4

Data sources

For our study, we used pharmacy adjudication records from across Canada that were provided to Sea to Sky Health Ltd., a health data research and consulting company owned by one of us (M.L.), by a large, national data source. This data set consisted of a convenience sample of pharmacy adjudication records from the automated systems used to process claims at more than 1000 community pharmacies across Canada, including every province and age group. These data included information on patients who used 1 or more discount cards between September 2014 and September 2017. The data set included both the transactions using a brand discount card and all transactions from the same individuals involving equivalent generic drugs from the automated systems that process claims.

We assessed the validity of our data using several checks, including assessing the range in values for the individual variables, identifying trends over time in the use of medicines with cards and comparing prices with those on the Ontario public formulary for a random subset of 100 specific medications with more than 1000 claims (selected by Drug Identification Number). All of these values were within 5% of what would have been expected on the basis of allowable ingredient costs and markups. Because the data set was derived from actual pharmacy adjudication records, there were no missing data. Our research team was provided with the original raw data, performed all data cleaning, designed the analytic approach and derived all of the results presented below.

For each transaction, we obtained information on each payer that contributed to payment (including dispensing fees and markups), specifically private benefits plans, public (government) insurance programs and cash payments from individuals. Our data set outlined the order in which payments from different sources were adjudicated, and how much each paid toward the total cost of each prescription. This ordering is important because if insurance plans cover a percentage of the total cost and are adjudicated before a discount card, then they will pay a higher portion of the total cost.

From the data set of transactions using a brand discount card, we derived 3 distinct cohorts of prescriptions: a private benefits cohort, a public benefits cohort and a cash cohort. First, to isolate the impact of discount card use on private insurance plans, we selected transactions for which a private benefit plan paid a portion, with no public drug plan paying any portion (the private benefits cohort). Then, we selected transactions for which a public drug program paid a portion of the transaction, with no private benefit plan paying any portion (the public benefits cohort). Finally, we selected transactions in which only cash payment from the patient was involved (i.e., no private or public drug coverage, the cash cohort). In cases in the private benefits plan cohort in which multiple plans were used (e.g., a spousal plan in addition to the person’s own plan), we summed all plans.

Statistical analysis

For each of the 3 cohorts of prescriptions, we matched the claims to equivalent generic prescriptions on the basis of exact matches for the following characteristics: active ingredient, based on Health Canada Active Ingredient Groups; dosage strength; form (e.g., tablet, extended-release capsule); quantity; and province of dispensation.

With these equivalent prescriptions, we compared the difference in cost for the brand prescription using a discount card and for equivalent generic prescriptions for private benefits plans, public drug plans and patients. We calculated 95% confidence intervals (CIs) for these differences and tested statistical significance using t tests.

Ethics approval

This study was approved by the University of British Columbia Behavioural Research Ethics Board.

Results

Over the period of our study, brand discount cards were used 2.82 million times for 89 different medications. Over the 3 years we studied, monthly use of brand discount cards grew by 67% (Appendix 1, Figure 1A, available at www.cmaj.ca/lookup/suppl/doi:10.1503/cmaj.190098/-/DC1). Cards were used slightly more often by women (54%), and the average age of patients was 50 years. Use of discount cards was heavily concentrated within a few medicines: the top 5 in terms of utilization numbers (rosuvastatin, buprenorphine/ naloxone, methylphenidate, escitalopram and atorvastatin) accounted for 53% of all cards used. By drug, discount cards paid a median of 44% of the cost of each prescription when they were used, but there was substantial variation in this number (interquartile range 29% to 55%). This percentage did not substantially increase or decrease over our study period (data not shown). In terms of payer order, in most cases (88%) payment claims for the drug was submitted to private benefits plans before the discount card.

Private benefits cohort

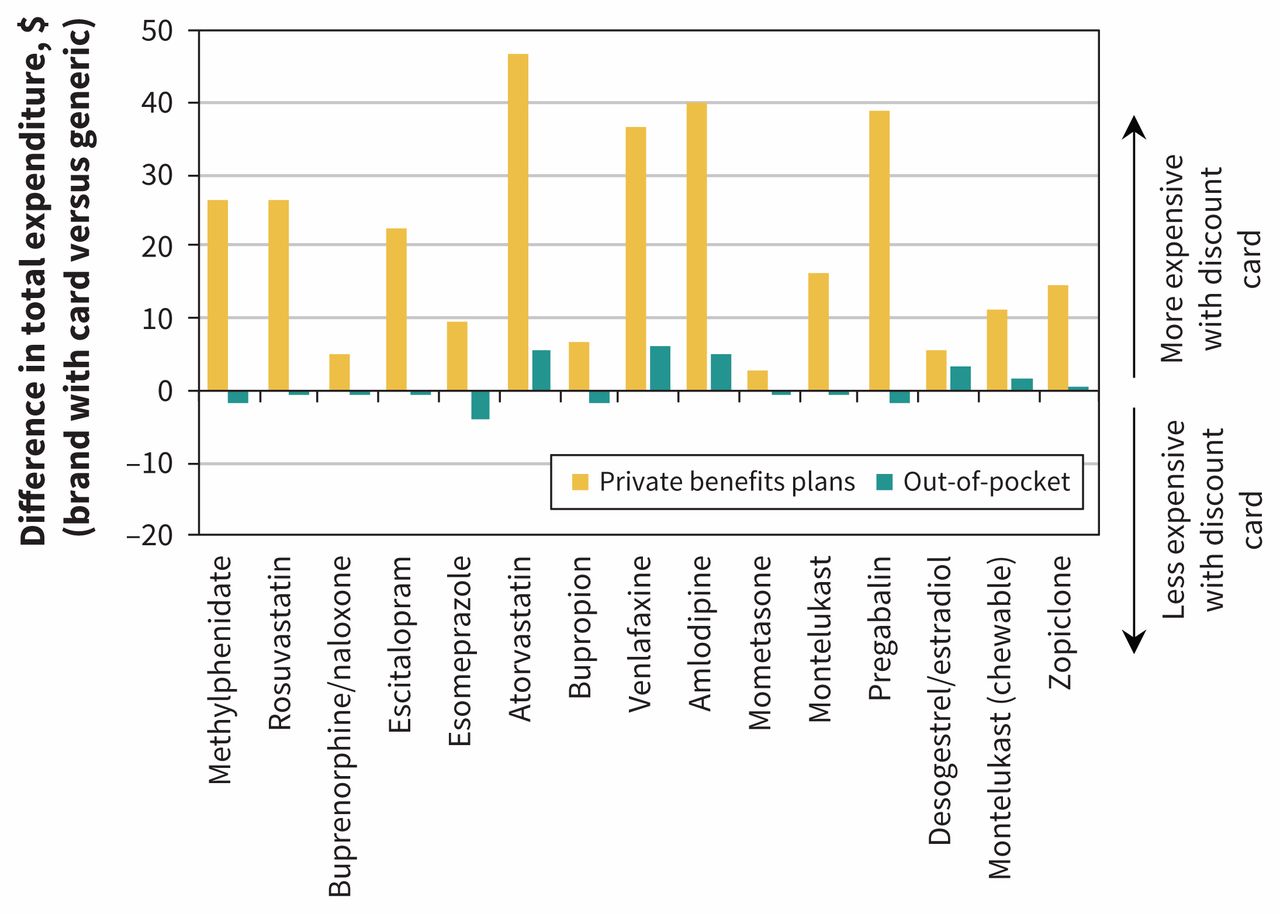

Our cohort contained 939 608 claims that involved a private insurer and no government payment (top 15 shown in Appendix 1, Table A1), which we compared with 995 149 equivalent generic claims. Overall, third-party insurers paid $69.4 million toward these claims compared with an estimated $47.7 million for the same mix of equivalent generic prescriptions. This equates to an increase of $21.7 million, or 46%. On a per-prescription basis, this represented a cost increase of $23.09 (95% CI $22.97 to $23.21) for private insurers. This increase in expenditure extended to all of the individual drugs that we studied: in every case, use of a brand card led to higher expenditure for private drug plans in comparison with equivalent generics. Figure 1 shows the estimated change in expenditure for the top 15 most popular discount cards, where the per-prescription increase by drug for private insurers ranged from $2.90 to $46.91.

Average change in reimbursement per prescription for private insurers and individuals for the top 15 medicines using brand discount cards when compared with equivalent generic prescriptions without a discount card (limited to prescriptions with only private insurance and out-of-pocket payment). Positive values represent increases in reimbursement when a brand discount card was used relative to an equivalent generic.

In contrast, there was little overall change in the out-of-pocket component for these prescriptions. Patients paid $7.1 million toward the prescriptions with a brand card, compared with the estimated $7.2 million they would have paid for the same mix of generic versions, for a difference of $108 000. This represents a 2% saving per prescription for patients, or a $0.12 saving (95% CI −$0.15 to −$0.08). As shown in Figure 1, the change in out-of-pocket expenditures by patients for the top 15 drugs was much smaller than for insurers, ranging from an average saving of $4.15 to an additional cost of $6.19.

Public benefits cohort

We found a similar number of claims, 901 200, with payment from a public drug plan and no private insurer payment (top 15 shown in Appendix 1, Table A2). These claims were compared with 1.45 million equivalent generic drug claims with the same payment characteristics. Overall, government plans paid $26.0 million toward these claims when a discount card was used, and we estimate they would have paid $25.7 million for equivalent generics, for a difference of $334 000. This represents an increase of 1.3%, or $0.37 per prescription (95% CI $0.33 to $0.41). As shown in Figure 2, the change in public drug plan expenditure was comparatively small, ranging from a saving of $1.43 per prescription to an increase of $2.49 per prescription.

Average change in reimbursement per prescription for public drug plans and individuals for the top 15 medicines using brand discount cards when compared with equivalent generic prescriptions without a discount card (limited to prescriptions with only public drug program and out-of-pocket payment). Positive values represent increases in reimbursement when a brand discount card was used relative to an equivalent generic.

Overall, patients paid $4.1 million for brand prescriptions in this cohort, whereas equivalent generics would have cost $2.4 million. This represents an estimated increase in out-of-pocket payment of $1.7 million, or $1.86 per prescription (95% CI $1.84 to $1.88). As shown in Figure 2, there was substantial variability in this impact for patients, with many drugs in the top 15 showing virtually no effect on out-of-pocket payments, whereas 4 had much higher per-prescription amounts: from $4.78 higher for clopidogrel to $11.71 higher for atorvastatin.

Cash cohort

Our final analysis focused on transactions involving only out-of-pocket payment from the patient (i.e., no private or public drug coverage). There were 376 838 such transactions that used a brand discount card, which we compared with 355 426 claims for equivalent generics (top 15 shown in Appendix 1, Table A3). Overall, patients paid $17.3 million for the branded prescriptions with a discount card, and we estimated that they would have paid $18.7 million for equivalent generics. This represents a saving of $1.3 million or 7% on out-of-pocket payments, or an average of $3.49 per prescription (95% CI −$3.55 to −$3.43). As shown in Figure 3, there was variability in these values for the top 15 drugs, ranging from a saving of $13.44 per prescription to an increased cost of $8.44 per prescription.

Average change in out-of-pocket payments per prescription for individuals using brand discount cards when compared with equivalent generic prescriptions for the top 15 most frequently used cards (limited to prescription claims with only out-of-pocket payments). Positive values represent increases in patient payments when a brand discount card was used relative to an equivalent generic. For desogestrel/estradiol, “28” indicates Marvelon 28, and “21” indicates Marvelon 21.

Interpretation

We found that the use of drug discount cards issued by the manufacturers of brand name drugs has increased in Canada and that the cards are used for a wide range of different drugs. Overall, we found that the impact of these cards on drug expenditures depends on the payer in question: the cards universally and substantially increased expenditures by private insurance companies but had very little impact on public drug plan expenditures. In terms of out-of-pocket payments, the impact differed according to both insurance status and the specific drug in question: in some cases patients saved money using a discount card, whereas in other cases they spent more.

The difference in impact between private insurers and public drug plans likely arises from the different payment rules in these plans. Although nearly every public drug plan in Canada will pay only the generic price when a generic is available (even when a brand version is dispensed),12 this is not the case for many private drug plans. In fact, only about half of private drug plans in Canada have rules whereby they will pay only the amount of the equivalent generic when one is available.13 Our study provides empiric evidence that drug discount cards represent a way for pharmaceutical companies to leverage this discrepancy while making patients’ copayments nearly equivalent, so as not to deter them from filling their prescriptions with branded medicines. This occurs despite the fact that, in most cases, it is not necessary to use the brand name version of a drug molecule when a generic alternative is available, as evidenced by many studies showing clinical equivalence between branded products and their generic counterparts.14–16 Finally, we observed much heterogeneity in the impact on cash payments by patients, which likely resulted from different adjudication rules for different medications.

Limitations

Although our study benefited from use of a very large, national data source and strong comparisons through the use of equivalent prescriptions, there were also some limitations. Because the data did not constitute a comprehensive record of all prescriptions received by the individuals included in the study, we were unable to assess the extent to which the brand discount cards affected important outcomes such as medication adherence. Our data set was a convenience sample and did not contain information on claims at every Canadian pharmacy. However, we have no reason to believe that the adjudication rules of the discount cards, public insurers and private insurers would vary elsewhere. Our study was completed during a period when generic drug prices were decreasing in Canada. However, if this timing resulted in any bias, it would be conservative in direction and would result in our underestimating the true effect on private insurers. Furthermore, although our results are clearly relevant to Canada, it may not be appropriate to extrapolate them completely to other countries with different reimbursement regimes. However, we believe that the impact of cards on private insurers may be even higher in the US, given that country’s lower generic drug prices and the fact that these programs exist for a larger number of drugs in the US.17 It remains unknown how different insurance rules — most notably the more common use of tiered copayments in private drug plans in the US versus the more common use of coinsurance in Canada — would modify the impact.18,19 Finally, we were unable to assess whether the use of brand discount cards affected private insurance plan premiums.

Conclusion

The use of brand discount cards is increasing in Canada, and their impact depends on the payer in question. Given that our analysis showed large increases for private plans, employers might consider adopting more stringent generic substitution policies to ensure value for money in drug spending. While governments need not make such changes, they should be aware of the potential for increased out-of-pocket payments with some drugs and for expenditures in the private drug plans for government employees. Finally, regardless of whether they hold insurance, individuals should check relative prices at their pharmacy between the brand with a discount card and the equivalent generic, given the possibility that they may be worse off financially if they use a card. Clinicians should inform their patients that differences in cost exist between brand name and equivalent generic drugs, particularly if they are involved in distributing these cards. Future studies should rigorously evaluate the clinical impact of brand discount cards, such as effects on adherence rates relative to non–card users.

Footnotes

-

Competing interests: Michael Law has consulted for Health Canada, the Hospital Employees’ Union and the Conference Board of Canada, and he has provided testimony as an expert witness for the Attorney General of Canada. Mark Harrison holds the UBC Professorship in Sustainable Health Care, which is funded by Amgen Canada, AstraZeneca Canada, Eli Lilly Canada, GlaxoSmithKline, Merck Canada, Novartis Pharmaceuticals Canada, Pfizer Canada, Boehringer Ingelheim (Canada), Hoffman-La Roche, LifeScan Canada and Lundbeck Canada. No other competing interests were declared.

-

This article has been peer reviewed.

-

Contributors: Michael Law conceived of the study; acquired, analyzed and interpreted the data; and drafted the manuscript. Heather Worthington, Mark Harrison and Fiona Chan contributed to designing the work and interpreting the data, and revised the manuscript for important intellectual content. All of the authors approved the final version to be published and agreed to be accountable for the work.

-

Funding: Michael Law received salary support through a Canada Research Chair and a Michael Smith Foundation for Health Research Scholar Award. Mark Harrison received salary support through a Young Investigator Salary Award from The Arthritis Society (YIS-16-104) and a Michael Smith Foundation for Health Research Scholar Award 2017 (no. 16813).

-

Editor’s note concerning data sharing: The provider of the database used for this study specified that the health research and data consulting company (Sea to Sky Health Ltd.) enter into a confidentiality agreement in order to have access to the data. As a result, CMAJ does not know the identity of the data provider and therefore cannot act as a guarantor for the data used, and the data are not available to others.

-

Disclaimer: The data provider and the pan-Canadian Pharmaceutical Alliance (pCPA) had no role in funding the study, developing the research methodology, conducting the analysis or interpreting the results, nor in the decision to seek publication. In addition, the pCPA had no role in the provision of the data for this study. The pCPA was consulted during this study and, as a policy-maker, was interested in the subject matter.

- Accepted October 2, 2019.

{kind=link}