Executive Summary

Throughout the first half of 2020, the market has penalised Avis Budget Group Inc (CAR) with views of limited upside, amidst severe restrictions in air passenger traffic and alternative ride-sharing companies stealing market share from rental cars.

However, bastion-like liquidity management in facing out the pandemic coupled with sound fundamentals at the current price of $28.89 (at time of writing), provides a rousing entry point and an equally strong investment case for those with an intermediate horizon. Expectations of a rebound in air travel demand over the short to mid-term, demonstrated quality in working capital management and large competitor Hertz’s (HTZ) bankruptcy are certainly catalysts for a dramatic gain in share price, over a medium-term holding period, as discussed below.

Market Considerations

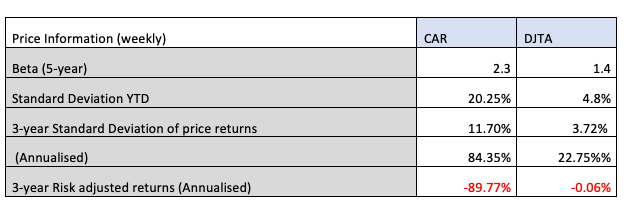

Price returns have shown considerable volatility over the last 3 years, amplified in response to market turbulence since March this year. Standard deviation of price returns at 84% (annualised) rates as exceptionally high compared to the Dow Jones Transportation Average index (DJT) volatility of 25.13% over the same period, to demonstrate. Such information is critical for investors holding a medium-term horizon as the market moves to price in the most recent industry developments, most noticeably in air traffic passenger travel.

Source: YahooFinance CAR; S&P Global Indices DJT

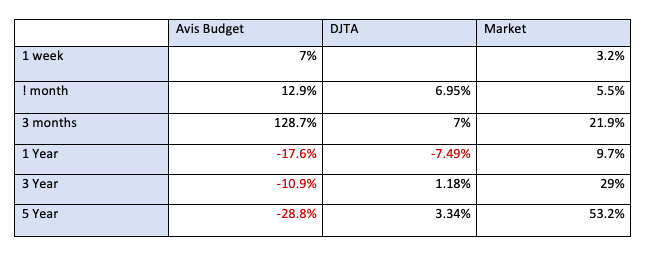

On this background, the stock price has given away over -17% in price returns in the first half of this year having already pulled back from market lows in April. CAR has shown shareholders an additional -10.11% loss in single-year returns over the DJT and subsequently has underperformed the market by approximately -8% over the same period.

Shareholder Price Returns: CAR vs DJT vs Market: Source: YahooFinance CAR; S&P Global Indices DJT;

Source: YahooFinance CAR; S&P Global Indices DJT;

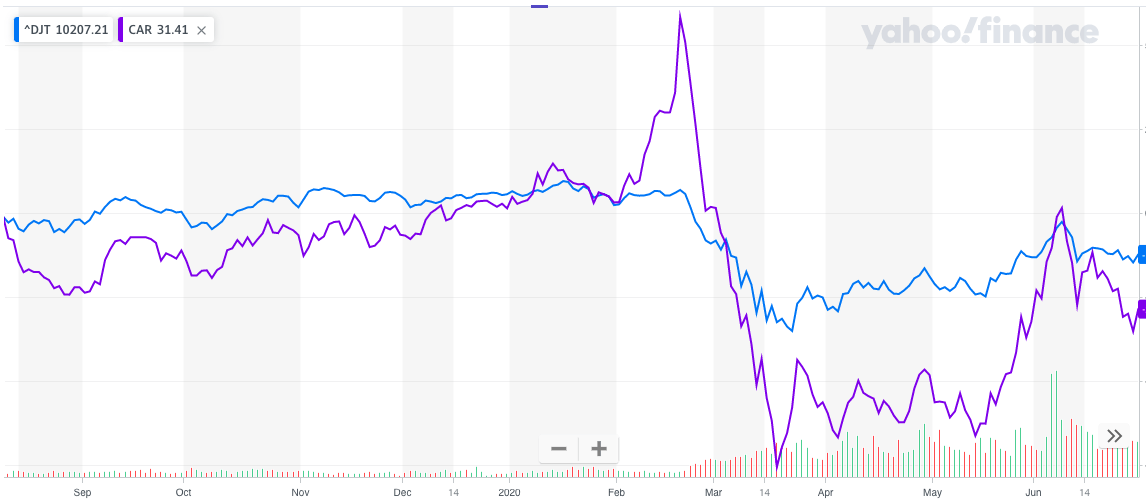

From the company perspective, proactivity from management during the COVID-19 pandemic market turmoil has ensured a solid liquidity position of $1.6 billion in cash and revolving credit facilities, whilst also revising the groups existing senior debt instruments, allowing an additional incurrence of up to $750million in first lien debt. These actions have led to management targeting $400 million in annualised cost savings, with a total $2 billion materialised by April this year; such as cancelling 80% of rental car vehicle orders in March alongside a disposal of 35,000 fleet vehicles in the same month.

On this news, investors seem to have accepted the swift moves from the leadership outfit and can foresee the positives for cashflow following any rebound in air travel, and lifting of restrictions over travel and car-sharing in general. Consequently, the stock price has trudged back to $28.89 from March lows of $7.78 following the market selloff in February 2020.

Source: YahooFinance CAR

Profitability

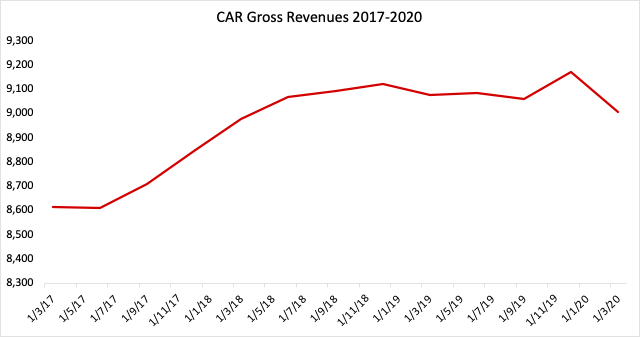

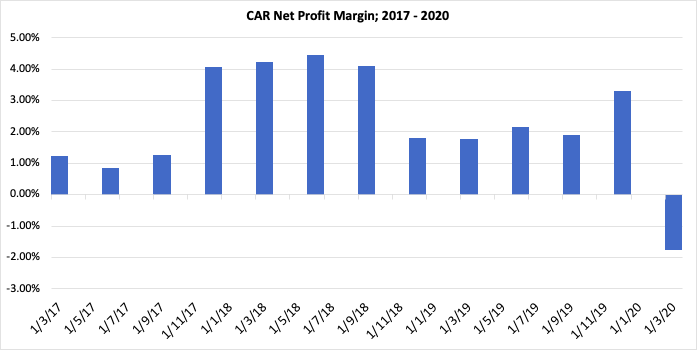

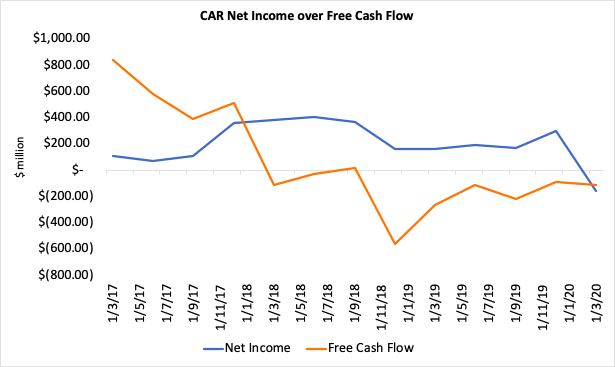

The group has posted solid revenues from 2017 with stable growth until mid 2018. Since then, figures have trended sideways form March 2018 onwards, accompanied by tightening net profit margins and lacklustre FCF over this same period. Revenues have shown stability, however, as have net profit figures for this 3-year period. Undoubtedly, with a smaller rental fleet and significant traffic restriction in air travel and car-sharing, earnings have slumped with a net loss of -$158million and adjusted EBITDA loss of around -$88million posted most recently in May of this year.

In light of this, earnings increased over the single-year period to February by 45%, well above the industry average of -13.1%; this on increase in revenues YTD to February by 9%, prior to the posted first quarter loss this year.

Source: Avis Budget Group 10-K 2019; 2018; 2017

Source: Avis Budget Group 10-K 2019; 2018; 2017

Presently, free cash flow is questionable, at -$91 million by December 2019 and -$108 million for the first quarter of 2020, on revenues of $9.172 billion and $9.005 billion respectively. Analysts confer that this may be the beginning of the j-curve however, with profitability in FCF forecast by mid 2021, as the economy slowly reopens and with capital restructuring.

Earnings are also forecast for growth of ~14% on revenue growth of around 10% over the next 1-year period, obtained from linear regression of analyst estimates, and adjusted for inflation. This is pleasing considering the current state of the entire transportation industry. At this run rate, CAR’s revenue will likely grow faster than the market however earnings will potentially expand further if the group capitalises on market share left over from the Hertz bankruptcy story.

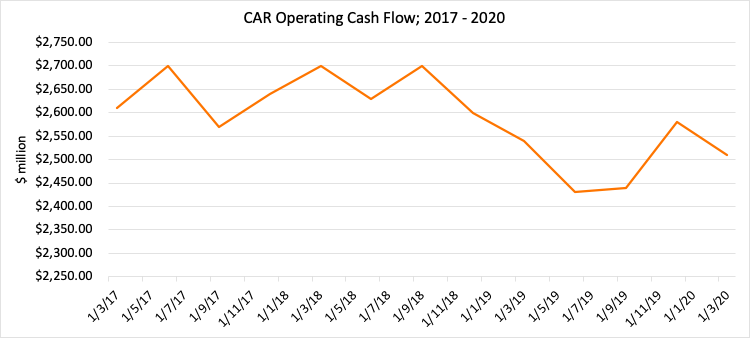

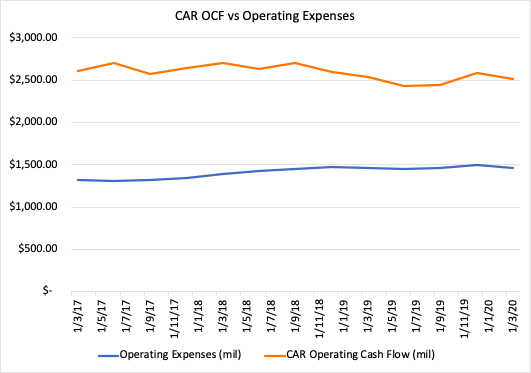

Moreover, now that management has secured an additional $750 million in their revolving credit facilities with relaxed covenants, this will show favourably on ROE and access to operating capital. Coupled with preservation of liquidity and a materialised reduction in operating expenses – as CEO Joe Ferraro has recently mentioned, quick calls to action in removing all “non-essential capital and operating costs” has amounted to approximately $2 billion in annualised cost reductions – this bolsters the case for upheaval in FCF and operating cash flow.

Source: Avis Budget Group 10-K 2019; 2018; 2017; Value Line Research

Cash burn – which is estimated at approximately $900 million for the 2020 second quarter (including retirement of senior notes) – remains marginally covered by operating cash flow at 2.79x coverage. Whilst this may seem as a risk for investors, it pails in comparison to car-sharing competitor Lyft (LYFT) for example, who have -$227.80 million in operating cash flow on operating expenses of $3.5 billion, and have been unprofitable over the TTM.

Source: Annual 10-K Filings 2017-2019; Value Line Research

Source: Annual 10-K Filings 2017-2019; Value Line Research

On EPS in Mar 2020 of $3.15, I am happy with this sentiment in light of the volatility experienced during market recovery, as shareholders have benefitted as much from holding during this period. Previously, EPS hit $4.06 in December 2019, up from $2.27 in the September Quarter, showing support from market participants and propping the case for investment over the intermediate term, especially with the evidenced management strategy for remaining profitable coming out of 2020.

However, with trailing twelve month ROA of 3.2%, this figure sits well below the industry average of 6.9% and shows room for greater efficiency in the asset base, but illustrates resilience in comparison to rental fleet competitor Expedia (EXPE) at -2.5%, by example. ROCE of 3.9% is also quite low in absolute terms and is down from 4.5% roughly 1 year ago and also low relative to EXPE at 6.6%. Thus, investors can use this period as a stress-test for management to observe how working capital shall be deployed and the corresponding impact over ROA and ROCE, because more evidence of competency is needed here to really see the upside in the market.

What is pleasing on this note is consistency in TTM total asset turnover, with every dollar in assets generating 38cents in revenue over the previous three quarters. This has also been fairly consistent on an annual basis over the 3-year period to 2020 and should serve as a solid platform to expand returns from capital with additional liquidity and cost savings measures in place.

Equally as attractive on face value is ROE for shareholders at 80.5% especially in contrast to the industry figure of 14% and over EXPE at -19.4%. This figure is likely unrealised, however, secondary to heightened debt levels secured early this year, because asset turnover and net profit margin remain largely unchanged, as shown in the 3-step DuPont analysis on ROE below. Investors need to be careful not to overweight the ROE figure without the necessary breakdown of where returns are stemming from.

3-step DuPont Analysis of ROE:

| 2019 Annual | 2020 Quarterly | |

| Net Profit Margin | 0.033 | 0.018 |

| Asset Turnover | 0.38 | 0.38 |

| Equity Multiplier / Leverage | 36.63 | 49.24 |

| CAR ROE | 56.45 | 80.5 |

| Industry Average ROE | 14% | |

| EXPE ROE | -19.4% |

Source: Value Line Research

Activity

The global rental fleet totaled approximately 660,000 vehicles by years end 2019 and around 64% of revenues were derived from onsite airport destinations. Of this figure, leisure customers led the way with 60% of revenues derived from this domain for Avis, Budget and subsidiary brands. However, the vehicle fleet has been reduced by 35,000 with further cancellation of 80% of incoming rental vehicle orders for the year. Further cancellations are not out of the question, either. Not surprisingly, the groups long-term capital lease obligation increased from December 2019 reaching $2.198 billion as of March 2020.

CAR Activity Analysis:

Source: CAR 10-Q Quarterly Results 2019 – 2020

On the above points, quality management over liquidity and working capital is also demonstrated from September through to the present as the company seems to be collecting cash faster than it pays. For instance, the cash conversion cycle moving from -41.21 to -51.55 is in parallel with liquidity preservation measures adopted by management early this year. This move is advantageous in the current climate, as the entity has an indirect source of financing from creditors, who will be redeemed on the receipt of customer settlements.

Although potentially disadvantageous to creditors, taking advantage of relaxed covenants over debt facilities in this sense allows faster access to working capital, again injecting liquidity for operations. Relaxed payment terms are also observed in the average payment period of 180 days which will provide additional coverage alongside the typical collection period reducing on average by around 1 week.

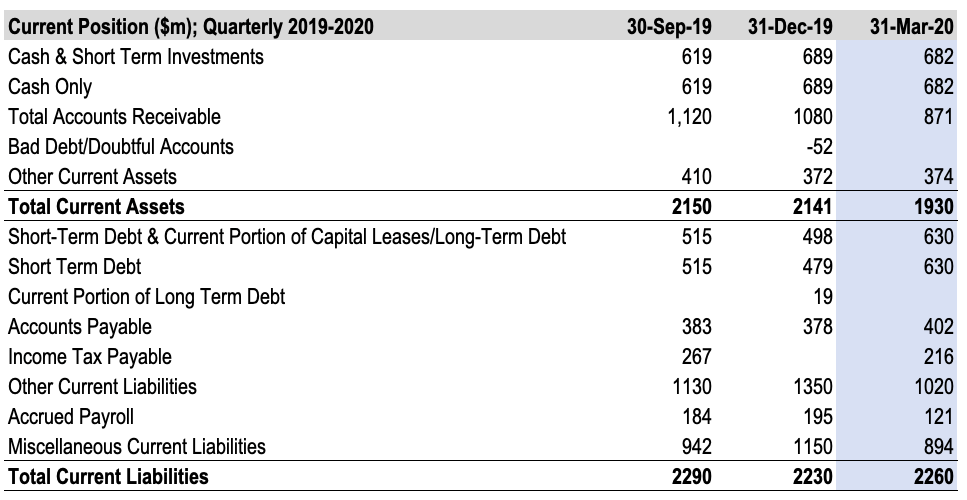

Solvency and Current Position

From a solvency perspective, management have again demonstrated competency in working capital management, relying on primary sources of liquidity and only accessing secondary sources through renegotiation of senior credit facilities and covenants.

Presently CAR has net working capital of -$330 million, but this figure is excluding of approximately $700 million in accessible cash from vehicle programs, which has not been consolidated on the balance sheet – plus an additional $200 million available through the existing revolving credit facility.

Avis Budget Group Current Position:

Source: CAR 10-Q Quarterly Results 2019 – 2020

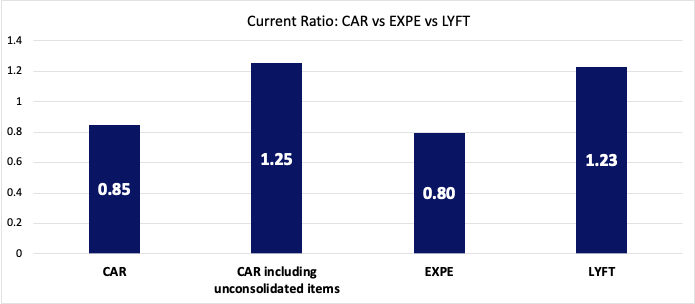

This is extremely important as without this accessible liquidity CAR has a short-term solvency ratio of 0.85 highlighting the company’s short fall in coverage of short-term liabilities, thus presenting default risk in their ability to cover short-term obligations when they fall due. A ratio of 1 or above is optimal in those companies reliant on large capital leases and unavoidable working capital requirements for ongoing operations, such as the case with Avis Budget Inc.

CAR vs EXPE vs LYFT Current Ratio:

Source: Lyft Fiscal Year Results; Expedia Annual Report 2019; CAR 10-K 2019

The above figures illustrate that for every dollar in debt, the company has $1.25 in cash or short-term assets (accessible liquidity included). Thus with the additional cash, CAR is well positioned from a solvency perspective moving into 2021.

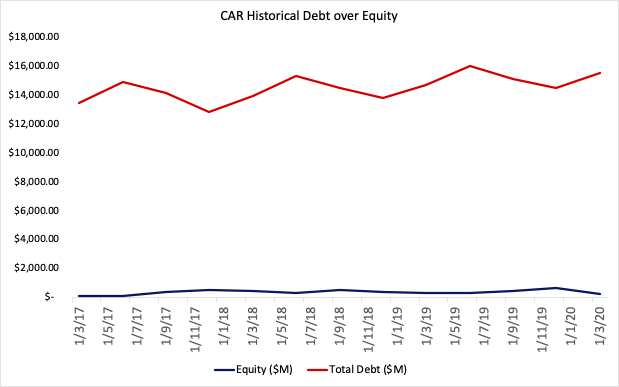

Debt management was also sound over the 3-year period to date through senior revolving credit facilities; the next notes not of maturity until 2023, which will again free up additional cashflow. Aggressive financing of growth through leverage shows a current debt to equity ratio of 62.50 as of March and is up around 139% from the previous quarter, on a debt ratio of 0.77 in the same period, which fortunately has remained stable within 1 standard deviation of the group’s debt ratio mean since March 2019.

CAR Debt to Equity:

Source: CAR 10-K filings 2017-2019; CAR Quarterly 10-Q 2020

Incurrence of the new debt instruments has resulted in short-term debt and capital lease obligations increasing significantly to March, thus impacting interest cover with just 1.7x coverage as of March 2020. On this, however, the large one-off loss in the March quarter has impacted EBIT totals and thus interest coverage and short-term solvency. As travel demand rebounds, earnings and operating cash flow will surely follow suit and so shall interest coverage on the back of these results, particularly as the company aims to snare market share from both rental and car-sharing competitors.

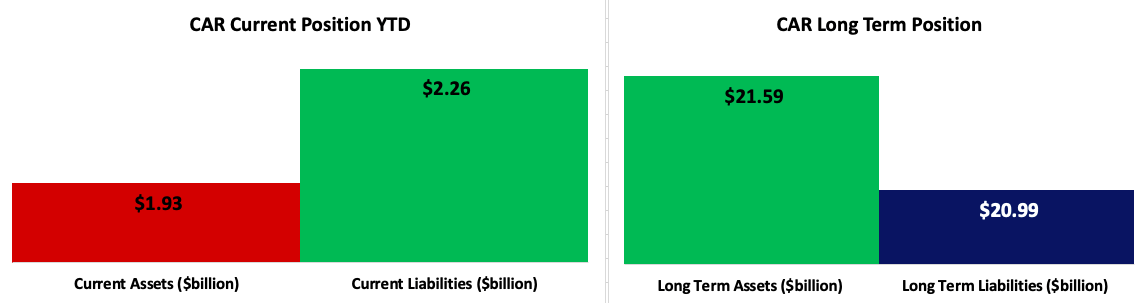

CAR Short and long-term assets & liabilities:

Source: Avis Budget Group Quarterly Filing 2020; Avis 10-K 2019

Valuation

As the company does not pay dividends, one may use FCF to equity, discounting the sum of analyst estimates on FCFE over the coming 5 years to todays value. This time frame would reflect the upper bar of a medium-term horizon for mine. At this point in time I personally don’t believe the equity risk premium is a reliable figure considering high market uncertainty, so I have opted to include opportunity cost of holding the S&P 500 index using the 10-year mean return as the proxy metric, in addition to the current 10-year treasury note yield as the risk-free rate. Such a method allows consistency amongst valuation of additional securities.

| Metric | Source | Figure |

| Risk-Free Rate | 10-year US Government note yield | 0.0059 |

|

Opportunity Cost |

S&P 500 10 year historical mean return | 0.141 |

|

Discount Rate Applied For DCF |

= risk-free rate + opportunity cost of holding S&P 500 index |

0.1469 |

| Shares Outstanding | Market Data | 69.56 million |

| FCFE Figures/Growth | Analyst Estimates | (below) |

| Year | FCFE ($M) | Present Value at Discount Rate ($M) |

| 2021 | $294.65 | $253.35 |

| 2022 | $253.35 | $187.31 |

| 2023 | $230.43 | $146.49 |

| 2024 | $217.37 | $118.82 |

| 2025 | $210.20 | $98.79 |

| SUM | $833.82million | |

| Equity Value Per Share | $11.99 |

Data Sources: Bloomberg US Treasury Yields; S&P Global Indices; Simply WallSt; YahooFinance CAR

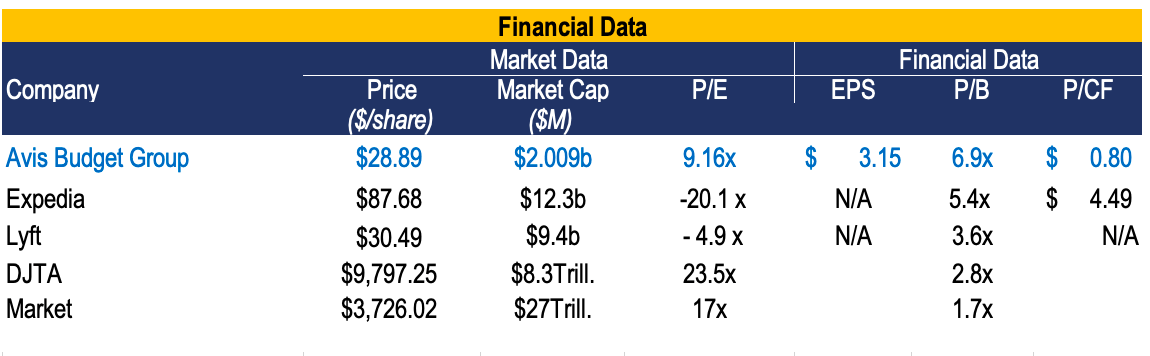

On fair value, the stock price seems quite overvalued at $11.99 on current trading price of $28.89. On a P/E basis however, a multiple of 9.16x is at good value in comparison to competitors and the market multiple of 16.8x, and in particular of the industry multiple of 23.5x.

Although, P/E may not be the best valuation metric for equities at this point in time. Take PayPal’s (PYPL) P/E multiple of 50x compared to the S&P 500 as case in point. It’s the leading tech stock in the index for 2020 and gains have continued to present day, however, whilst one might expect the stock to sit in overvalued territory; further could be from the truth. Krantz agrees. From this, on P/B value CAR is pricier than the market and competitors, however I personally also use P/B as a metric to evaluate performance of management. A P/B greater than 1 demonstrates that value has been created for shareholders, albeit at the premium of 6.9x dollar earnings. Thus, the statement “you get what you pay for” is rampant in equities at this point in time and in addition, considering recent one-off items that have impacted net earnings and EBIT totals this year, further calculations must be completed for an accurate scope of CAR’s valuation.

CAR Valuation:

Source: S&P Global Indices; Avis Budget Group 10-K filings; Expedia Annual Report 2019; Lyft Annual Report 2019

Source: S&P Global Indices; Avis Budget Group 10-K filings; Expedia Annual Report 2019; Lyft Annual Report 2019

EPS and P/CF are not applicable to Lyft as the entity is not profitable, similarly with EPS for EXPE on a background of their most recent earnings. Thus, P/CF is a better metric for comparison in CAR’s case, as it shows true cash figures and strays away from any manipulation of, or slump in earnings. For CAR, this shows a price-to-cash flow of $0.80 per share which is excellent value in absolute terms and in relative to $4.49 elicited by EXPE. Combined with a favourable P/E multiple and decent EPS on these terms, CAR makes a strong investment case for intermediate horizon players on a valuation front.

Risks

Greater evidence is required in cash generation from their deployed capital base, particularly in the short to mid-term, to be measured by ROCE and ROA. Further confirmation of the above is noticed in operating cash flow coverage of long-term debt and capital lease obligations, which have ballooned to $17,592million combined following drains on liquidity this year; whilst short-term obligations are currently at $630million. This presents default risk for Avis Budget Inc if revenues continue along a downward trajectory. Whilst the company is poised to remain profitable moving into 2021, this may largely depend on the rebound in air traffic travel demand, not to mention stagnant economic consumption seeing out the pandemic-backed society.

As airlines begin to reopen, countries are unfortunately seeing the so called “second wave” of the novel coronavirus which has prompted political responses to travel in many states. This presents risks to top line earnings for CAR, as over 60% of revenues in 2019 were in airport rentals, the majority being leisure customers.

In view of this, there are further risks related to the high level of competition in the mobility industry, although CAR seems to be positioned well in comparison to competitors here. Such factors extend to property leases and vehicle rental concessions. There is savage competitiveness in this arena for floor space and businesses bid for the same in rigorous tender processes. Hypothetically, if the entity were to lose a property lease or vehicle rental concession, such as an airport or a train station, there can be no guarantee that they can find a suitable replacement location; and with uncertainty around travel, this is certainly to be factored in prior to any investment decision.

Beyond 2020, the company also faces resistance through vehicle electrification and environmental legislature in various operating states which it will have to handle through future works in the pipeline. Additionally, exchange rate risks are present by using USD as the base currency which has faced turmoil in recent months. Luckily, derivative positions the company hold hedge against such fluctuations.

Conclusion

As Avis Budget Group continues to weather the financial storm of 2020, investors should lay weight to evaluating managements success thus far in preventing liquidity erosion and maintaining solvency. Although the market has certainly penalised the company on the back of global travel restriction impacting mobility and aviation stocks, a contrarian viewpoint would suggest that the strategy moving out of 2020 places CAR at the brink of explosion as the global economy slowly begins to reopen.

Despite the fact the balance sheet may not reflect this sentiment on paper, in my investing experience often it’s the companies that present with questionable balance sheets but crackerjack management style that become favourable over the mid-term. Especially when they are traded down and as the market chooses to judge against the company, as in the case of CAR. That’s where real money can be made. By using a contrarian flavour to one’s strategy the case is certainly made for Avis Budget Group. As travel demand rebounds and continues to climb out of the pandemic, so too can the company’s position, and the stock price will likely follow suit as the market looks to price in the above factors.

Thus, at the present valuation and market price, a strong investment case is made for CAR for entry at this very point in time, particularly for those holding an intermediate horizon. Long on CAR for the remainder of 2020.

Disclosure: I am/we are long CAR. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}