Thesis

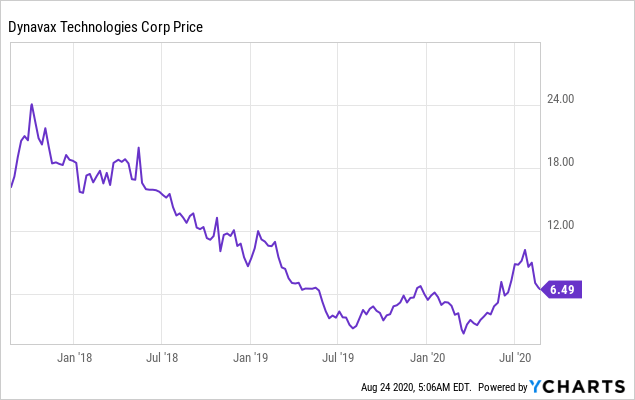

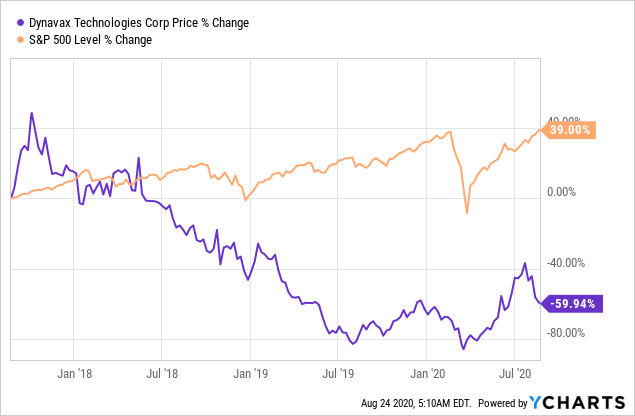

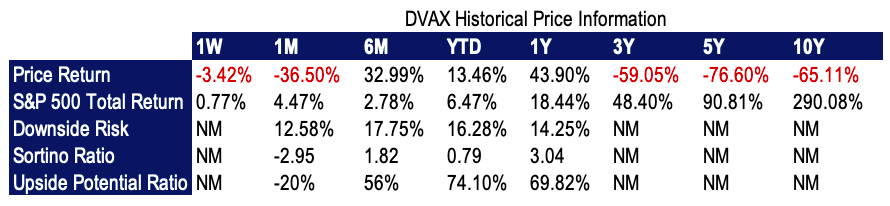

Dynavax Technologies (NASDAQ:DVAX) has again left investors with a sour taste, having given away -36.5% in price returns over the previous month, after a 385% gain to $11.70 in July from the March selloff. Since 2017, shares have drastically declined -59.94% to today’s price of $6.49, but perhaps what is equally as unimpressive is the fact the stock has given away over -93.02% since listing in 2004/2005. Furthermore, investors don’t seem to have been rewarded for the high downside risk over price returns during these periods, with low Sortino Ratios across each examinable period in our analysis. We are dissatisfied with the level of downside risk at play over this term, particularly with 14.25% risk to the downside over price returns over the single-year period to date, representing an unfavourable divergence between risk and reward, whereby shareholders have experienced heightened levels of risk exposure with inadequate compensation through capital losses.

Data by

Data by Data by

Data by

Data Source: Seeking Alpha; Author’s Calculations

Here, we will assist investors with their own reasoning by providing a brief snapshot of DVAX’s propensity to turnaround current market expectations and capitalise on recent advancements in Heplisav-B, the purported disruptor for all known subtypes of hepatitis B virus infection in the 18 years and over domain. We advocate investors to complete a deep dive analysis to garner the complete picture for the company’s current posture, which we have completed in house. However, we feel this brief overview will enable investors to inform themselves of the company’s capacity to generate value for shareholders, partially by demonstrating the ability to generate return on capital and to finance ongoing growth capital. We will incorporate a basic screening strategy to identify this potential and analyse some other metrics to give investors further insight over their own decision-making process.

Valuation

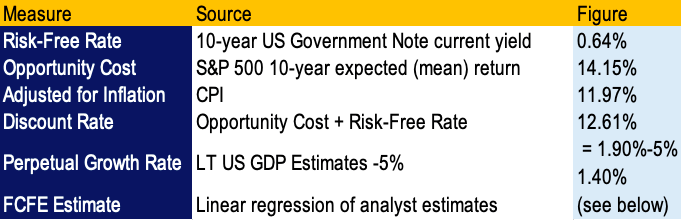

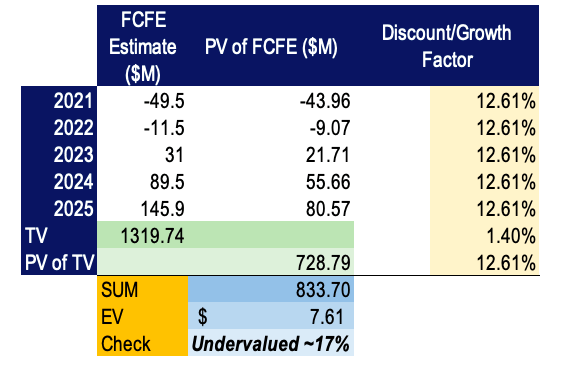

We have valued DVAX using a DCF analysis on FCFE estimates, figures we have obtained by performing linear regression over the consensus of analyst estimates. We have forecasted 5 years out, to reduce forecasting risk and to incorporate the disruptive nature of the biotech industry, alongside the uncertainty DVAX faces as a majorly single-skewed company. We are accustomed to assigning a terminal value using the PRAT model of DuPont. However, as the company is currently unprofitable, we have assigned a terminal growth rate related to the long-term US GDP forward estimates to obtain a terminal value in year 5. Additionally, we have incorporated the 10-year treasury yield alongside the opportunity cost of holding the S&P 500, using the 10-year expected (mean) return, as the proxy for the discount rate.

Data Source: Author’s Calculations

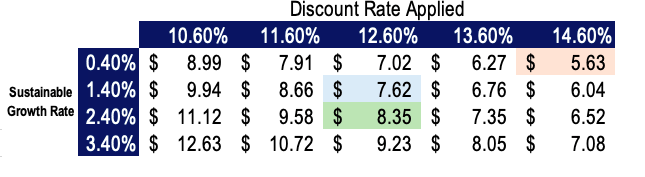

On a DCF basis, based on FCFE numbers we have obtained from the regression analysis, we see the stock as marginally undervalued compared to the market price. In the downside case, the stock is certainly overvalued as seen in the sensitivity analysis below. We would argue that there is an asymmetry between the valuation and the stock price in the base case, which highlights notable upside potential should the market value the product offerings that DVAX presents, alongside the alignment with the novel adjuvant CpG 1018, which has potential implications towards COVID-19 vaccine, amongst others. However, we set a price target of $5.63 based on current performance and our valuation model.

Data Source: Author’s Calculations

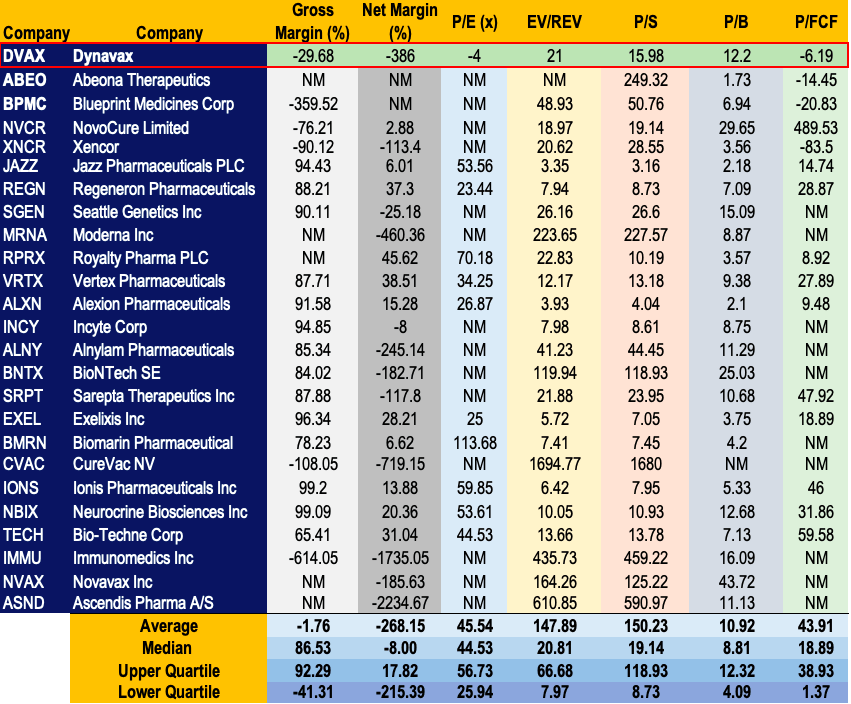

In relation to companies within the industry, we have collated a large data set to give insight to the company’s standing relative to peer entities. We feel this gives investors a greater snapshot of DVAX’s posture in relation to several valuation metrics. As there are some companies whom are currently unprofitable, DVAX included, there are blank scores for some metrics, and others were not meaningful to this analysis. We have scored the P/E for DVAX, for reference, although we lay less weight to the figure in this instance.

NOTE: Click for a larger view.

Data Source: Author

We see that DVAX is above the median figure of the comparables listed for EV/Revenue and is in the lower quartile of the group, alongside Price/Sales, with a figure of 15.98 vs the upper quartile figure of 7.97, although is below the median figure in this examination. On a Price/FCF front, much won’t be told due to negative FCF recorded until present, but we are seeking a P/FCF of less than 8 in the current climate. Certainly, DVAX scores below 8 here, at -6.19, but we feel less weight should be placed onto this figure as it doesn’t tell the whole picture and doesn’t provide reasonable basis for comparison with peer entities. Plus, we would prefer a score greater than 0 for a successful pass in this valuation input.

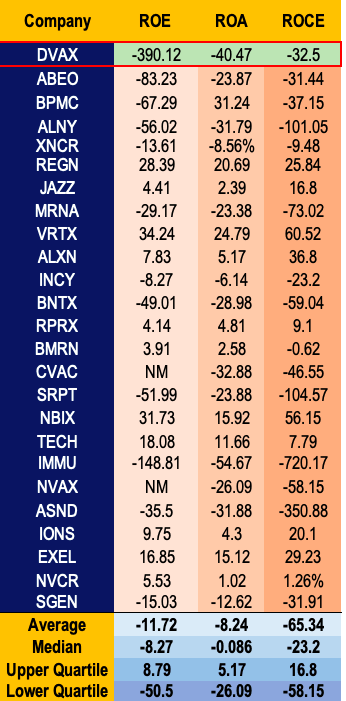

We have also examined Price/Book and the inverse Book/Market ratios as a measure of value and value creation by management. DVAX scores a Price/Book value of 12.2, which is aloft the industry median and comparables Abeona Therapeutics (ABEO), Blueprint Medicines Corporation (BPMC), NovoCure Limited (NVCR), and Xencor (XNCR). We use the book/market metric to understand value creation for shareholders from management. A score greater than 1 we feel evidences this sentiment, and DVAX scores 0.078 on this examination, signifying that there has been an absence of value created for shareholders above and beyond book value. We also feel that this evidences that the market is willing to pay for more for ownership into the company than its assets are worth. These points remain within our narrative that the company may not have the demonstrable capacity to reward shareholders moving forwards.

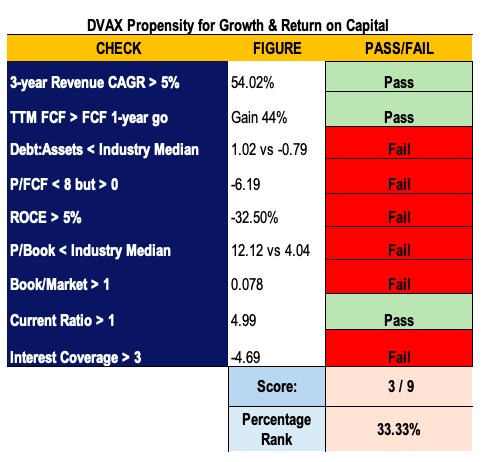

In our model, we also look to observe ROCE that is greater than 5% with a pattern of growth over the single-year and 3-year period, as we feel this signifies growth in valuation and, therefore, value creation for shareholders. We often observe companies with low ROCE and growth of the same to be ubiquitous with poor valuation growth. By this examination, we observe DVAX score -32.5% return over capital employed, which has climbed from -68.5% 3 years prior. We are unsatisfied with this score, particularly in line with poor ROA of -40.47% and equally as unsatisfactory asset turnover of ~12 cents for every dollar invested. In its growth stage, we firmly believe that DVAX needs to demonstrate greater competency in invested capital and garner greater turnover from the asset base to continue to remain competitive. Therefore, DVAX scores poorly here.

Furthermore, in our overview, we have included the current debt-to-assets measurement, which we hope to observe as less than the industry median. At a score of 1.02, the debt ratio signifies that a hefty portion of the company’s debt figure is funded by the asset base and sits well above the industry median of -0.79. Again, DVAX has failed to demonstrate the capacity for value and growth from these measurements.

Data Source: Author

Thus, there seems to be a discrepancy between the intrinsic value and the company’s posture within the market on a comparables front. We tend to believe that DVAX is underperforming as compared to market expectations, particularly in respect to the data sets above alongside the unsatisfying returns to shareholders over recent time, alongside lacklustre gross revenue performance to date. The market doesn’t necessarily lay weight to fair value, particularly in the absence of the necessary fundamental momentum to support and justify the valuation. The suite of metrics that we have performed over the stock’s value certainly highlights that it lays in the underperform domain, by our analysis. Should the market foresee the potential in revenue growth and success of DVAX’s hero products, there is a potential justification for entry at the current intrinsic value. However, greater evidence is required from the company’s end to bolster the upside case here.

Now, let’s examine the company’s ability to deliver on the inputs required to bolster the valuation, to observe management’s capacity in generating growth in revenues, FCF, and return on employed capital through investment and via the asset base.

Performance

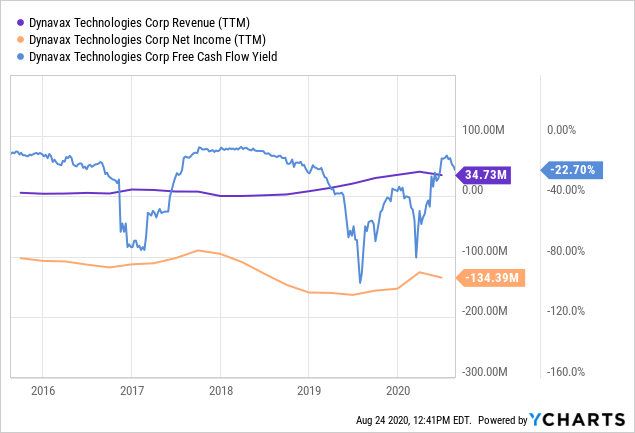

For DVAX, all product sales currently consist of Heplisav-B revenues in the U.S. For Q2, total revenues were down -67.86% YoY and behind by -14.11% on a TTM basis. YTD revenues were recently posted at $13.6 million, down -3.47% YoY; both figures not alarming, considering that adult vaccine utilisation remained low throughout Q2, including for hepatitis-B vaccination, as many centres elected to close elective procedures in the wake of government social-distancing restrictions and to reduce COVID-19 transmission rates. This undoubtedly hurt Heplisav-B sales. Fortunately, vaccination utilisation has begun to normalise since June, where it reached ~60% of pre-coronavirus levels and will likely continue north as the economy slowly reopens.

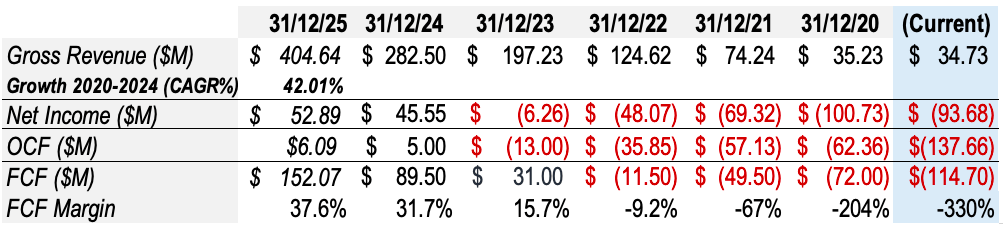

Revenues have climbed drastically since Heplisav-B’s approval in 2017, from ~$330,000 to $34.7 million in Q2 2020, signifying a CAGR of 54.02% over this period. In our analysis, we are seeking a 3-year CAGR greater than 5% of companies of this company’s size, so DVAX scores well here. However, DVAX has incurred consistent losses on gross profit, cash from operations and negative FCF since inception, and future losses are by all means anticipated into the near future as the company continues to commit towards the commercialisation of Heplisav-B. Gross and net margins, therefore, remain under pressure, currently at -29.68% and an unpleasing -396%, respectively, which signifies large room for improvement and demands significant sales growth from their flagship product coming out of 2020.

Data by

Data byFCF has remained negative since 2017, most recently recorded at -$114.7 million in June 2020. For our screen, we are seeking to observe TTM FCF that is greater than FCF of 1-year previous, in which DVAX scores well, as FCF expanded 44.90% YoY. Additionally, on the current figures, we observe an FCF yield of -22.7%, which undoubtedly does not stand out to us. We are certainly aware of the evidence of FCF in growth companies that are reinvesting earnings as growth capital. DVAX showing reinvestment growth in NWC of 44.5% certainly supports this sentiment, although seems out of sync with CAPEX growth of only 0.90%. One might anticipate higher correlation in growth of capital expenditures alongside the plan to commercialise and scale Heplisav-B, amongst other projects within the pipeline.

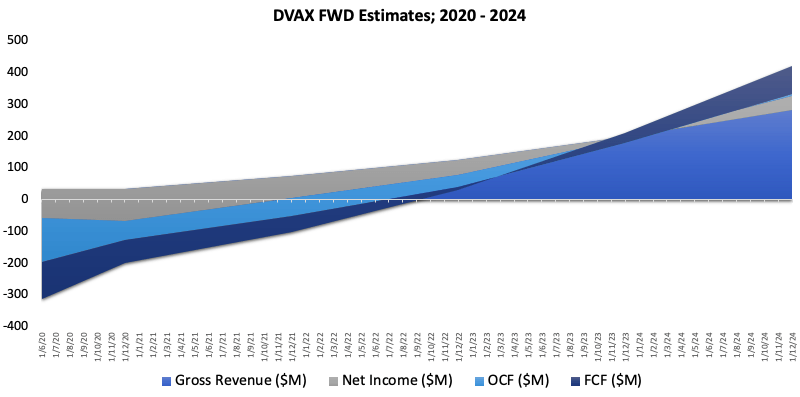

We foresee revenue growing at a CAGR of 42.01% over the next 4-year period from FY2020 end in our upside case, alongside growth in net income, OCF, and FCF over this same period. Our figures are not out of alignment with the consensus of analyst estimates, and performing linear regression over the consensus of said estimates yields remarkably similar results. Our forecasts shown here represent our upside case, on the belief that the company will drive sales of the hero product, remain competitive through establishing distribution channels, and successfully commercialise said product, and profit on the back of the CpG 1018 adjuvant with strategic collaborations and applications with peer entities, alongside approval of Heplisav-B within the European framework.

Data Source: Author’s Calculations

Data Source: Author’s Calculations

Solvency

We feel it is equally as important to visualise the solvency capacity of DVAX to fund ongoing capital expenditures and the variable costs associated with sales growth, alongside meeting its obligations as they fall due. At the exit of Q2, DVAX had $200 million in cash and equivalents and marketable securities, which means, on a short-term solvency basis, the company has 4.99x coverage over short-term obligations. Such coverage is favourable alongside negative net cash burn for the quarter of -$7.53 million a month leading to June; a plus for the company considering lower than anticipated sales this year and ongoing losses on revenue & net income.

In February of 2018, the company opened a $175 million Loan facility with CRG Servicing LLC, for access of liquidity of $173.3 million, maturing in December 2023. The effective interest on this facility is at 10.3% currently, and the company paid a portion of the interest in kind ultimately increasing the principal to $181 million. Therefore, there are no meaningful debt maturities within the next 2-year period, but in 2023, the principal must be repaid including the interest payment in kind, a point for investors to watch over regarding debt management by the leadership outfit.

Additionally, the interest expense is not well covered at -4.69x coverage based on the TTM EBIT total, outlining the greater attention needed by management to meet debt obligations as they all due. The EBIT total reflects a lacklustre performance from sales of Heplisav-B alongside poor return on employed capital and likely, inadequate asset turnover from the asset base. DVAX also holds $1.83 in CF/share, which we feel is on the low side in relation to the above solvency examination.

Screening Checks

Although negative free cash flow may not be a huge concern in growth-style companies, combined with poor ROCE and ROA, low asset turnover, large margin pressure, uncertain sales growth alongside various other factors, the picture is even less colourful when performing our basic screening test. We have scored the metrics outlined in this report as we feel it will give investors a solid fundamental overview on the company’s propensity to generate return on capital and consequently garner future returns for shareholders. The observable measurements are not unrealistic as a stress test for future management alongside company performance to date, in order to gain insight to the direction investors need to witness to deliver value in the foreseeable future.

Below are our checks highlighted throughout this analysis:

Data Source: Author’s Calculations

From this examination, we observe that DVAX fails in 6 out of the 9 basic tests we have examined, which we feel is unsatisfactory and, therefore, may hinder the company’s capacity to generate above-average returns for shareholders moving out of 2020. Thus, we are unconfident that the stock has the propensity to make a sharp turnaround or show a large breakout in the near term, unless there are significant changes to sales and revenue structure entering into the remainder of FY2020 and throughout 2021.

Further Considerations

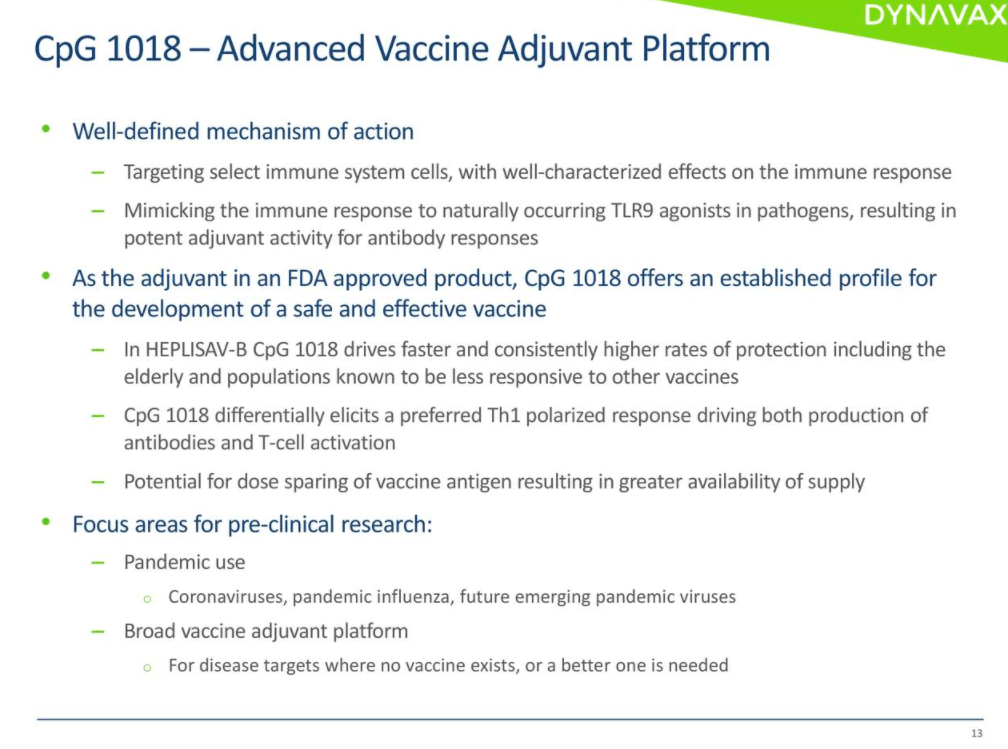

There is a great deal riding on the success of Heplisav-B, alongside various collaborations with the adjuvant CpG 1018. DVAX has signed several collaborations for this novel adjuvant, firstly in March with the Coalition for Epidemic Preparedness Innovations, then later again in April with Sinovac Biotech (SVA) and French company Valneva (OTCPK:INRLF), although little has been released from these ventures to date. Furthermore, the CpG 1018 adjuvant has been poised for use in a collaboration with the Serum Institute of India, to develop and commercialise an improved adjuvant pertussis vaccine. Keep an eye out in Q4 for the data release of these clinical trials, as reported by the company. More on CpG 1018, in a venture with Mount Sinai to build on their existing procedure designed to protect against all strains of influenza. This has potential excitement, particularly in the current state of the healthcare industry dealing with COVID-19.

Data Source: DVAX Investor Presentation

If, however, DVAX is unable to generate the required growth from Heplisav-B and other products in the pipeline, management will be required to fund operations through strategic alliances, licensing arrangements or through additional public and/or private debt and equity placements. The risks for investors within issuance of these facilities include dilution of current shareholders and heightened fixed obligations, which would register as senior commitments to the primary claimants, whilst likely including restrictive covenants that could hinder growth operations. It would be as if FCF couldn’t catch a break at all, should this pan out.

There is also significant competition within the Hepatitis-B treatment and prevention marketplace, where DVAX is a new entrant. The importance of sustaining sales growth and capturing market share cannot be understated. Thus, the company has significant work to do, in obtaining the required sales growth, accessing key providers and distribution channels whilst financing ongoing marketing, sales and infrastructure costs, in order to remain competitive if anything else. If unsuccessful, there is a large chance collaboration will be required with a 3rd-party biotech entity who run existing products, whereby revenues and profit generation will be shared amongst DVAX and the entity, adding further margin pressure and subtracting earnings potential. There is also no saying on the feasibility of these arrangements based on these facts, meaning there is a chance an arrangement may not even be met, which would potentially limit the timeliness of the company’s ability to establish Heplisav-B relative to competitors within the domain.

To partially offset these risks, as a competitive advantage, the Heplisav-B product has shown greater efficiency and efficacy in protection with Hep-B using only two doses over a single month, which is in contrast to the gold standard three-dose regimen that spans over six months. Provided the company establishes effective distribution routes and teams with the right providers, there is a huge chance DVAX’s approach will become the new gold standard, which presents an enormous market opportunity, particularly if approved in Europe, also.

Conclusion

We are bearish on DVAX, purely on the basis of the quantitative factors we have examined as a part of this report and our in-house analyses using our own proprietary research modelling. Whilst the company has shown headway in Heplisav-B alongside potential applications of the CpG 1018 adjuvant, we feel that DVAX has to demonstrate greater capacity from management and market acceptance to fulfill a bullish outlook, as, currently, the analysis doesn’t support this sentiment, in our view. Combined with the amount of returns that DVAX stock has given away over the previous 3+ years to date, we also feel the market has yet to realise the value that may exist in DVAX’s operations, provided they get it right and deliver on the sales expectations of their hero products. We hope to see a better Q3 performance, on the back of the economy slowly reopening and with vaccination utilisation returning to pre-COVID-19 levels, whereby we can gauge a perhaps more accurate snapshot of company performance based on the fundamentals discussed in this report, amongst others. We would encourage investors to perform a deep dive analysis to be in the best position to make the most informed decisions possible.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}