Our SWOT analysis (Strengths, Weaknesses, Opportunities, Threats) is meant to serve as a baseline for doing research on companies that we might invest in at certain prices. As Warren Buffett has repeated many times, only by getting to know a company’s business, can we start to understand whether or not to invest our hard earned money.

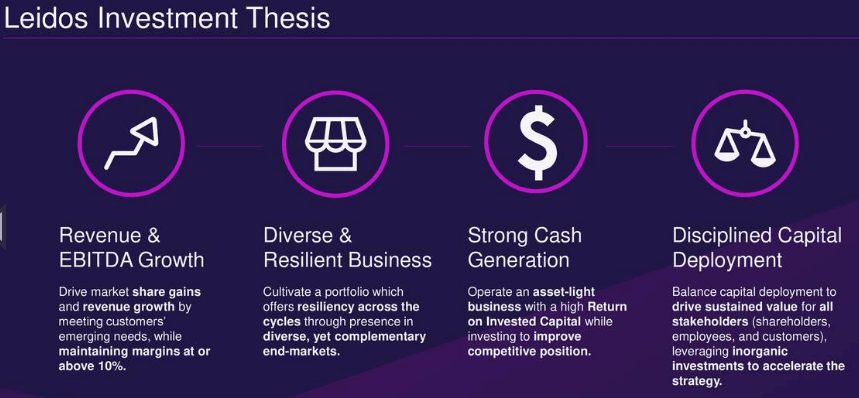

Leidos (LDOS) is a company that is poised to benefit from the ongoing need for intelligent defense systems, air navigation systems integration and managed health services. The company is likely to experience growth as we need to maintain the latest defense technology for the numerous potential dangers in the world today.

Leidos operates three business segments:

1. The Defense segment is the largest and comprises 48% of total revenue. This segment provides intelligence systems, command & control, logistics, data analytics, and cyber security solutions. These solutions cover air, land, sea, space, and cyberspace.

2. The Civil segment comprises 34% of total revenue and handles systems integration for air navigation service providers. The Civil segment offers services to the FAA, TSA, airport operators, and vehicle/cargo inspection systems. This segment also offers IT solutions for mobility, cloud computing, data center, networks, help desks, app modernization, asset management, and more.

3. The Health segment comprises 18% of revenue and provides global solutions for the health and well being of people for federal and commercial customers. These solutions include: managed health services, complex systems integration, life science services, and enterprise IT transformation.

Leidos gets a continual flow of new contracts, which drives ongoing growth. This is evident in the 48% increase in the backlog within a little over two years. The recent intention to acquire Dynetics (privately owned) for $1.7 billion can help strengthen the company’s defense, civil, and intelligence businesses. The acquisition can also strengthen Leidos’ R&D for developing new solutions for the most challenging customer needs.

source: Leidos Company Presentation

Strengths

Leidos has an extensive list of internal strengths that are positive drivers for their businesses.

- Leidos has a growing backlog: Net bookings increased 9.5% to $11.5 billion in the first 9 months of 2019. The total backlog increased 17.7% to $23.9 billion over the same time period. This will help drive revenue growth as actual sales are realized.

- The company has a highly competent workforce: 67% of employees are rated top secret and above, 39% are (security) cleared employees, 21% have Master Degrees, 3% or 1,000 have PhDs, 22% are military veterans.

- Diverse set of businesses: Although the company is highly dependent on the defense segment, slightly more than half of revenue is derived from the Civil and Health segments. This diversifies the company if defense spending had to be cut.

- The balance sheet is strong overall with 1.16x more current assets than current liabilities and 1.53x more total assets than total liabilities with share holders’ equity of $3.25 billion.

- The company’s cash flow is strong: Over the past 12 months, Leidos had $927 million in operating cash flow. From this, CapEx was $87 million, $94 million was spent on acquisitions, $50 million in debt was repaid, $686 million of shares were repurchased, and $148 million was paid in dividends. Some cash was added to this from sales of property, plant, & equipment of $96 million and divestitures of $183 million.

- High ROE of 20%: This is an example of management effectiveness.

Weaknesses

Leidos has a few internal weaknesses that can be improved upon.

- Leidos is smaller than the large defense contractors. The company has less resources as a result. This could make acquisitions or large investments more challenging for Leidos as compared to their large competitors.

- Leidos has a lower gross margin than their competitors. Therefore, there is room for improvement for reducing the cost of revenues.

| Company | Gross Margin |

| Leidos | 13.8% |

| Raytheon (RTN) | 26.9% |

| Northrop Grumman (NOC) | 20.6% |

| General Dynamics (GD) | 17.7% |

| Lockheed Martin (LMT) | 14% |

source: seekingalpha

- There is 5.6x more total debt of $3.54 billion as compared to total cash of $635 million. The good news is that Leidos has sufficient cash flow to handle this debt. The $3.54 billion of debt could be paid off in about 7 years based on the recent amount that the company is paying off per year.

- Leidos is highly dependent on obtaining contracts from government agencies. In 2018, 85% of revenue came from U.S. government agencies.

Opportunities

There are a few strategies that Leidos can implement to improve the business.

- Continual development of new defense technology: Leidos should ensure that they remain on the cutting edge of new technology. The uncertainty in the world today creates the need for advanced defense systems so that the U.S. and their allies are well equipped to handle security/military-related threats and remain a step ahead of the enemies.

- Expansion of the Health segment can help to further diversify the company. Growing the Health segment’s revenue to be a larger percentage of total revenue can accomplish this. This could be through organic growth and through acquisitions.

- Quick and successful completion of the Dynetics acquisition: This will ensure that Leidos reaps the intended benefits of acquiring the company.

- Strategic new acquisitions for add-on growth. Leidos should keep their eye out for additional companies to acquire. This will help drive the company’s ongoing growth.

Threats

Leidos faces a number of potential external threats that could have a negative impact on the company.

- Reduced defense spending by the U.S. and allied countries could reduce the amount of revenue earned from contracts. The amount of contracts could be reduced and the total dollar amount of contracts could be decreased.

- New government regulations in each business segment could increase costs for Leidos. This could be in the form of product/service compliance regulations or new health regulations.

- Increased competition for similar products/services could reduce Leidos’ revenue or market share. Better offerings from competitors could reduce the amount of contracts that Leidos receives. Competitors include: BAE Systems (OTCPK:BAESY), CACI (CACI), Booz Allen (BAH), General Dynamics, Lockheed Martin, L3Harris (LHX), Northrop Grumman, and Raytheon.

- Leidos is at risk of legal disputes regarding their products/services. Significant damages to be paid under a large legal dispute could have a negative impact on the company.

Long-Term Outlook for Leidos

The constant threats in the world today are positive for Leidos’ long-term growth. More intelligent systems are needed in today’s volatile foreign relations environment. Threats can be combatant related, while others could be cyber-based. Leidos has a variety of solutions for the numerous threats that we face.

The Dynetics acquisition is expected to close in the first quarter of 2020. This can be a near-term positive catalyst as it is expected to be immediately accretive upon closing. The long-term catalyst can come from expectations for improvements in Leidos’ rapid prototyping and agile systems integration and production as a result of the acquisition.

It would be reasonable to expect Leidos to continue to be awarded lucrative contracts going forward. This is due to the company’s expertise and track record of delivering effective solutions. It is also likely as a result of the various threats facing the U.S. and their allies from multiple sources.

The 2020s will see the transformation of the economy during the 4th Industrial Revolution. We are also running head first into a wave of demographic and debt driven problems that will need solving. A cautious, but forward looking approach, will be required to thrive in what could be a lost investing decade for many, much like 2000-2009.

Benefit from the insights of Kirk Spano, Dividend Sleuth and David Zanoni. Get exclusive investment ideas based upon in-depth and up close research that few others do.

Sign-up now for a free trial and 20% first year discount.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. Business relationship disclosure: The article was written by David Zanoni for Kirk Spano’s Margin of Safety Investing service. Most of our SWOT analyses are only available to subscribers, but we release a few to the public as samples. Leidos stock increased 3% since this SWOT analysis was released exclusively for subscribers on January 6, 2020.

Additional disclosure: The article is for informational purposes only (not a solicitation to buy or sell stocks). David is not a registered investment adviser. Kirk Spano is an RIA. Investors should do their own research or consult a financial adviser to determine what investments are appropriate for their individual situation. This article expresses my opinions and I cannot guarantee that the information/results will be accurate. Investing in stocks involves risk and could result in losses.

{kind=link}