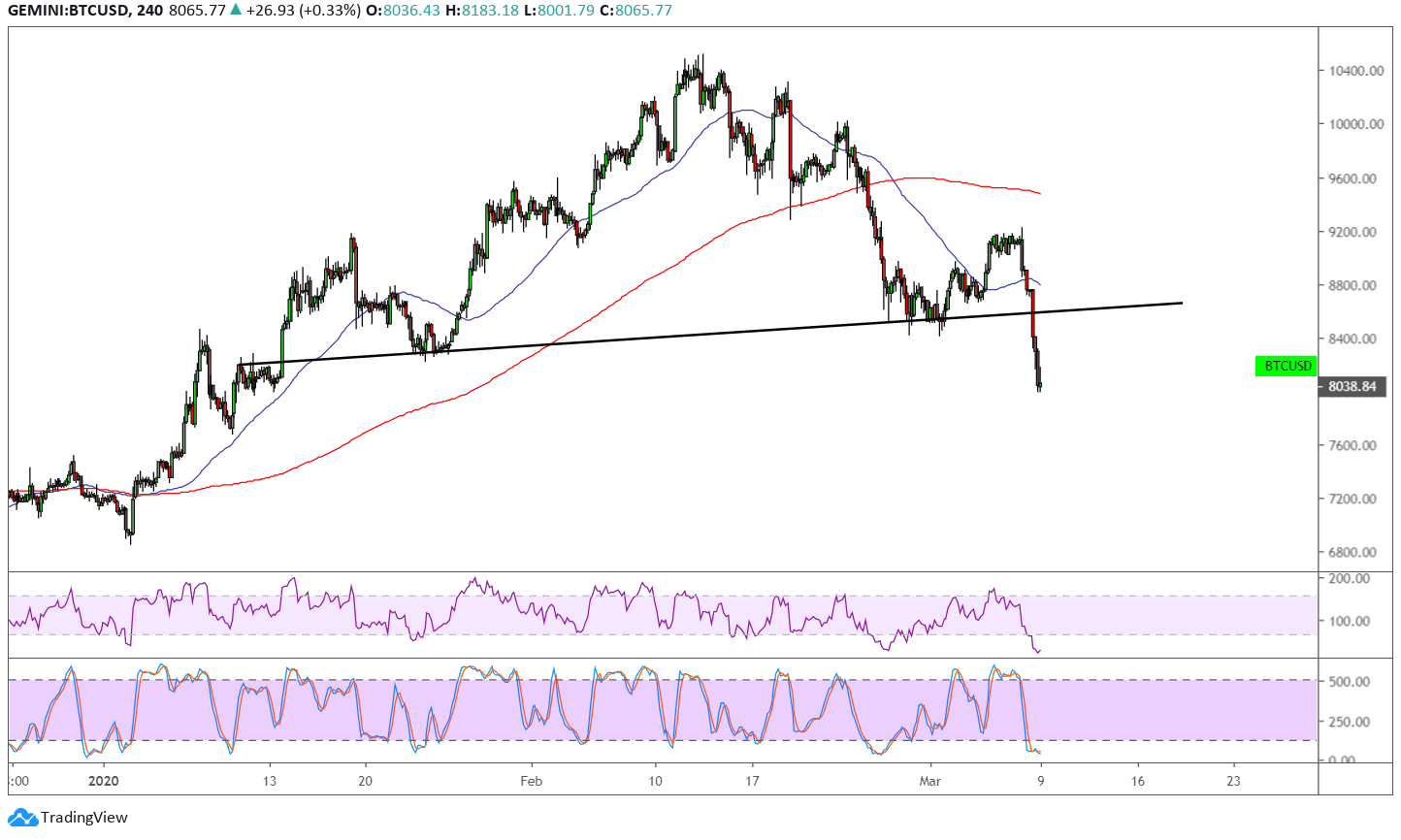

Bitcoin broke below the neckline of a larger head and shoulders pattern visible on the 4-hour time frame, indicating that another selloff is in the works.

The reversal pattern spans $8,800 to around $10,500 so the resulting slide could be at least $1,700 in height. The 100 SMA is below the 200 SMA to confirm that the path of least resistance is to the downside or that the selloff is more likely to gain traction than to reverse. Price is also below both moving averages, so these could hold as dynamic resistance levels.

RSI is heading lower to indicate that selling pressure is present, but the oscillator is already dipping into the oversold region to reflect exhaustion among bears. Stochastic is already in the oversold region and appears to be bottoming out to indicate that buyers could take over soon. In that case, a pullback to the broken neckline support could still happen before more sellers hop in.

It’s hard to pinpoint the exact cause of the slide, with many still blaming the recent run-up in risk aversion as a likely culprit. Global markets opened lower for the week as coronavirus fears continue to mount, although cryptocurrencies tend to enjoy safe-haven flows in some cases like these.

There’s also the news that one the most significant cryptocurrency scams from the past few years known as PlusToken recently tried to launder another 13,000 bitcoins in the past 24 hours. It didn’t help that Brian Armstrong, the chief executive of the largest U.S. bitcoin and cryptocurrency exchange Coinbase admitted that bitcoin might not be the coin that drives up mainstream adoption, citing:

“I think it’s still very much up in the air which blockchain will help get crypto from [around] 50 million users to 5 billion.”

Images courtesy of TradingView

{kind=link}