Philip Morris International (PM) is a buy for the dividend income investor that also wants to take advantage of the overdone stock price dip. Philip Morris International is one of the largest worldwide manufacturers and distributors of smoking products. PM is a conservative investment for the income investor who also wants a moderate growth estimate of 7% increasing since the FDA approval of IQOS.

Philip Morris International is 4.1% of The Good Business Portfolio (a full position). The company has slow growth and has the cash it uses to increase the dividends each year.

As I have said before in previous articles,

I use a set of guidelines that I codified over the last few years to review the companies in The Good Business Portfolio (my portfolio) and other companies that I am reviewing. For a complete set of guidelines, please see my article “The Good Business Portfolio: Update to Guidelines, March 2020“. These guidelines provide me with a balanced portfolio of income, defensive, total return, and growing companies that hopefully keeps me ahead of the Dow average.

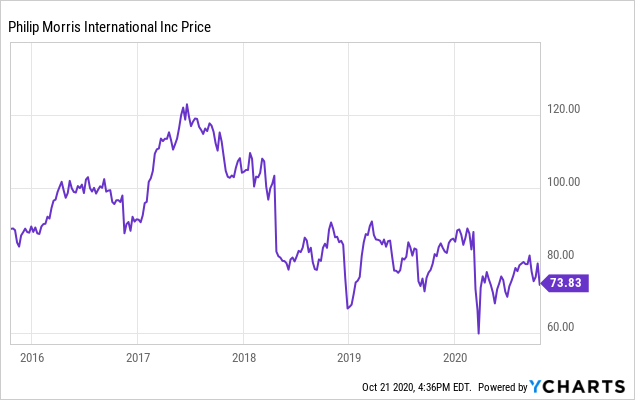

When I scanned the five-year chart, Philip Morris has a poor chart going up and to the right in a steady, strong slope for two of the five years with a downturn starting in 2018 when the FDA started to investigate vaping and other smokeless products. Recently PM stock price has gone down with the market correction and recovered, but not as much as the market. This correction creates a buying opportunity for a great slow-growing defensive business at a discount price with a high yield while waiting for the pandemic to be controlled.

Fundamentals and company business review

The method I use to compare companies is to look at the total return, as shown from my previous articles in the section below.

The Good Business Portfolio Guidelines are just a screen to start with and not absolute rules. When I look at a company, the total return is a key parameter to see if it fits the Good Business Portfolio’s objective. My total return guideline is that total return must be greater than the Dow’s total return over my test period. Philip Morris missed against the Dow baseline in my 58-month test compared to the Dow average. I chose the 58-month test period (starting January 1, 2016, and ending to date) because it includes the great year of 2017 and 2019 and other years with fair and bad performance.

The poor Philip Morris’s total return of +14.49 compared to the Dow base of 59.40% makes Philip Morris a poor investment for the total return investor. Still, it makes an interesting investment for increasing income investors. Looking back five years, $10,000 invested five years ago would now be worth over $12,100 today. This slight gain makes Philip Morris a poor investment for the total return investor looking back, which has future growth as the United States and worldwide countries need more of the company’s IQOS heated tobacco products.

Dow’s 58 Month total return baseline is 59.40%

|

Philip Morris does meet my dividend guideline of having dividends increase for 8 of the last ten years and having a minimum of 1% yield. Philip Morris has an above-average dividend yield of 6.1% and has increased for thirteen years, making Philip Morris the right choice for the dividend growth investor. The dividend was last increased in September 2020 for an increase from $1.17/Qtr to $1.20/Qtr or a 2.6% increase. The five-year average payout ratio is high, at 94%. After paying the dividend, this leaves cash remaining to increase the company’s business by developing new additions to the company’s product lines.

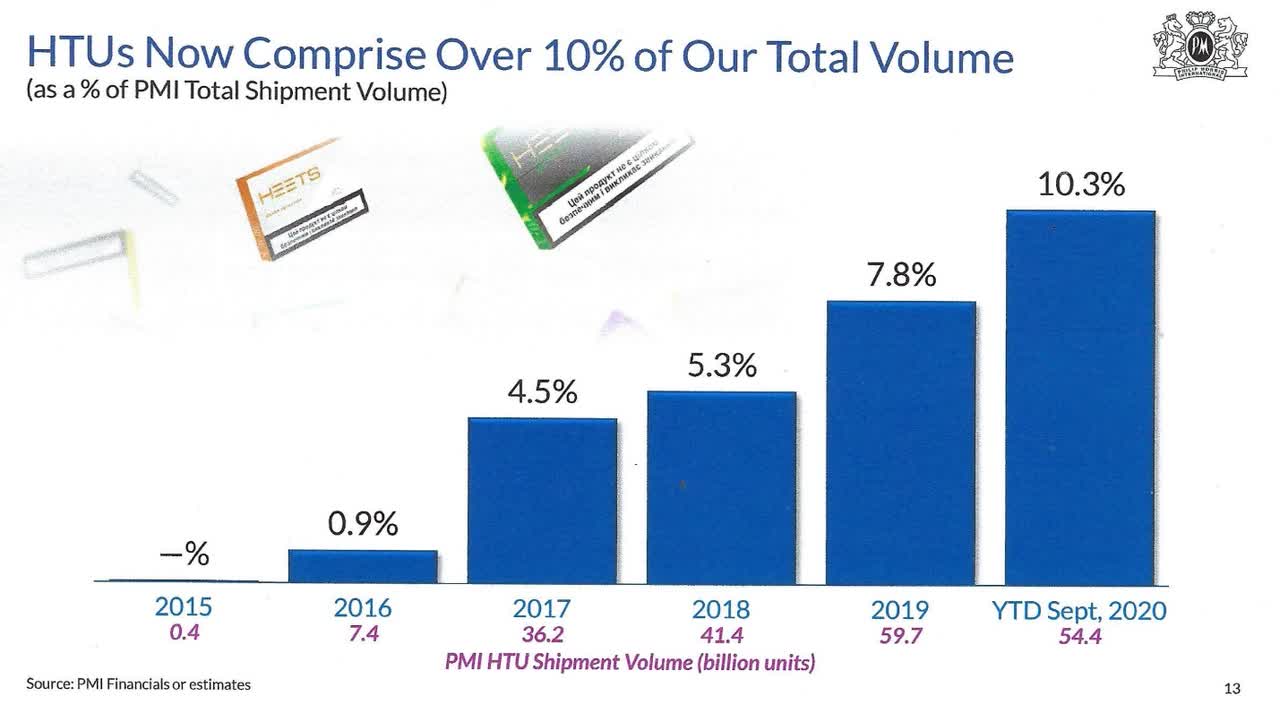

I also require the CAGR from now on to cover my yearly expenses and my RMD with a CAGR of 7%. My dividends provide 3.3% of the portfolio as income, and I need 1.9% more for a yearly distribution of 5.2% plus an inflation cushion of 1.8%. The three-year forward S&P CFRA CAGR of 4% misses my guideline requirement, but I feel this understates the company’s potential, and I rate PM at 7% growth. This slow future growth for Philip Morris can continue its uptrend benefiting from the reliable growth of heated tobacco products worldwide. Still, it may be mitigated by the coronavirus short term. The graphic below shows the growth of the HTU product.

Source: PM earnings call slides from web site

I have a capitalization guideline where the capitalization must be greater than $10 Billion. Philip Morris passes this guideline. Philip Morris is a large-cap company with a capitalization of $123 billion. Philip Morris 2020 projected cash flow at $10.2 billion is good, allowing the company to have the means for company growth each year. Companies like Philip Morris have the cash and ability to buy other smaller companies.

One of my guidelines is that the S&P rating must be three stars or better. Philip Morris S&P CFRA rating is five stars or strong buy with a target price of $95, passing the guideline. Philip Morris’s price is below this target by 23%. Philip Morris is below the target price at present and has a low forward PE of 15, making Philip Morris a great buy at this entry point. Considering the company’s potential growth and stability, if you are a long-term investor that wants good, increasing income and moderate growth, you may want to look at this company. Take advantage of the long term correction and buy a good business at a nice discount.

One of my guidelines is would I buy the whole Company if I could. The answer is yes. The total return is not good looking back, but the above-average dividend yearly yield has grown at a fair rate over the past twelve years, making Philip Morris a great business to own for the growth and the long-term income investor. The Good Business Portfolio likes to embrace all kinds of investment styles. Still, it concentrates on buying companies that can be understood, makes a fair profit, invests profits back into the business, and generates a good income stream. Most of all, what makes Philip Morris interesting is the increasing long-term demand for the company’s smokeless products, and the product pricing is inelastic.

I don’t have a guideline for earnings but look for my positions’ earnings to consistently beat their quarterly estimates. For the last quarter on October 20, 2020, Philip Morris reported earnings that beat expected by $0.06 at $1.42, compared to last year at $1.43. Total revenue was lower at $7.45 billion less than a year ago by 2.5% year over year and beat expected total revenue by $180 million. This was a mixed report with bottom-line beating expected and the top line decreasing with a decrease compared to last year. The next earnings report will be out January 2021 and is expected to be $1.23 compared to last year at $1.04, a strong increase.

Philip Morris International is one of the largest manufacturers and distributors of tobacco products in foreign countries.

As per data from Reuters

The company is engaged in the manufacture and sale of cigarettes, other tobacco products, and other nicotine-containing products in markets outside of the United States. Its segments include European Union (EU); Eastern Europe, Middle East & Africa (EEMA); Asia, and Latin America & Canada. Marlboro leads the company’s portfolio of international and local brands. Its mid-price brands are L&M, Lark, Merit, Muratti, and Philip Morris. Its other international brands include Bond Street, Chesterfield, Next, and Red & White.

Overall, Philip Morris is a good defensive business with a 7% CAGR projected growth as the worldwide economy grows going forward with the increasing demand for more smokeless products. I feel this growth rate will be at least 7% because of the IQOS and HEETs products. The good earnings and revenue growth provide PM the capability to continue its growth as the business increases by demanding the inelastic priced smokeless sector.

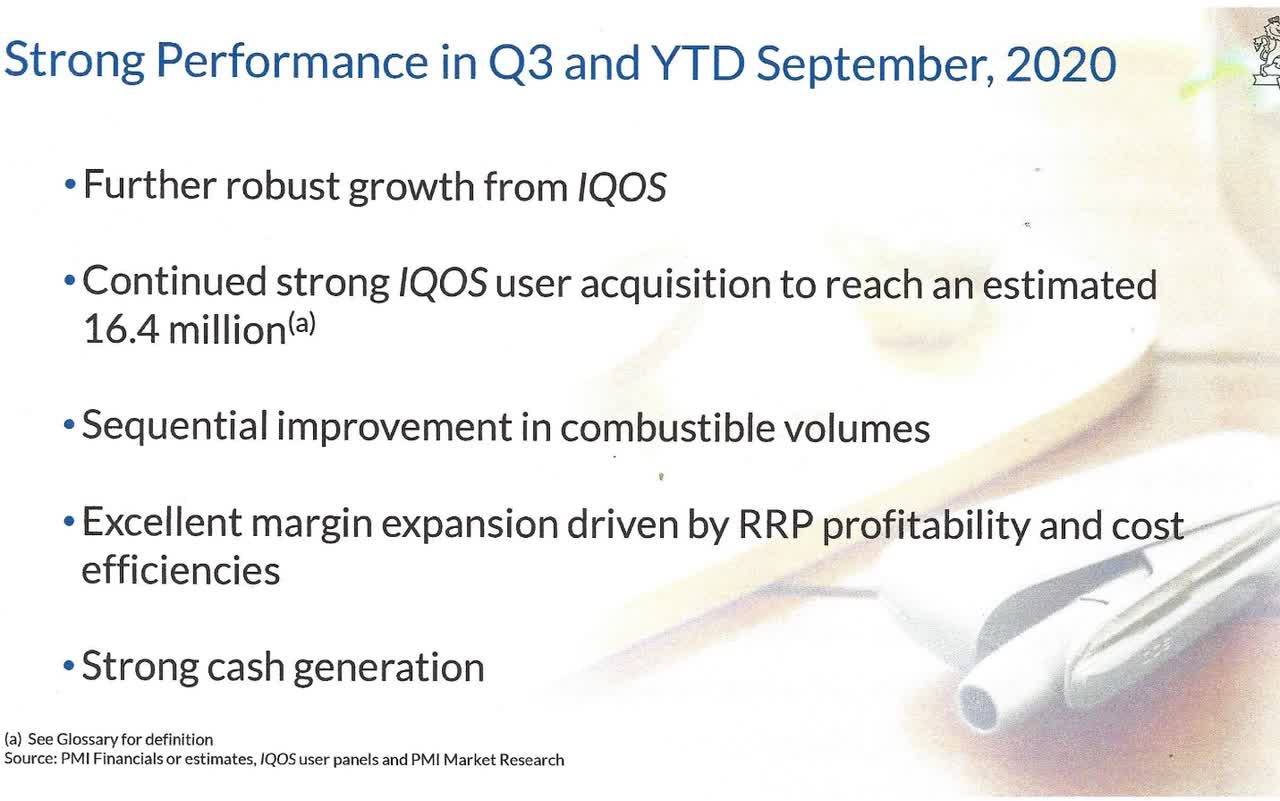

From the 3rd quarters earns call, Philip Morris had good growth in IQOS. HTU volumes have grown 28% year-to-date with a positive mix of net revenues, where RRPs made up one-quarter of the Q3 business. IQOS users were an estimated total of 16.4 million at the end of September. Their cash generation was also strong, with $3.6 billion of operating cash flow in the quarter with the target of at least $9 billion this year. The organic growth was 6.5% in revenue per unit. Combustible tobacco pricing was up 2.1%, reflecting solid pricing in several markets. The net revenue decline was offset by a strong adjusted operating income margin expansion of over 300 basis points on an organic basis.

Source: PM earnings call slides from web site

Conclusions

Philip Morris International is a good investment choice for the dividend income investor with its above-average high dividend yield and a poor choice for the total return investor looking back. Philip Morris International is 4.1% of The Good Business Portfolio and will be held and watch it grow. PM will be held in the portfolio and trimmed when it reaches 8% of the portfolio. If you want a growing dividend income and fair total return to come in, PM’s smoking product business may be the right investment for you. Due to the FDA’s possible regulations and the downturn in stock price correction from the COVID virus, I think the price drop creates a buying opportunity to buy a quality business at a bargain price.

The total return for the Good Business Portfolio is ahead of the Dow average from 1/1/2020 to October 16 by 0.44%, which is a small gain above the market gain of 0.24% for the Dow with Boeing (BA) a strong drag but getting better. Each quarter after the earnings season, I write an article giving a complete portfolio list and performance; the latest article is titled “The Good Business Portfolio: 2020 2nd Quarter Earnings and Performance Review“. Become a real-time follower, and you will get each quarter’s performance for my portfolio companies after this earnings season is over.

Disclosure: I am/we are long BA, JNJ, HD, EOS, DHR, MO, DIS, V, OHI, TXN, PM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Of course, this is not a recommendation to buy or sell, and you should always do your own research and talk to your financial advisor before any purchase or sale. This is how I manage my IRA retirement account, and the opinions of the companies are my own.

{kind=link}