It is difficult to predict what consequences the current health crisis will have on the insurance industry but it can be said with certitude that all insurers will not be impacted in the same way.

Also, it looks like the rotation away from tech and high growth stocks is likely to continue as people take profits and invest more in other sectors, one of them being financials.

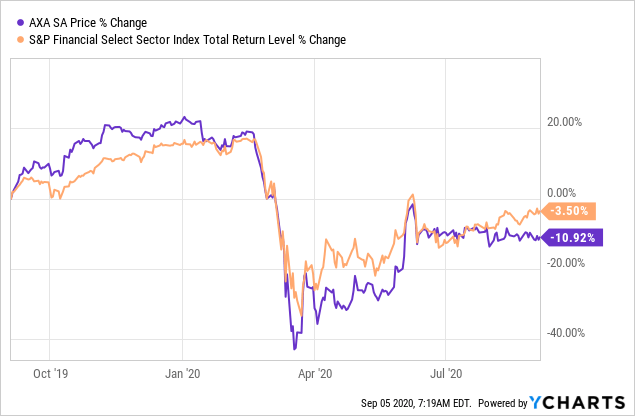

Now AXA (OTCQX:AXAHY) is a French insurer which has not yet recovered from the March lows despite having some strong fundamentals going into the crisis.

Figure 1: AXA stock price v/s S&P Financials Total Return.

Data by YCharts

Data by YCharts

Moreover, due to the completely exceptional nature of COVID-19 which caused the shutdown of a large number of activities throughout the planet in an environment of globalization and working-from-home means a lack of precedent to learn from.

Hence, I will lay a lot of emphasis on risks.

First, it is important to provide investors with some visibility as to the nature of insurance claims pertaining to the coronavirus pandemic.

Higher commercial insurance claims

Some will remember that in May, the Paris commercial court ordered AXA to compensate a Parisian restaurant owner for two months’ loss of revenues due to confinement-related business interruption, a closely watched event both by the insurance industry and retail sector.

In its response, the French insurer said it intends to make an appeal as to the court decision due to ambiguity in the contract as to the meaning of “pandemic coverage.” Moreover, the CEO, Thomas Buberl specified that out of the 20,000 restaurants insured by the French insurer, less than 10% (numbered 1700) actually had contracts similar to that of the Parisian restaurant owner.

In terms of impact, these claims have essentially been hitting the commercial business, more specifically, AXA XL, AXA’s subsidiary.

Going into more details, first, the fact that part of insurance premiums are indexed on business activity of owners, a fall in activity entails lower revenues for insurers like AXA.

Second, smaller and medium-sized companies which have been severely impacted with most located in France require support measures.

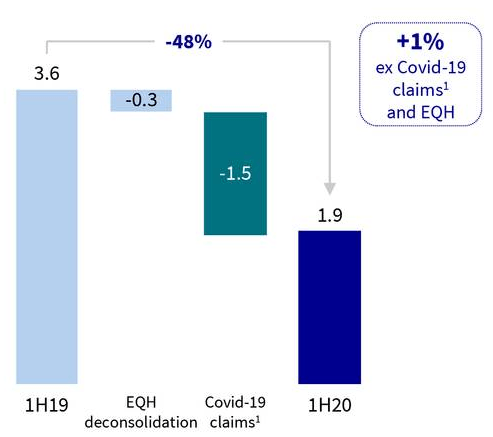

As a result earnings have decreased to €1.9 billion ($2.25 billion) compared to the 3.6 billion euros ($4.26 billion) during the same half last year.

Figure 2: Earnings impact by COVID and debt repayment

Source: Seeking Alpha

The main reason for this decrease was COVID-19 claims and also some US civil unrest costs reaching €1.5 billion. US riots expenses negated €100 million out of earnings.

Also, the group incurred a deconsolidation debt of €0.3 billion with respect to its previous stake in Equitable Holdings (EQH).

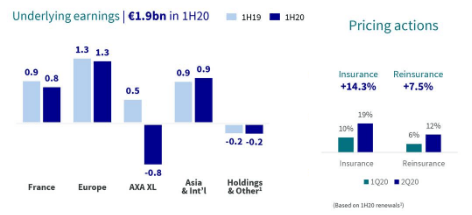

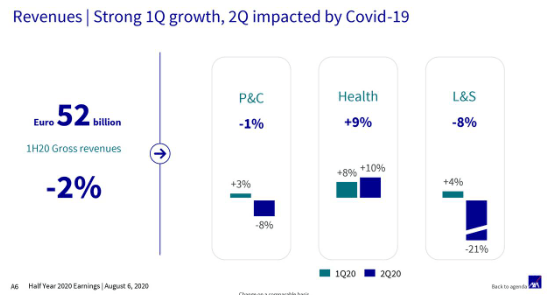

Furthermore, as for revenues this time, Property and Casualty (P&C), which is AXA’s largest line of business showed resiliency helped by higher prices which managed to offset lower volumes.

Figure 3: Impact of AXA XL on earnings

Source: Seeking Alpha

Going into the second half, due to the ongoing restructuring at AXA XL, aimed at focusing on disciplined underwriting, AXA should benefit from positive pricing actions both in the insurance and re-insurance segments.

At the same time, the group has been reducing its property category exposure by reducing the maximum risk limit from €50 million per risk to €25 million per risk.

These measures should strengthen AXA XL to face the possible surge in claims because of hurricane Laura, a deadly and damaging Category 4 Atlantic storm which hit the US in the last week of August.

In this case, the P&C business should be impacted while reinsurance should help mitigate some losses.

In this respect, the reserve level surplus at AXA XL stood at €0.5 billion, down from €0.8 billion due to the COVID-19 impact.

Now, I move to the brighter side of the picture by covering sectors of activity that have been positively affected by the crisis.

First, the health business has been performing well and ended up emerging stronger. One of the reasons is that people in developed markets, as a result of confinement measures have paid fewer visits to health professionals and therefore submitted less claims for reimbursement.

In the meantime, they have continued to pay monthly insurance premiums to AXA.

Second, in developing and emerging markets, more people are subscribing to insurance plans given the higher post-COVID-19 period health awareness. One example is China, where strong growth is being seen.

Figure 4: Revenue for H1-2019 and H1-2020

Source: Seeking Alpha

Third, in addition to the health segment which contributes around 20% to earnings, the fact that people have driven their cars to a lesser extent during stay-at-home measures has resulted in fewer motor insurance claims.

Fourth, geographical diversification which is a strong positive for AXA, has also helped to mitigate the effects of the coronavirus pandemic as not all regions of the world have been impacted by COVID-19 in the same way. In Asia for example, there has been earnings growth.

However, this health crisis will undoubtedly be followed by an economic downturn which will result in bankruptcies and a reduced activity level for those companies that have been spared in the first wave of the pandemic.

Therefore, going forward, it is important for the balance sheet to be strong.

The balance sheet

AXA has several positives going into the crisis.

First, its transformation plan launched in June 2016 is nearing completion in terms of deleveraging and the group has sold its remaining stake in AXA Equitable Holdings and repaid associated debts. This has strengthened capitalization.

Figure 5: Transformation plan launched in 2016.

Source: www.axa.com

Second, the balance sheet has proven to be resilient with the solvency ratio standing at 180%, in the 170-230% range as per 2016 financial objectives and well above the regulatory requirement of 150%.

According to the executives, this should be incremented further in the second half by way of disposals estimated to be at 6% as well as through integration synergies of AXA XL at 5%-10%. For that matter, the French insurer completed the acquisition of the XL entity back in September 2018.

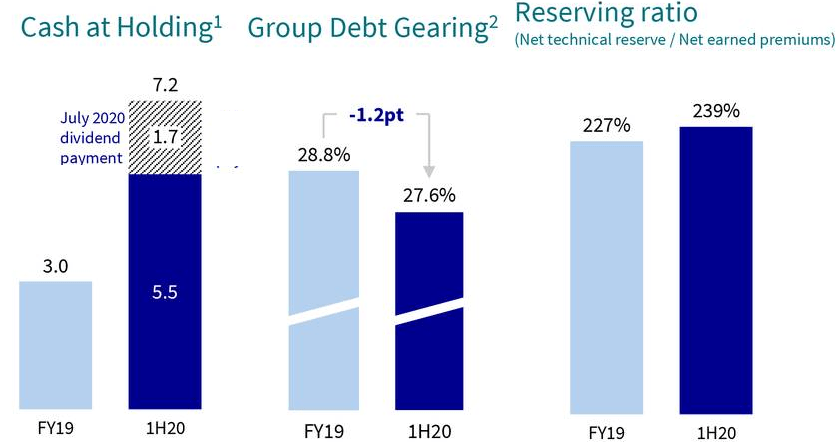

Figure 6: Cash at Holding and group gearing ratio

Debt gearing range has been reduced and it is aimed to reach the 25%- 28% level by the end of 2020. Cash is significantly up despite having been impacted by the July 2020 dividends payment.

Reserving ratio is up, reflecting notably additional COVID-19 reserving from 227% to 239%. This ratio provides an indication as to the adequacy of the reserves in relation to new risks being written as determined by the net earned premium.

Even more important are the IFRS reserves which are in excess of the undiscounted Solvency II (EU directive that harmonizes insurance regulation) requirements’ best estimate liabilities.

The reserves stand at €6.6 billion, down from €6.8 billion after the 0.3 billion reduction incurred at AXA XL being partially offset by a €0.1 billion gain in Europe.

As for a comparison with peers, Fitch Ratings ranked AXA’s business profile as ‘Most Favorable’ compared with that of other European-based multinational insurers in July 2020.

In addition the group was attributed a “Very Strong Capitalization” as measured by Fitch’s Prism factor-based capital model. This represents an improvement from 2018 and is due to a reduction in AXA’s exposure to market risks.

In addition, Fitch Ratings mentioned that the capitalization is resilient to pandemic stress and the agency “does not foresee a material weakening of AXA’s capital strength in the medium term.”

Therefore, these are strong positives for AXA but as a risk-averse investor, I look at other possible challenges in this uncertain world.

Other risks

First, the current low interest rate environment prevailing on both sides of the Atlantic puts pressure on the profitability of insurance companies, in particular on the life insurers with policy guarantees. Hence in AXA’s Life & Savings business, General Account suffered from revenue shortfall.

On the other hand, AXA is seeing progress in its capital-light unit-linked insurance products as the insurer is changing its product strategy to focus more on products like integrated wealth management.

Also, personal protection covering risks related to an individual’s physical integrity, health or life is progressing too.

Second, other risk factors which just six months back had never been heard of are emerging. In this context, in the US and UK, COVID-19-related business interruption insurance coverage has been a “hot” topic even involving legislative debate and governmental talks. There have been a call for insurance companies to cover some of the related risks.

To counteract these, insurance industry groups like the NAIC (National Association of Insurance Commissioners) and Association of British Insurers (“ABI”) have clearly voiced out their concerns affirming that very few contracts actually include pandemic coverage.

Equally important in this case, AXA’s executives also see limited probability of amendment of contracts in favor of the businesses making the claims.

Finally, there are risks as to the very payment of dividends. In this context, AXA has already paid a dividend of $0.8272 in July representing 50% of the total dividend it pays for the year. Interestingly, the group’s financials do indicate that a dividend payment is possible in the second half but they were prevented in doing so by the ACPR (French Insurance Regulator).

To sum it all, there are risks but with its flexible business mix, strong financial position and support from industry lobby groups, AXA should not be significantly impacted. Also, during the earnings call, the executives have clearly shown a willingness to reward shareholders with dividends.

Valuations and Key takeaways

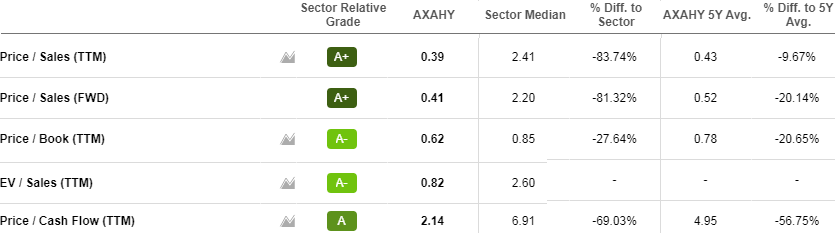

AXA looks to be undervalued based on the Price/Sales and Price/Book ratios and should be at a higher price. My target, also taking into consideration underperformance with respect to the S&P Financial index is for a $23-24 range while waiting for more visibility during the third quarter results.

Figure 7: Valuation metrics.

Source: Seeking Alpha

The fact that the stock price has started lagging the financial index as from July after being aligned with the latter for the most part of the year shows that the decision of the ACPR on dividends had some negative effect. Thus, there seems to have been a lack of interest from income-seeking investors to invest.

On the other hand, there has been no abrupt sell-off which is a testimony to confidence that, in the longer term, it is unlikely that the ACPR would continue to veto the payment of dividends as this would be counter-productive for France’s marketplace and economy.

A worst-case scenario is that the current dividend level (4%) will be maintained while not being increased further, which given the present low interest rate environment is not bad from an income point of view.

This said, AXA has increased reserves to meet financial obligations with respect to the insurance policies it has issued and its restructuring, initiated at the right time four years back puts it in a position of force to tackle claims associated with a re-insurgence of COVID-19 in some parts of the world and the explosion in Lebanon.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in AXAHY over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This is an investment thesis and is intended for informational purposes. Investors are kindly requested to do additional research before investing.

All figures except dividends are provided in EURO in line with the figures. Whenever, a conversion has been made, the currency rate of 1 EURO = 1.18 USD has been used.

{kind=link}