Investment Thesis

Peloton (NASDAQ:PTON) offers a compelling luxury stationary bike, treadmill, and content subscription. But it has entered into the “fitness wars” and competes in a smaller TAM than the company or analysts estimate. Further, its initial unit economics are not indicative of long-term trends. We have seen this story play out before with hardware plays like Jawbone and Fitbit (NYSE:FIT), and with niche fitness players like SoulCycle and Yoga Studio.

We believe the stock is worth ~$15/share right now, suggesting 50% downside.

Highly Competitive Market

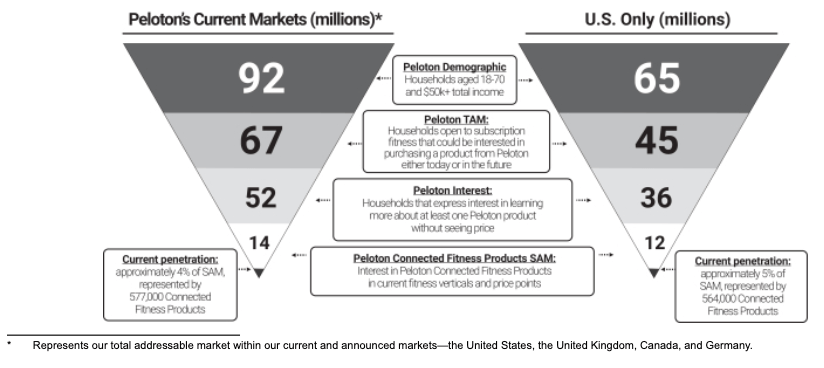

Peloton has entered into a highly competitive and fragmented market. Management estimates the addressable market is ~10% of the US (~45 million), and analysts take a haircut to estimate it at 14 million. We believe that is still generous, and that the actual addressable market is closer to 10 million.

Given this haircut, we believe the long-term runway and our discounted cash flows should reflect growth that eventually slows.

Peloton competes with traditional companies like NordicTrack, Echelon Fit, and others that offer bikes for less than half of what Peloton sells it. Many of the features are the same.

While the price reduction and move into content is one way to tackle a different market segment, we believe there are already players in those segments (i.e. free apps, Planet Fitness (NYSE:PLNT)).

In addition, there are dozens of competitors in the in-home market like Mirror and others that are competing for the same time. Not only will this hinder growth, but it will also cause pricing pressure in the medium term.

Source: Company S1

Brand Differentiation and Content Is Not Enough

Peloton claims its brand and content differentiation creates a moat, but we disagree. Although it helps to create a community, especially among those that are relatively price-insensitive, we surveyed a group of individuals who told us it is more about the workout. That experience can be bought for cheaper, and some people prefer workouts in studios.

Unit Economics Are Not Sustainable

The company mentions ~1% monthly churn with subscriber workouts growing from 7.5 million to 11.5 million from 2017 to 2019. These numbers are impressive, and so is the overall revenue growth.

Management is really executing well within the niche they have built, but we believe the valuation the business trades at warrants a much larger market opportunity. Eventually, these unit economics may suffer as the company moves outside of its core demographic, which we believe is more narrow than suggested.

Further, the business makes ~40% gross margins on hardware today, which account for ~70% of overall revenue. These financial metrics will eventually come under pressure as management has to make choices between market share and profitability. Today’s share price implies growth in both dimensions for a long time.

History Of Underperformance In The Segment

By the nature of being boutique or luxury, Peloton has to price at the upper end of its competitor range. This limits the number of people that can use the bike and the community size.

There is a history of companies in this space. YogaWorks (YOGA), a boutique studio chain with 46 locations, went public in 2017. It subsequently was delisted. SoulCycle famously removed its IPO, with 98 studios around the country.

These businesses are valuable, but they cannot get to scale because of their market strategy.

Peloton may claim that it is a different play without the real estate costs. We have examples in Fitbit, GoPro (NASDAQ:GPRO), and other “premium” devices. Do not forget Apple Health (NASDAQ:AAPL) and the giants who are entering the spaces with big customer moats.

We believe Peloton is closer to these examples than the “Apple of fitness”.

Valuation

The business trades at ~7x EV/S today and is unprofitable on other metrics. We can do a sum of the parts valuation on the subscription (~13x EV/S and the hardware at ~2x EV/S). Nautilus (NYSE:NLS), a peer, trades at ~0.5x EV/S, but is growing much more slowly. Even if we 4x this, it still results in a 2x EV/S multiple.

We can look at the subscriber growth and count to back into a valuation as well. Each subscriber is worth ~$5k ($8 billion EV/1.5 million subscribers). We can see Planet Fitness at ~$500, Netflix (NASDAQ:NFLX) at ~$1k, and Stitch Fix (NASDAQ:SFIX) at $800. This $5k value implies an LTV of 333 months or 27 years.

If we put a multiple of 4x EV/S, where the “dogs of SaaS” trade, that would imply a ~$15 price target. We believe this is a fair, premium valuation to all reasonable competitors and gives credence to the story of subscription, content, and a premium bike. To be clear, we love the product, but believe it is mispriced.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

{kind=link}